Total credit card balances at credit unions nationwide rose 8.1% year-over-year to top $53.6 billion as of June 30, 2017. Annual balance growth has surpassed 7.0% in five of the past six quarters, and second quarter 2017 growth was the highest of the past 11 quarters. Credit cards accounted for 5.8% of the $923.2 billion credit union loan portfolio at mid-year.

Also at mid-year, 17.3% of members held a credit card with a credit union. Credit card penetration was 20 basis points higher than it was in the second quarter of 2016. The average credit card balance reached $2,792 in the second quarter, an increase of 3.1% year-over-year.

Credit unions in all the NCUA regions save the Southeast posted growth in average credit card balances in the second quarter. The average credit card balance was highest for credit unions in the Mid-Atlantic region. Average balances there were $4,193. Mid-Atlantic credit unions also had the highest penetration, at 22.8%. On the other end of the spectrum, penetration for Central region credit unions came in at 14.5%. ContentMiddleAd

Balances and penetration rates have increased, but credit card utilization has not. Usage declined 36 basis points annually, dropping from 31.5% at mid-year 2016 to 31.1% in 2017. Unfunded commitments rose nearly $11 billion in the same time frame.

Over the past 12 months, credit card delinquency increased 15 basis points to 1.08%. Although credit card delinquency increased year-over-year, it has improved 6 basis points compared to the end of 2016. Additionally, at 1.08%, credit card delinquency at credit unions is still considerably lower than FDIC-insured institutions, which reported second quarter credit card delinquency of 2.47%. This is even more compelling given credit unions classify loans as delinquent when they surpass 60 days past due, whereas banks use a 90-day window.

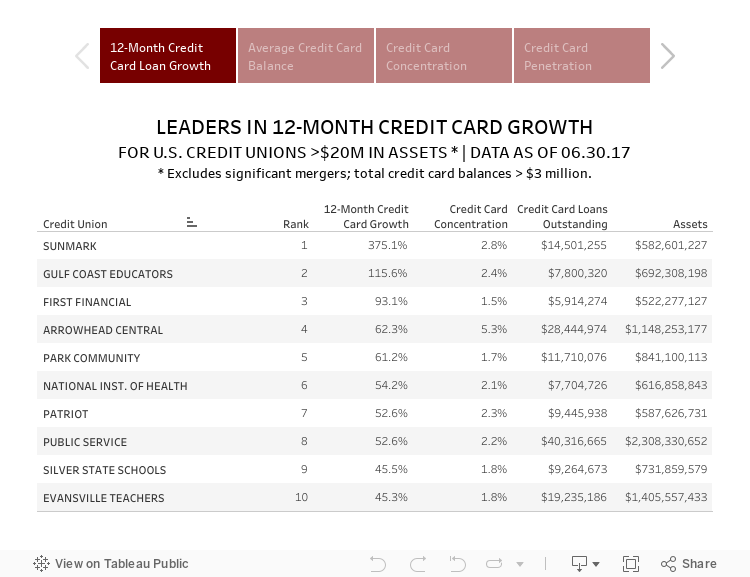

Click through the tabs below to see the top 10 credit unions in each leader table.

var divElement=document.getElementById(‘viz1514326698955’); var vizElement=divElement.getElementsByTagName(‘object’)[0]; vizElement.style.width=’750px’; vizElement.style.height=’577px’; var scriptElement=document.createElement(‘script’); scriptElement.src=’https://public.tableau.com/javascripts/api/viz_v1.js’; vizElement.parentNode.insertBefore(scriptElement, vizElement);

var divElement=document.getElementById(‘viz1514326698955’); var vizElement=divElement.getElementsByTagName(‘object’)[0]; vizElement.style.width=’750px’; vizElement.style.height=’577px’; var scriptElement=document.createElement(‘script’); scriptElement.src=’https://public.tableau.com/javascripts/api/viz_v1.js’; vizElement.parentNode.insertBefore(scriptElement, vizElement);

See the rest of these tables and explore dozens more along with hundreds of pages of credit union performance data in the 2018 Callahan Credit Union Directory. It’s the gold standard for reliable insight. Read the digital download today.

CASE STUDY

Cashing In With Credit Card Rewards

InFirst FCU | Alexandria, VA | Assets: $172.8M | Members: 11,555

InFirst Federal Credit Union took inspiration from retail giant Costco when the suburban Washington, DC, credit union launched a new credit card rewards program.

We looked at Costco and said we wanted to do one better, says Jeff Parish, the credit union’s chief marketing officer.

The world’s second-largest retailer rolled out its own new Visa card in 2016. InFirst’s new Visa rewards credit card mirrors that program, only without the annual fee. The credit union’s Visa rewards card offers 4% cash back on allgas purchases; 3% on all restaurant and travel; 2% cash back on all grocery stores, superstores, and wholesale clubs; and 1% cash back on all other purchases.

Rewards stimulate the use of the credit card and bring in additional members, Parish says. And then there’s interchange income from card use as well as interest income from those people who carry a balance.

The card has an introductory rate of 1.99% for six months that then adjusts to between 10.90% and 17.90%. The credit union’s Young Adult Visa Rewards card for 18- to 25-year-olds offers the same rewards benefits and introductory rates and noannual fee. However, cardholders do not need a credit score to qualify, and when they turn 25 their accounts convert into the regular portfolio.

As for getting the word out, the credit union relies on a combination of old school and social media outreach.

For us, the most effective form of marketing is digital mail, Parish says. But it’s hard for us to find people who are not already members.

Social media also has proven to be an effective channel, with personal reviews attracting more business than self-promotion.

Finally, the credit union offers a tool on its website, mobile app, and social media presence that calculates savings for members switching to the new credit card. All this has contributed to a growing base of card users.

We don’t have nearly 100% penetration with our members, but the number of credit cards we issue continues to grow, Parish says. Each time we do a promotion we see a nice bump our number of cards.

Read The Whole Story

How Do You Compare?

NCUA and FDIC data is right at your fingertips. Build displays, filter data, track performance, and more with Callahan’s Peer-to-Peer analytics. More insightful performance comparisons start here.

![]()