Many of you may recall our four-day loan sale of last January.We set it in motion on January 31, the day the Federal Reserve announced it was dropping interest rates 75 basis points.We had already made up advertisements, which hit the airwaves within hours of the Fed’s statement. We offered rates as low as 3.95% on any secured loan, real estate, or refi, guaranteeing the rate for five years.

People taking theloans would be required to have a direct deposit checking account with the credit union. We were hoping for $35 million in new loans but got 2,000 calls on the first day, leading to over 3,000 applications for $158 million. We approved 93% of theapplications for $149 million in loans. Thirty-one percent of applicants were new members, who opened 696 new direct-deposit checking accounts with us. Seventy percent of the $149 million was new money. Not all of the loans were written at 3.95%,of course. The average rate was 4.27%; for auto loans it was 5.03%.

One Year Later

Now a year has gone by and we can look back to see how things have been working out. I’ll give a summary.

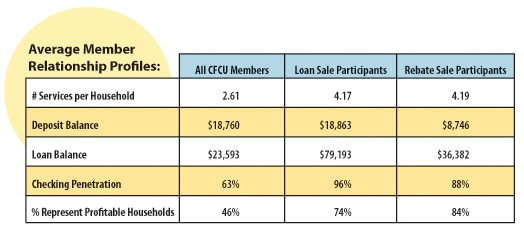

The four-day loan sale members are more profitable to the credit union than average members. Of the four-day loan sale member households, 74% are profitable for us, compared to 46% for all CFCU member households. Loan sale borrowers also use moreof our services than do the average, 4.17 services to 2.61 per household. They maintain a slightly higher deposit balance, $18,863 to $18,760. They hold higher loan balances, $79,193 to $23,593. Almost 90% of them hold three or more services withus compared to 45% for all CFCU member households, and 96% have their checking with us compared to 63% for all CFCU households. In all, the four-day loan sale members created a perhousehold profit of $1,203 as of the end of March last year, vs. $917created on average by all CFCU member households.

The demographics of those people who were attracted to and participated in the four-day loan sale were: 23% middle market customers, 46% credit driven, 19% upscale, and 10% middle income depositors. Looking at fourday loan sale member household productpenetration, we have as follows by year-end 2008: Free checking, 49%, Relationship checking, 38% ,Used Auto loan, 36%, Home Equity loan, 73%; and Platinum credit card, 26%. All of these figures are higher at year-end than when we first measured thisinformation at the end of March 2008 except for the Home Equity loan participation which was 1% lower at year-end than it was two months after the loan sale.

April-May Rebate Sale

We followed up the four-dayloan sale with a springtime Rebate sale starting April 15. Members could receive a 1% cash rebate up to $500 on personal secured loans vehicles, campers, boats, etc. Real estate loans, signature loans, student loans, business loans, and creditcard lending were not eligible. Five thousand dollars of new money was required for the rebate. Rates could be as low as 4.99%. Vehicles had to be a 2003 model year or newer; older ones could qualify for the rebate, but at standard loan rates.

We ran this promotion from April 15 to May 17. It brought in 539 loans for $7.5 million at an average yield of 5.8%. By far the most loans were for used cars there were 376 of these, 51 loans for new cars, 44 for motorcycles, 29for boats, motor homes or trailers, and 39 were for other personal secured loans.

These borrowers are also good members for us. More than 84% represent profitable households. The average borrower from this promotion uses 4.19 of our services.Checking penetration is 88%; average retail deposit is $8,746 and average retail loan balance is $36,382. Our analysis of the characteristics of the persons taking advantage of this promotion is as follows: Middle market 32.7%; credit driven 25.6%;upscale 21.4%; middle income depositor 10.8%; fee-driven 7.5%; and low income depositor 1.8%.

Leading with loan sales was a profitable strategy for us in 2008 – one that helped to introduce new members to CFCU and deepen relationshipswith existing members. Our ROA last year was 1.17%. Our assets grew $222 million or 23.5% to $1.69 billion, our deposits grew 24.3%, our loans grew 22.4%, our members grew 7.5% to 80,872, and our capital grew 15.7%.