Credit unions commonly use deposits as a funding mechanism for higher-earning loan products. But deposits provide value beyond liquidity. They engage members and provide cross-selling opportunities, too.

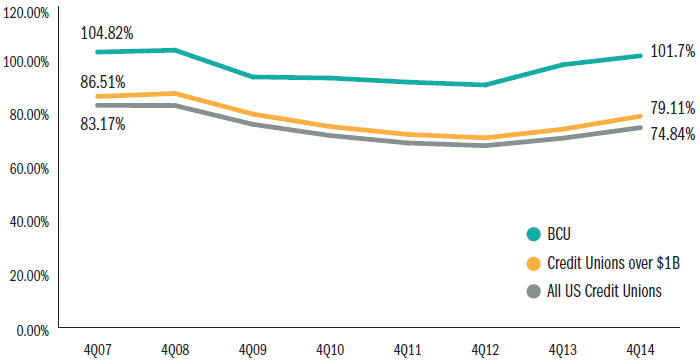

Historically, BCU ($2.1B, Vernon Hills, IL) has focused on the lending side of the balance sheet, as evidenced by its roughly 102% loan-to-share ratio.

The credit union’s total loan portfolio has grown approximately 10% every quarter since the second quarter of 2012 outpacing its asset-based peer group but BCU is taking steps to even things out.

We assessed whether there’s value in focusing as much on deposits as loans; the answer was clearly yes,’ says Ken Dryfhout, director of balance sheet management at BCU. They go hand in hand from a liquidity perspective you need the dollars if you are going to lend them but also in terms of synergies.

Increasing deposits requires success in a number of variables, including a willingness to change and adapt. Here are four rules BCU follows to build its deposit portfolio.

Loan-To-Share Ratio

Data as of 12.31

Callahan & Associates | www.creditunions.com

Source: Callahan & AssociatesPeer-to-Peer Analytics

Historically above peer and industry averages, BCU’s loan-to-share ratio underlines the institutions’s recent loan growth and shows the importance of the deposit portfolio.

Focus Your Efforts

More than one year ago, BCU created a manager of deposit products position to reinvigorate deposits and hired community banker Brett Engel to fill the role. Engel’s hiring underscored CFO Tom Moore’s commitment to deposits.

He’s always talked about how the most successful retail financial institutions have a successful deposit program as a foundation, Dryfhout says of Moore.

CU QUICK FACTS

bcu

data as of 12.31.14

- HQ: Vernon Hills, IL

- ASSETS: $2.1B

- MEMBERS: 195,230

- 12-MO SHARE GROWTH: 9.80%

- 12-MO LOAN GROWTH: 13.51%

Dryfhout and Engel have spearheaded BCU’s deposit growth efforts, which have included pushing for more evenly distributed resources between deposits and loans. For example, its average cost of funds is 0.08%, meaning for every $1 deposited, thecredit union spends $0.08 on higher interest rates and larger dividends. That’s higher than the average of its peers $1 billion to $3 billion in assets.

It’s a matter of making that commitment, understanding the value, and trying to get deposits ramped up to the degree we’re doing on the lending side, Dryfhout says.

BCU values relationships, especially those with some transactional component, such as a checking account. Specials on certificates of deposit (CDs) can collect millions in deposits, but they don’t engage members. Checking accounts, however, requirethe member to keep BCU top-of-mind every time they use the account. These members are more likely to consider other BCU products or services.

To track the performance of BCU’s deposit portfolio, Dryfhout and Engel have created an internal deposit dashboard. The central reporting repository allows branch managers at the institutions’ 39 locations to compare their performance againstone another using metrics such as checking penetration and checking activation, among others.

We want to drill into the individual branches to see their production level, Engel says. We want to get data into the hands of the people who have the ability to turn that data into action.

The institution’s commitment has contributed to 9.8% share growth year-over-year.

Push For Early Activation

BCU believed, and now has the data to show, that members with deposit relationships are more engaged.

BCU members with both active checking and credit card accounts transactional relationships are more than twice as likely as members without those accounts to take out an auto loan, mortgage, or HELOC; set up direct deposit; or use onlineand mobile services, says Dryfhout. BCU defines an active checking account as one that has at least one transaction and a cumulative $500 deposit within the first 60 days of activation.

Although it does track activation over time, BCU focuses on new products to ensure it is engaging members up front, Dryfhout says. It’s worth more to the credit union in terms of effort and resource allocation to make sure members activate new productsimmediately rather than revisit inactive accounts months later.

|

| The main tab of the deposit dashboard that allows users to examine perfomance by branch or SEG. |

Dryfhout and Engel rely on BCU’s front-line staff, which interacts with members most frequently, to encourage activation. To want to do that, they must understand the value of deposit products for the institution a growing deposit base translatesinto more efficient marketing and outreach and the ability to leverage engagement data for cross-sell opportunities.

They have to understand why we are making investments and marketing the way we are to grow this part of the balance sheet, Dryfhout says.

Set A Goal

BCU continuously monitors its members’ needs and develops products to meet them. Today’s members have diverse needs, and the credit union looks at purchase decision variables such as functionality, price, and convenience to determine how wellit is meeting those needs.

Convenience continues to climb up the ladder in terms of what members desire, Dryfhout says.

Responding to member demands for functionality and simplicity, the credit union has plans to consolidate two of its premium checking products, its Power Interest and Total Access Checking accounts, into a single product by late first quarter 2015. Thenew product will offer high yields and reimbursements for ATM surcharges, which are common at local banks and credit unions already, Engel says.

We recognize that our checking sales pitch is long-winded and confusing when comparing the two accounts, Engel says. We think the consolidation will help alleviate this confusion as well as provide additional value to our members.

The credit union does not yet have a penetration, activation, or usage goal for the consolidated product, but the account plays a large part in BCU’s 14% checking balance growth goal in 2015.

Increase Internal Visibility

BCU has a strong internal sales culture, and loans receive the most attention at the institution’s monthly organization-wide sales meeting.

If we value deposits on par [with loans], they should be getting as much air time, Dryfhout says.

So Dryfhout and Engel looked for a way to increase visibility and knowledge of deposits that was easy to put together, approachable, and allowed employees to interact with the information on their own time.

The duo now produces five- to 10-minute videos every month and releases them internally to staff. The videos update viewers on the performance of the deposit portfolio from an institutional and branch level. Employees enjoy watching these light, personablevideos as much for the personality as the information.

The videos allow the organization to get to know us and what we’re trying to do, Dryfhout says. They’ve lowered potential barriers that would otherwise be in place and sped up the time we’ve needed to increase ourvisibility.