A credit union’s ability to deliver the right products and services that meet members’ daily needs is the most important factor in creating a superior member experience.

To retain existing members and engage future generations, it is imperative that credit unions prioritize investments and operations that address these day-to-day needs.

Your credit union should consider expanding credit card underwriting criteria, digital investment, and financial literacy support to strengthen membership growth and loyalty.

Expand Underwriting Processes

Many underwriting approaches rely primarily on member credit scores. Although this is a straightforward approach, it has drawbacks. For example, younger generations just beginning their credit journey may not have the established credit scores of older generations. To reach a broader sector of potential members from evolving demographics and economic conditions, credit unions should consider expanding risk-based underwriting criteria.

Credit scores do not tell the entire story, and, when used alone in the underwriting process, can dramatically limit a credit union’s ability to meet members’ needs. For instance, although the average credit score in 2021 was 714, according to FICO, about 60% of people in the United States have a score lower than 714. Further, within age cohorts, several groups have scores below the national average. Specifically, Gen Z consumers (679) and millennials (686).

Expanding underwriting methodologies can help credit unions identify and provide opportunity for more members who can be responsible users of credit cards. Having the ability to support more members not only improves their experience but also deepens the overall relationship.

Digital Development

To remain competitive, credit unions should offer robust digital services and support for cardmembers. Many credit unions today still ask credit card applicants to enter a brick-and-mortar branch to complete paperwork or perform a manual process that makes it hard for a member or potential member to apply for a card.

As of 2020, The Economist reported that 59% of executives believe traditional, branch-based financial services would be obsolete within just five years. In addition, a growing number of consumers, especially younger demographics, demand frictionless mobile transactions and expect seamless, accessible digital services from their financial institutions. This includes applying for and seamlessly managing a credit card using a mobile device.

According to PYMNTS research, credit unions have been slower to adopt new technology, as just 19% are early adopters or innovators. However, credit unions realize consumers want more digital offerings and are ramping up investments to stay competitive. Seventy-four percent of credit unions made investments in mobile banking in 2021, 64% adopted mobile wallet technology, and half now offer peer-to-peer (P2P) payments capability — nearly double the number from a year earlier. By the end of 2022, only 4% of credit unions will have begun a digital transformation strategy. Offering digital services to credit card holders shows credit unions are committed to evolving with their members’ lives.

Help More Members Understand Their Finances

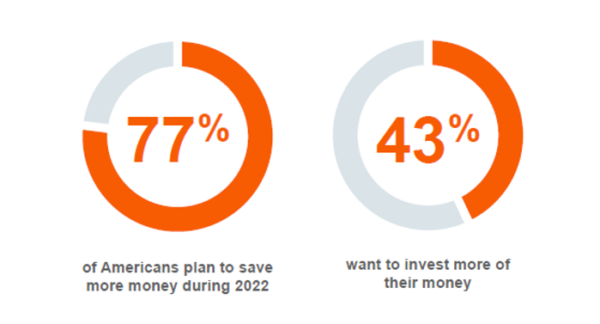

According to Goldman Sachs Consumer Sentiment Study, 44% of respondents want to focus on improving their credit score throughout 2022. Additionally, a CIT Bank survey found:

These survey results show that most consumers are setting financial goals and want to be more financially savvy and literate. Because credit unions excel at this today, this continued financial literacy assistance can reach more members to help them understand their financial health, adopt good financial practices, and save for major purchases.

Younger members often need the most assistance with financial education but are not always the only members who may need financial advice. With respect to financial maturity, baby boomers and Gen X still value the existence of physical branches and have high levels of trust in their financial institutions. Millennials, meanwhile, experience the highest level of interactions with their financial institution each month — almost four times as often as baby boomers and 50% more than Gens X and Z. All factors to keep in mind when addressing member preferences.

Supporting financial literacy can positively influence the member experience, deepening member engagement and encouraging members to use more of a credit union’s financial services — including credit cards.

Support Your Members

As preferences shift, it’s vital credit unions remain agile and adaptable. Having the resources to respond quickly to new products and services will help member engagement.

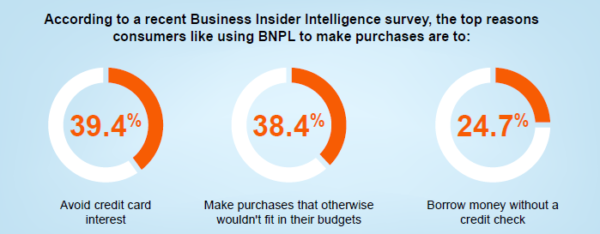

One recent change in consumer behavior is the growth in buy now, pay later (BNPL) and similar services. According to Accenture, spending on BNPL grew by 230% during 2021.

Notably, 14.4% said they use BNPL because they can’t get approved for a credit card — potential further reasoning for credit unions to explore expanded underwriting.

Fortunately, credit unions don’t have to lose focus on the goal of growing and engaging members in pursuit of the latest digital capabilities. Credit unions can take advantage of industry experts that provide AI and machine learning tools without needing to invent and managed in-house versions of these technologies. Leverage the strength of a financial services provider with a deep commitment to service, existing partnerships with more than a thousand financial institutions, and proven technology developed over the past six decades: Elan.

Elan is your partner in the complex and rapidly changing credit card landscape. With Elan, you will have access to competitive products, industry-leading reward options, and a dedicated underwriting team. Our underwriting process allows credit unions to use incremental relationship data to reach more members while using the credit union’s own branding. Benefit from the proven top-of-wallet appeal Elan offers, without the costs and risks.

Download our latest whitepaper for more insights and strategies to engage your members and contact us to learn how your credit union can stay competitive with a credit card partnership.