Credit unions have played a crucial role in the ever-changing financial services industry, especially in commercial lending. In 2023, this trend continues with a significant increase in digital transformation to stay competitive and support growth. Exploring the challenges faced by credit unions when adopting technology-driven business models, it becomes evident how integrated solutions can help them scale their commercial lending operations.

Current Landscape Of The Credit Union Industry

The credit union industry has always been dynamic, continually adjusting to cater to members’ evolving needs and the broader economic climate. In recent years, credit unions have noticeably increased their engagement in commercial lending activities, a trend that continues into 2023.

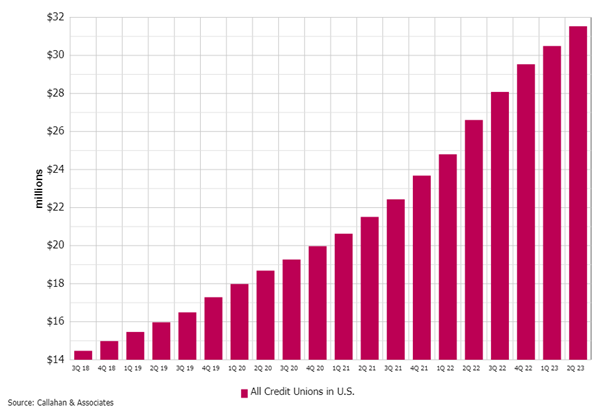

MEMBER COMMERCIAL BALANCES

FOR U.S. CREDIT UNIONS | DATA AS OF 06.30.23

©Callahan & Associates | CreditUnions.com

MEMBER COMMERCIAL LOANS TO TOTAL LOANS

FOR U.S. CREDIT UNIONS | DATA AS OF 06.30.23

©Callahan & Associates | CreditUnions.com

The Digital Shift: Responding To Growth And Competition

The sustained growth in commercial lending necessitates credit unions shift toward technology-driven business models. With the financial services sector facing various industry headwinds, from high interest rates to liquidity challenges, credit unions find it necessary to adapt to the evolving digital lending landscape.

Moreover, rising competition from traditional banks and fintech companies makes it essential for credit unions to leverage technology to streamline operations, enhance member experience, and maintain competitiveness.

Integrated Technology Solutions: Scaling Commercial Lending

In response to these challenges, credit unions are exploring various integrated technology solutions to scale their commercial lending businesses. These solutions include automation tools that streamline loan origination processes and AI-powered analytics platforms that offer insights into members’ financial behavior.

Additionally, many credit unions are turning to digital platforms that enable seamless integration with core systems, imaging, document preparation, data warehouses, and CRM. These integrations not only enhance operational efficiency but also provide a more holistic view of member data, enabling credit unions to make more informed lending decisions.

Leveraging Technology: Key Considerations For A Commercial Loan Origination System

Credit unions that are serious about leveraging technology must adopt a comprehensive and strategic approach when considering a commercial loan origination system. The right system can significantly enhance efficiency, reduce risk, improve member experience, and scale with the credit union’s needs to support the growth of commercial lending operations.

When selecting a system, consider these key factors:

Process Improvement Advisory is Key: A fully integrated loan origination system, paired with process improvement advisory services, facilitates seamless data flow among various platforms, minimizing manual input and reducing the risk of errors, ensuring efficient and effective operations.

Custom vs. Configurability: Empowering system administrators to make changes, rather than relying solely on the software provider, allows for configurability so credit unions can adapt the system to their specific needs, enhancing flexibility and reducing dependency on external support.

Buy Today And Expand Technology Over Time: Scalable loan origination technology allows credit unions to start with the necessary workflows and automation and then gradually expand as their business grows. This approach focuses on long-term success and avoids the need for a complete system overhaul.

Integration Versus Manual: Integration with core systems, imaging solutions, document preparation software, data warehouses, and customer relationship management (CRM) systems eliminates the need for manual data transfer, streamlining workflows and reducing the risk of errors.

Proven Experience Delivering Roadmap Items: A proven track record of delivering roadmap items is critical when selecting a loan origination technology partner. It ensures the software provider has a history of successfully implementing planned features and enhancements, giving credit unions confidence in the system’s future development.

Scoped SOW Up Front, No Third-Party Implementation: When the total cost of ownership is transparent from the beginning — with a scoped statement of work (SOW) outlining all implementation costs — it reduces overall expenses and ensures a streamlined implementation process. This approach also eliminates the need for third-party implementation services that can quickly increase the total cost of ownership without providing value to your credit union.

Measure Capacity, Tune Solution, And Review ROI: Robust data analytics and reporting capabilities allow credit unions to measure capacity, fine-tune the solution, and review return on investment (ROI) on an annual basis. This data-driven approach enables informed decision-making, strategic planning, and continuous improvement year after year.

These considerations provide the foundation for a successful technology migration and should guide decision-making when selecting a commercial loan origination system.

Navigating Change Management Challenges

Despite the clear benefits of technology adoption, credit union executives often encounter several pain points when undergoing the change management needed to excel in commercial lending.

To effectively navigate these challenges, credit unions must adopt a strategic approach to technology adoption. This includes conducting thorough due diligence before selecting a technology partner, ensuring the chosen solution aligns with the credit union’s long-term goals, and investing in staff training to ensure the smooth adoption of the new technology.

As credit unions continue to grow their commercial lending operations, technology adoption will remain a critical factor in success. Although the journey might present challenges, the opportunities for enhanced efficiency, competitiveness, and member satisfaction make the transition well worth the effort.

Baker Hill NextGen® Accelerate: A Purposefully Designed Solution For Scalable Commercial Lending Growth

Baker Hill recognizes the transformative power of technology in empowering teams as well as the challenges many financial institutions face in technology implementation and adoption when scaling their commercial lending operations. To address the unique needs of growing community financial institutions, Baker Hill has designed Baker Hill NextGen® Accelerate, a solution built to help institutions make new technologies more consumable, driving adoption throughout the organization. With a steadfast commitment to industry best practices, Baker Hill NextGen® Accelerate equips institutions with a scalable and adaptable commercial loan origination platform that staff will look forward to using.