Google isn’t the only business bringing a Silicon Valley ethos to the Midwest.

The technology company raised eyebrows when it chose the Kansas City metropolitan area as a launching pad for its move into broadband Internet and cable television. Google Fiber went live in Kansas City in 2012. That same year, Brandon Michaels became president and CEO of Mazuma Credit Union ($524.3M, Overland Park, KS).

Michaels is a third-generation credit union manager who served as the vice president of finance at San Francisco Fire Credit Union before joining Mazuma in 2009 as chief financial officer. Perhaps true to his Golden State roots, his vision for Mazuma is more reminiscent of a California start-up than a traditional financial institution, but it is serving the credit union well.

Mazuma has always aspired to be bigger and better than it currently is, Michaels says.

This is the story of how Mazuma is turning aspirations into reality.

Did You Know?

Mazuma is a Yiddish word for money. The credit union took on that new name in 1998, part of what it jokingly refers to as a mid-life crisis.

Dismantling Silos From The Top Down

CU QUICK FACTS

Mazuma Credit Union

Data as of 06.30.15

- HQ: OVERLAND PARK, KS

- ASSETS: $524.3M

- MEMBERS: 55,444

- BRANCHES: 25

- 12-MO SHARE GROWTH: 5.63%

- 12-MO LOAN GROWTH: 9.38%

- ROA: 0.71%

When Michaels joined Mazuma which was founded in 1948 and formerly known as Federal Employees Credit Union before rebranding under its current moniker creative stagnation, analytical deficit, and operational silos had grown so strong that senior staffers rarely knew what was going on outside their office walls.

This was no way to respond to a market that demands agility, so when Michaels became CEO, he led a re-organization of the institution that included replacing nearly all the C-level managers, adding to and enhancing the vice president roster, and implementing a new, institution-wide culture that not only encourages but in fact inspires collaboration.

And to address those silos, Mazuma now has roles dedicated to the effective flow of information among various parties.

Silos don’t work, Michaels says. As I built out my own leadership team, I looked for people I knew would not have that management style. We don’t have a complex mission or vision statement, so the ongoing purpose for all of us is the same to make Kansas City a better place to live, work, and bank.

According to Mazuma’s chief operating officer, Deonne Christensen, the executive leadership team now works together to prioritize all projects rather than presenting pet issues independently and competing for resources on a per-department basis.

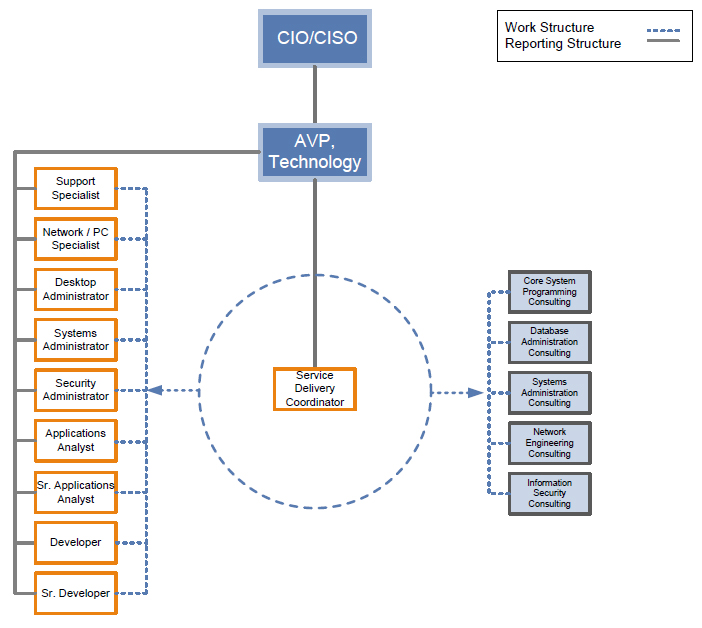

Mazuma Technology Team Org Chart

This example provided by the Mazuma technology team shows how a staffer in the middle facilitates collaboration across their team and up the ladder.

In support of this unification, executives jointly create their Rally Cry, a document that outlines the organization’s current most important objectives and shows how their programs and initiatives, both current and desired, contribute to those goals.

Loan growth is currently one such front-and-center priority. Consequently, the credit union posted 9.4% year-over-year growth in this metric as of second quarter 2015, according to data from Callahan Associates.

Growing With Its City, Standing By Its Members

This new era of soul searching has also caused Mazuma to boil down its institutional identity into a simple, timeless mandate for both employees and its more than 55,000 members: Bank Happy.

Happiness is a state of mind to be sure, but the right location doesn’t hurt either, which is why Mazuma also considered not just how it served its members but from where.

In early 2015, the credit union left the headquarters in midtown Kansas City, Missouri, that it had called home for more than 30 years and opened its first new branch in a decade, located in the neighboring suburb of Overland Park, Kansas.

We don’t have a complex mission or vision statement, so the ongoing purpose for all of us is the same to make Kansas City a better place to live, work, and bank.

Overland Park is the second-largest city in Kansas, with an estimated population of 184,525 in 2014. Its per capita and household incomes are above the metro area’s averages, while its cost of living is below national levels. It also skews young, with an average resident age of 37.8 in 2012, according to the American Community Survey.

An inside look at the credit union’s new digs.

The credit union’s new 53,000-square-foot building is located in an upscale office and retail development. The building itself is brimming with personality, including conference rooms with Steam Punk, Lego, and underseas themes, easy-on-the-eyes terraces and glass-walled offices, and staff amenities that include exercise facilities, a nursing room, and even a ping pong table.

Our longtime members told us, We’ll give you this, but you cannot slack off on the service; you can’t do this at the expense of my money or my trust, says brand manager Andy Dickhut. So everybody here knows we have to deliver excellent service in return.

Indeed, the facility’s hip look is a constant reminder of Mazuma’s vision to more effectively serve its target audience of 18- to 45-year-olds. However, it is still an effective headquarters for maintaining and growing the flip side of the credit union’s operations its numerous, innovative services designed to serve historic, lower-income markets within Kansas City proper.

To date, these include a mix of payday lending alternatives as well as ATMs and best-of-breed online and mobile services.

When Less Is More

While currently serving both areas of opportunity and areas of need, Mazuma aims to reach 70,000 members and $700 million in assets by 2020.

As of midyear 2015, it has 55,444 members and $524 million in assets.

Mergers are a possibility to meet this goal, Michaels says, as are expansions into territories around its hometown. Yet this desired growth won’t come at the cost of operational nimbleness.

For example, at the member-facing level, all front-line service responsibilities fall primarily to two groups: Mazuma’s branch-based universal agents and its centralized e-branch staff. The former are trained to handle multiple products and services in the branch and call center, from opening new member accounts to closing loans, and the latter are there when members need help with mobile and online applications, as well as to support ACH and wire transactions.

But these team members aren’t just in control of all member interactions, they are in control of their own professional destinies as well. That’s because motivated individuals from both groups have on-demand but optional access to training and examinations that can increase the scope of their responsibilities and provide bumps up the pay scale. Exam results also can help employees join issue-oriented special ops groups or even potentially open the doors to careers in other areas of the organization.

In addition, while the credit union is not currently as operationally efficient as some of its comparable peers, it’s looking to enhance performance there by shrinking the physical footprint it needs to serve members, both at the new headquarters and among its network of branches.

We’re empowering our people to empower our members to take advantage of the best financial products and services in the Kansas City market, Michaels says. Both physical and cultural transformation are a huge part of this , and we’re well on our way.