Tennessee-based Leaders Credit Union has $244.3 million in assets, approximately 35,000 members, and six branches in and around its hometown of Jackson, which is about70 miles east of Memphis. It has a mix of demographics you’d expect to find in any Mid-South American town, but despite the many ways in which it is a typical credit union, it is also aggressively expanding its digital services. The credit unionhas self-made mobile lending apps, responsive websites, and robust online alerts functions and promotional messaging prompts.

Marketing here also is high-tech in both its research and delivery. But despite the bits-and-byte crunching going on in the back office, the credit union’s mantra is all about simplicity. For instance, Leaders promises the ability to open an accountonline in 10 minutes, using one click from a home page that itself is heavy on simple functionalityand light on the bells and whistles.

The numbers show it’s working. At the end of 1Q2015, Leaders ranked in the top 10% among credit unions of $100 million to $250 million in 12-month member growth and in or very near the top 15% in return on assets, efficiency ratio and loan growth.

In this Q&A, Josh McAfee, Leaders’ vice president of marketing, offers a deep-dive look at how the credit union operates.

Describe your market area.

Josh McAfee: We have three distinct markets in West Tennessee. Our core is a fair blend of urban and rural, as it’s ahub city for all contiguous counties in the region. Our other markets are respectively hyper-rural and metropolitan,so we have an amalgam of membership and market. At an aggregate level, we are predominantly southern and rural, and thus late adopters on the technology spectrum.

What basic products and services do you offer on mobile?

CU QUICK FACTS

LEADERSCredit Union data as of 6.30.15

- HQ: Jackson, TN

- ASSETS: $255.4M

- MEMBERS: 36,215

- BRANCHES: 6

- 12-MO SHARE GROWTH: 12.07%

- 12-MO LOAN GROWTH: 17.50%

- ROA: 1.31%

- CORE PROCESSOR: Fiserv Portico (Service Bureau)

- MCIF/CRM: Fiserv Reporting Analytics/Fiserv Prism

- ONLINE BANKING: Digital Insight (NCR)

- MOBILE BANKING: Digital Insight (NCR)

- RDC: Vertifi (Through DI/NCR)

- BILL PAY: FIS Matevante (Through DI/NCR)

JM: We offer the core services of balance inquiry, transaction history with check image viewing, intra-account transfers, and bill payment (and origination).

Extra to the core, we also offer remote deposit capture, geo-location of proprietary and shared branches and ATMs, mobile-optimized loan application, and a loyalty program that allows checking accountholders to add digital coupons to their debit cardand earn cash back at POS.

Most recently, we released a dedicated mobile application for our VISA credit card program that offers the same core services as well as the ability to dispute a charge and report a card as lost or stolen.

These are all supported on Apple and Android platforms alike, plus our responsive website.

What about lending and account opening?

JM:We have five online account and loan applications. The most robust, yet perhaps most cumbersome, is our new membership application that offers multifactor authentication of the applicant and funding via ACH or EFT. We also offeran online mortgage application that feeds into our loan-origination system for all in-house and secondary-market mortgages.

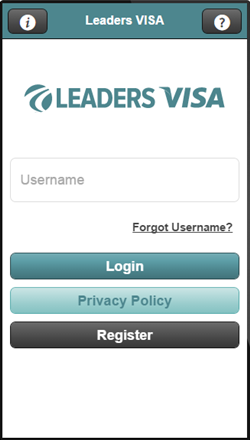

|

| This is the login page for mobile app users at Leaders Credit Union. |

The remaining three applications have been developed in-house: consumer loan which encompass all non-mortgage loans and lines of credit existing member deposit account, and VISA credit card. The in-house applications are essentially webforms that feed into a database in real-time upon completion and are keyed over by our inside sales processors.

Can you describe your digital marketing strategy and its ROI?

JM:We spend approximately $2,000 to $2,500 per month in online ad spend. From that, we typically see a $10,000 to $14,000 return on that spend, allocated among loan mortgage, checking, and credit card app completions. The lions’share of our PPC (pay per click) dollars goes to Google AdWords.

I know there are lots of solutions out there, but Google AdWords has been a good fit for us because it aligns with our Google Analytics account and we can make a 1:1 correlation between spend and return. We have used other solutions like local broadcastersand publishers as well as Zillow, and we’ve evaluated Pandora, but the king of the mountain continues to be Google.

How do you determine that ROI?

JM:With regard to how we assign value, we use a basic conversion metric and we have four attributable goals: 1) checking account, $250; 2) loan, $400; 3) credit card, $100; 4) mortgage, $2,000. These values are based on our estimatedannualized revenue per product.

The mortgage value is our net commission for a sold loan because that’s a little more of a straight-line figure. The credit card value is admittedly low, but we have run a 0% intro rate for the greater portion of the life of our portfolio as we’veworked to build it since 2012.

You Might Also Enjoy

- 4 Ways To Win The War Of The Inbox

- The Matrix From Charlotte Metro Credit Union That Makes Big Data Byte-Sized

- How Altra Credit Union Uses Mobile Technology To Target Younger Members

How have you marketed these lending app capabilities? What has proven to be the most effective and why?

JM: We’ve tried to create continuity and drive usage of the apps by allowing the retail officers to participate in the application as a processing option. The end user has the opportunity to select their favorite representativeto work with after they’ve completed the app. This makes our retail staff more willing to encourage usage of the tools, knowing that they will be able to retain the relationship and credit for the production.

Of course, we continue to leverage fixed-cost channels to promote the convenience of applying online, and as I’d mentioned earlier, we’ve deployed tablets at each branch desk to educate members about the website and what’s availableto them.

|

| This More page shows the other options besides transactions available to Leaders’ mobile bankers. |

We even allow members to complete applications online using the tablets if they’re in queue and we know the wait-time might cause them to abandon their request.

How would you describe your approach and rationale for putting your whole business model on digital channels?

JM:Our approach has been to work diligently toward getting the logistics of traditional delivery into digital, and then begin to shape the experience. For example, in a simple transaction we’re first making sure the actualposting works flawlessly, and then we back into what messaging and graphics the member sees during the process.

Like everyone else in our space, we’re doing everything possible to shift away from a transactional relationship with our members to being viewed as the advisor for their financial household. The more we can do to knit this mobile acquisition strategytogether and make it as functional as the transactional side, the further we will be toward clearing retail space and phone lines for the relationship questions that lead to profitable members.

How about the mobile channel?

JM:On the transaction/advisory continuum, mobile is slanted toward transactional information. Our focus, along with our mobile host, has been to deliver speed and a fluid experience as priority No. 1. A few years ago, we had moreof an la carte model for mobile, but this led to multiple logins for different services.

|

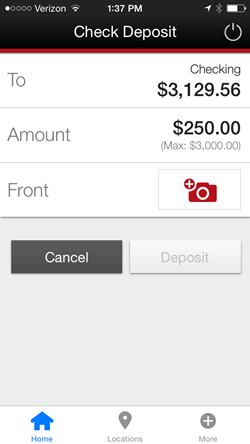

| This is the mobile check deposit page now in use by 20% of Leaders’ mobile app users. |

This model was also placing web-based elements in a native container rather than serving up information directly into the app. Naturally, speed and a fluid experience weren’t possible, so we brought all elements under one umbrella and ensured allinformation was accessible through the native app.

Do you approach it like many major retailers do now, from advertising to checkout, perhaps? How would it differ or resemble that?

JM: It’s difficult for us to model the user flow inside of the online and mobile banking login, but we are evaluating the user flow on the retail side of the site, and this does lead to huge insights about how our members arrive,make purchase decisions, and in some cases, abandon.

Most recently, we’ve opted for a suite of promotional messaging within our online and mobile applications that allows for intelligent prompts. Based on the user’s reported relationships and balances, we can serve up messaging that is relevantto their individual profile and their expected next best product.

How do you know how members are using and responding to your marketing and digital banking tools? How do you know you’re meeting their expectations?

JM:We offer online ratings and reviews through our retail website, and we collect 50 to 75 pieces of feedback every month from our base. To a large extent, the feedback is about technology. This is great for us because whether it’saffirming or indicting, we don’t have to wonder what our members think. People vote with their feet, too, and when we see download/active-use rates climb 10 to 15% net-annualized each month, that’s additional positive feedback.

|

| This is a page that users see when they use a mobile advice to access Leaders’ responsive website. |

The biggest tool I can share that has been a true game-changer has been our ratings and reviews engine provided by Bazaarvoice. After a member opens a new product, this tool generates an email invitation to review and displays the results on our websiteproduct pages.

There have been two key benefits to having the tool: one is the public relations benefit of members sharing their positive experiences. The second has been when there were opportunities for improvement, we had verbatim comments from our members, andwe had nowhere to hide. We had to address those improvement areas. The benefit of the tool extends beyond marketing, into sales, operations, IT, and more.

How did you measure member expectations for each of those mobile products and determine there was a market for them?

JM: Starting with a lean, low-cost option helped in proving the mobile concept. When we first decided in 2011 to release mobile banking, the cost to deliver a native experience was prohibitive and options were limited.

In releasing the la carte option with a mobile-optimized experience inside a native app, we kept costs low and increased the user base quickly. Once we had proof-of-concept and pricing and options had proliferated, weopted for the more robust product.

Nothing that we’ve provided to the members has gone unused. In fact, we have usually regretted not delivering it sooner.

Nothing that we’ve provided to the members has gone unused. In fact, we have usually regretted not delivering it sooner.

Are there products you offer through the website but not on the mobile channel?

JM:We don’t yet offer our personal finance manager, FinanceWorks, through mobile and tablet. We’re working hard to deliver mobile-first user-registration because this is one of the largest pain points for our membersand service representatives. As a workaround, we’ve deployed tablets to each retail branch desk to provide a registration environment for new members until that mobile-first function is available.

How are you using geolocation or other targeting technologies with mortgage lending or any other loan product?

JM: This is a new area for us. We’re preparing to start geo-fencing with some of our larger select employee groups, but the focus might not be solely loan products. We have heard about other credit unions geo-fencing or usingBLE beacons at auto dealerships to provide offers to the member via mobile app push-message. This is something we might explore if our need for consumer auto volume returns.

How much business have you generated through each of those mobile products?

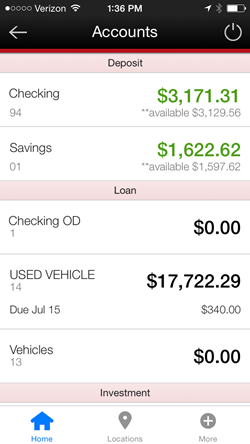

|

| This is a sample account overview page that mobile users get when they access Leaders from their smartphones. |

JM: Unfortunately, because our apps are mobile-responsive and we have dedicated URLs for them, there is no way for us to track whether the application is being filled from our mobile app or simply from a mobile browser through ourretail website.

Further, because they are web forms, we track hits to the actual HTML page, then app starts, abandons, completions, and funded loans to create a funnel, but we’re not quite as concerned with measurement of source at present.

If there were an ongoing cost associated with delivering the applications through mobile, I believe the impetus would be stronger for measuring ROI, however there is not.

How much growth have you seen?

JM: Our app starts through the online/mobile channel have been pretty straight-line over the past year. We’re in the maturity phase of the service, with about 100 completed loan applications and about 50 member and non-membercombined deposit applications each month on average.

The fact our apps are mobile-optimized gives us an opportunity for growth as the trend shifts toward purchases via smartphone, but where I believe we’ll continue to drive innovation is in the area of discovering ways to limit data entry.

I don’t have production goals or projections as much as aspirations to improve the end-user experience. I believe once we’ve solidified the experience, the true growth will come.

The fact our apps are mobile-optimized gives us an opportunity for growth as the trend shifts toward purchases via smartphone, but where I believe we’ll continue to drive innovation is in the area of discovering ways to limit data entry.

What did you learn as you went from one app to the other? What kinds of things did you learn that you could apply to the next app?

JM:In moving from our legacy application to our current platform, we discovered members appreciated the unified login and snappier interface. We have, however, had to be cognizant of our legacy device user base.

We’ve hesitated to opt for the latest release of each application wave because we operate in a rural, late-adopter market. However, many of our end users are abandoning their desktop PCs for their mobile devices as a primary computing option,and this presents an enrollment issue.

Finally, we’ve learned the irritation threshold is fairly low for mobile, and we have to design for the lowest possible denominator to delight the end user.

Many of our end users are abandoning their desktop PCs for their mobile devices as a primary computing option, and this presents an enrollment issue.

|

| This is the home page for credit card users through Leaders’ mobile channel. |

On the lending side, we have to manage a tension between what information our sales staff and underwriters need in order to make a decision and what the end user is willing to provide and the subsequent time involved in providing the information.

We’re constantly searching for opportunities to auto-fill and use skip-logic to omit unnecessary questions. Modern browsers like Google Chrome are an excellent resource for this because they tend to store regularly used information.

What’s next?

JM: In the next 60 days, we will be releasing P2P payments. In the next 120 days, A2A payments. In terms of functionality enhancement, we also plan to release mobile-first user registration end-users must currently enrollthrough Internet banking first and fingerprint authentication for login. Additional biometric options like facial recognition will likely be ready before year-end.