The new year is nearly upon us, and as the first quarter comes into view, so does the expectation of deposit growth, the annual influx of funds needed to buttress loan growth and the critical income it produces, even in this decade-plus stretch of narrowloan margins.

As Callahan & Associates co-founder Chip Filson notes here,Most of the share growth for credit unions occursin the first quarter of each year. And, he adds,With one minor exception, the first quarter of each year is the only quarter from 2012 through 2014 when shares grew faster than loans.

Total shares in the credit union system, meanwhile, crossed the trillion dollar mark for the first time in the third quarter, as noted in Callahan’s latest Trendwatch webinar,with share growth even surpassing member growth.

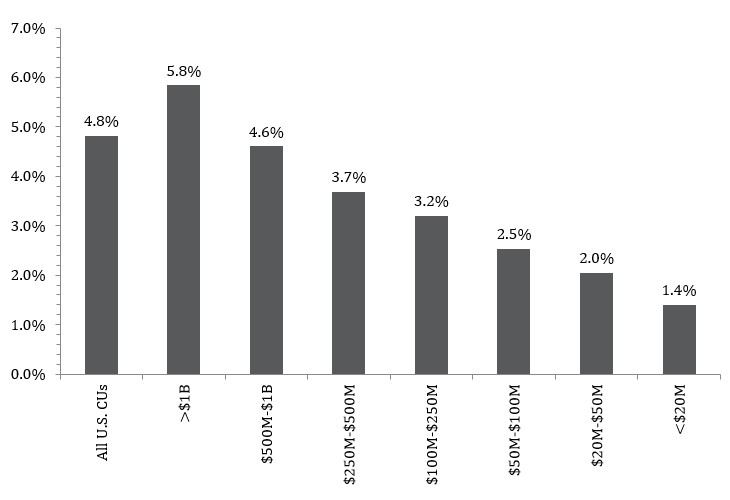

As it turns out, though, the larger the credit union, the more likely it was to show decent share growth so far in 2015, as the chart below shows. In fact, the growth rate declines neatly from the largest asset class to the smallest in the Callahan database.

YTD Share Growth

For all U.S. credit unions | Data as of 09.30.15

Callahan & Associates | www.creditunions.com

Source: Peer-to-Peer Analytics by Callahan & Associates

But regardless of size, everyone needs deposits, and ways to attract them are myriad. How to attract deposits, in fact, is a popular subject at CreditUnions.com. Here are five in-depth looks at how different credit unions took different approaches todoing just that.

We assessed whether there’s value in focusing as much on deposits as loans … you need the dollars if you are going to lend them.

How To Handle TheHot Money

Timing can be everything.Ent Federal Credit Union($4.2B, Colorado Springs, CO) found that out after launching a 50th anniversary certificate special six years ago, just beforethe onslaught of the Great Recession. The rapid drop in market rates during the two-month promotional period after the January 2009 launch caused demand to spike much higher than the credit union anticipated. Ent brought in $80 million in new money,which grew to $143 million by the time the certificates began maturing in 2014. MJ Coon, the credit union’s chief financial officer, says $46 million inhot money exited the credit union as the certificates matured, but that carefulmanagement made the hit on net interest margin from the special rates tolerable. Find out more here.

Healthy Growth With HSAs

Elements Financial Federal Credit Union($1.1B, Indianapolis, IN) has found that health savings accounts are a workplace benefit appreciated by many of its nearly 80,000 members.A bonus: HSAs have the salutary secondary effect of boosting deposit growth, too, since unspent money in those accounts roll over each year. The Indianapolis credit union which changed its name last year and still serves primarily employeesof pharmaceutical giant Eli Lilly has more than 7,000 HSAs in effect now, with balances nearing $10 million earlier in the year before the heavy payout period began. The accounts are a great way to build relationships, as well as deposits,especially with the opportunity to go into SEGs for educational sessions on the accounts. Get the whole HSA diagnosis here.

Early Pay A Sticky Way

Digital Federal Credit Union($6.0B, Marlborough, MA) has long been crediting members’ accounts when it receives the deposit notice instead of when the money actually arrives. The move costs the credit union a day or two of lost interest and use of that money, and the impact of that kind of goodwill can be hard to quantify, but there are some numbers that can help. For example, according to Callahan data earlier this year, DCU boasted member penetration of 39.7%, compared with 8.25% on average among the nation’s 228 billion dollar credit unions and 5.40% for all 6,400 or so credit unions nationwide.I’ve been here 20 years, and we were doing early pay when I arrived, senior vice president for marketing and strategy Tim Garner says.We know it sets us apart from other financial institutions. More on that here.

Four Ways To Double Down on Deposits

Aggressive lenders need a steady flow of new deposits.BCU($2.3B, Vernon Hills, IL) stays around 100% loaned out, and knows that well. The Illinois credit union follows four rules for keeping the cash available: Focus your efforts, push for early activation of checking and card accounts, set goals, and increase internal visibility of those deposit goals in the internal sales culture.We assessed whether there’s value in focusing as much on deposits as loans; the answer was clearly yes,says Ken Dryfhout, director of balance sheet management.They go hand in hand from a liquidity perspective you need the dollars if you are going to lendthem but also in terms of synergies. Here BCU details its four ways to focus on deposit growth.

Growing Deposits By Facing Down High-Fee Competitors

First Imperial Credit Union($83.7M, El Centro, CA) helps grow deposits by offering alternatives to high-fee check cashers and payday lenders in an agriculturalarea where a lot of people don’t have a lot of money to spare.To encourage direct deposit and help members build a relationship with a traditional financial institution many for the first time the credit union offers astarter checking account that provides direct deposit and a debit card for $10 a month, a fee that shrinks over time. And if $10 sounds pricey,add up those fees they’re paying elsewhere, and we charge a hell of a lot less, sayscredit union CEO Fidel Gonzalez. In the past six years, total checking accounts of all kinds have grown from 3,500 to 5,200, about one-third of First Imperial’s membership. Share growth also has exceeded its asset-based peer group. There’s more here.