The COVID-19 pandemic has resulted in the slowdown of the global economy. Domestically, economic shutdowns have created uncertainty about the future financial impact on U.S. businesses and consumers. The Dow Jones Industrial Average fell more than 25% in March, the sharpest decline since 2007. To slow consumer pullback, the Federal Reserve cut interest rates twice in March, to between 0.00% and 0.25%. This prompted an influx of liquidity and helped the markets rebound. However, it also compressed margins and led to revenue pressure for lenders.

Key Points

- Total first quarter revenue at U.S. credit unions surpassed $20 billion, the highest level through March on record. However, year-over-year growth of 4.7% was the lowest rate since 2014.

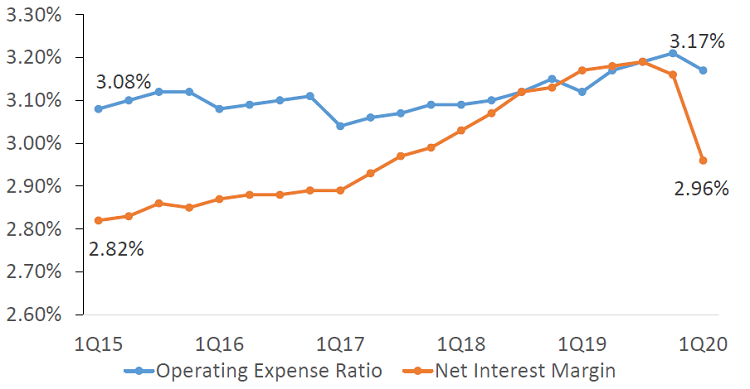

- The net interest margin fell 21 basis points year-over-year to 2.96%, the first annual decline since 2013.

- Interest income hit a first quarter high of $15.4 billion. This is up 3.2% annually, the slowest growth rate since 2014. In contrast, non-interest income rose 9.6% annually to $5.2 billion as credit unions emphasized alternative income streams.

- Operating expenses hit a year-to-date high of $12.8 billion, 9.5% higher than the first three months of 2019.

- The industry’s average net worth ratio was 11.0% in March, down 12 basis points from last year.

TOTAL REVENUE AND ANNUAL GROWTH

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.20

Callahan & Associates | CreditUnions.com

Net interest margins plummeted in the first quarter as the Federal Reserve rate cuts reduced spreads.

NET INTEREST MARGIN VS. OPEX

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.20

Callahan & Associates | CreditUnions.com

Fee and other operating income increased 4.5% and 13.7%, respectively, as credit unions supplemented slowing interest income via alternative revenue streams.

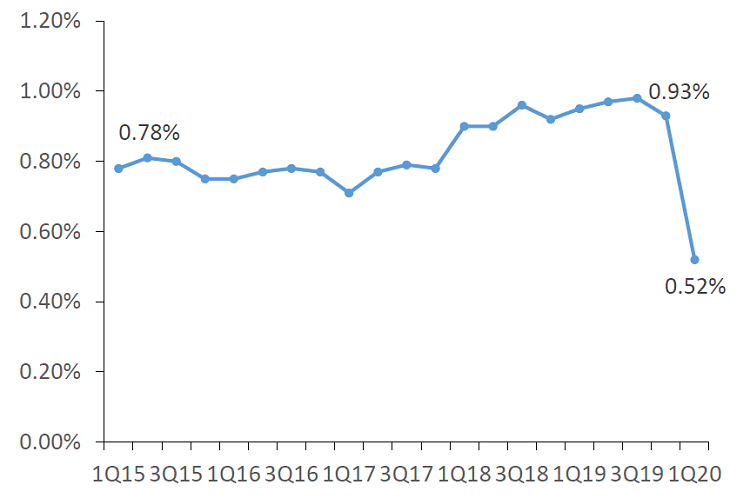

RETURN ON ASSETS

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.20

Callahan & Associates | CreditUnions.com

A compressed interest margin and increased provision expense caused ROA to drop 43 basis points annually, the largest year-over-year decline since 2009.

The Bottom Line

A locked-down economy combined with volatile changes in monetary policy put lenders in a difficult position in the first quarter of 2020: total revenue growth slowed as sources of income shifted away from interest-driven streams. Additionally, the industry’s collective provision for loan loss was up 33.4% from this point last year. The decision to allocate more funds to cover future losses impacts earnings in the near term; however, it also shows how the industry is preparing a cushion of liquidity for an uncertain future.

Without official data from the NCUA, Callahan is reporting first quarter data trends from institutions that represent 99.7% of the industry’s assets.

This article appeared originally in Credit Union Strategy & Performance. Read More Today.