Every time a member opens an account, applies for a loan, or uses a credit union service, data trickles in that credit unions can translate into reports. Those reports, when properly sliced and diced, offer business intelligence that cooperatives can use to hone strategy and improve member value.

Oregon Community Credit Union ($1.5B, Springfield, OR) has more than 100,000 members and nine branches in and around Eugene, OR. It is a forward-thinking financial institution that is aggressively aggregating and parsing membership data in a way that steps into the crystal-ball realm of predictive analysis.

CU QUICK FACTS

Oregon Community Credit Union

Data as of 03.31.16

HQ: Springfield, OR

ASSETS: $1.5B

MEMBERS: 134,616

BRANCHES: 9

12-MO SHARE GROWTH: 9.65%

12-MO LOAN GROWTH: 4.64%

ROA: 0.56%

The approach goes beyond the ABCs of demographics. According to chief financial officer Ron Neumann, it is a way to examine how members engage with the credit union, what makes them profitable, where they conduct transactions, and how that all is changing over time.

That means taking OCCU’s member data beyond trending and into creating models that predict where deposits, loan, and other products could be heading, says Dave Schiffer, director of finance for Oregon Community.

The appetite of the organization was such that it was a great time to step into that, Schiffer says. More people were looking into [predictive analysis] as they were getting more familiar with the data. I think there was a strong appetite for data all along.

Start At The Core

The credit union’s implementation of business intelligence started with member and account-level data it pulled from its core, says Dustin Hahn, senior business intelligence analyst at Oregon Community.

We then began adding additional core data such as transaction, general ledger, and collateral along with introducing non-core data like loan origination system data and credit card processor data.

The system grew more or less on the fly.

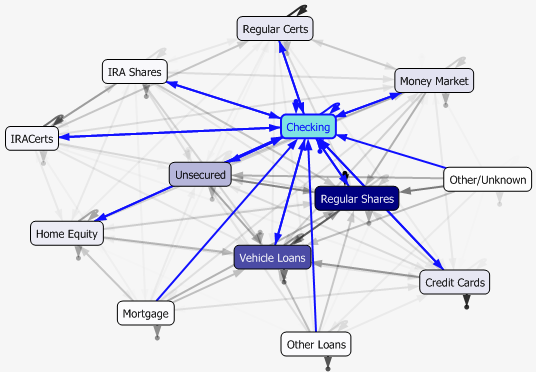

We can use data to show the member, who is already in certain channels, what the logical next best product would be.

We didn’t have the luxury of dedicating a programmer specifically to this endeavor, Hahn says. As we received new requests we incorporated them within our warehouse. We started with the member, account, and relationship dimensions and have continued to expand on them.

Ron Neumann, Chief Financial Officer, Oregon Community Credit Union

According to Hahn, the credit union’s data warehouse is set up so different departments can serve themselves and pull the reports relevant to their needs.

For Deborah Mersino, chief marketing officer, it enables an informed next-best-product approach that looks at past and trending data as well as aggregate member data i.e., the behavior of other members with similar profiles to suggest what this member might need next.

We can use data to show the member, who is already in certain channels, what the logical next best product would be, Mersino says. We can serve up that product in real time based on a predictive model that anticipates their needs in real time. We’re at the beginning and it’s proving successful.

Dave Schiffer, Director of Finance, Oregon Community Credit Union

Statistical modeling, such as cluster analysis, is one of the essential tools here, Hahn says.

We look at members’ adoption rates to certain products so we can determine, for example, that a member of this classification usually adopts a credit card after they’ve had a checking account for this many months, the intelligence analyst says.

Adds Schiffer, Once we do that modeling, we can focus on members who are likely to be the most responsive, who are at that point in their product journey where they’ll be most open to that offer.

Thus, instead of sending out thousands of direct mail credit card communications, marketing can create a prospect list based on the likelihood of adoption as indicated by predictive analysis and cluster modeling.

Deborah Mersino, Chief Marketing Officer, Oregon Community Credit Union

By being so targeted, you market to a smaller list and bring down acquisition costs significantly, Mersino says. Whereas in the past it cost us hundred of dollars per card, it now can be as low as $66.

Each time a member responds or doesn’t the credit union tweaks the data to achieve an even finer degree of insight.

Ultimately, the goal is to create analytical models for next-best-offers or products for each member. To that end, Mersino says, Oregon Community is implementing Adobe Analytics, Adobe Target, and Adobe Campaign, a suite of real-time marketing and reporting tools.

Oregon Community uses models like this to determine a next-best scenario for members.

That will allow us to serve up marketing offers and do analysis in additional ways, she says. Adobe Campaign will allow us to do trigger campaigns. For example, once a member gets an indirect loan, the predictive model says they are good candidates for a checking account or something else. This would automatically produce that offer in email or serve it up to them on the website.

According to Hahn, that’s the next question how to serve the offer.

We have all these models set up internally, Hahn says. And it’s about getting the information to the member who might accept it and use it.

If credit unions are beginning to plumb the implications of business intelligence and predictive analytics, the rest of the corporate world isn’t far ahead.

Save Time. Improve Performance.

NCUA and FDIC data is right at your fingertips. Build displays, filter data, track performance, and more with Callahan’s Peer-to-Peer analytics.

According to an August 2015 CreditUnions.com article, research shows only 15% of Fortune 500 companies have the systems in place to crunch big data and put it to competitive uses such as molding customer behavior. But that is quickly changing. The same article says from a base of $40 billion in 2015, data investment is projected to grow at 14%through the decade’s end.

For today, Schiffer is pleased with Oregon Community’s progress.

We have a warehouse that houses a lot of data we’ve been modeling, he says. As we run the campaigns, the data grows. Adobe gathers the information as people respond and don’t respond and we continue to learn who is likely to respond to given offers. Once they become a member, we have all that info behind the scenes.

Looking beyond its current membership, Oregon Community also uses outside marketing lists to determine whether certain behaviors might predict someone has a higher propensity to open an account, Schiffer says.

So what’s the one thing the credit union’s employees said they would do differently if starting again?

We would have started sooner, Hahn says.

You Might Also Enjoy

-

What Does Business Intelligence Mean for Credit Unions?

-

How A Governance Committee Helps Langley FCU Tackle Business Intelligence

-

How Analytics Can Drive Efficiency And Innovation

-

KEMBA Financial Knocks Down Silos With Shared Data Ownership