This is part of the Callahan Financial Performance Series. Presented by the analysts at Callahan & Associates, the series helps leaders interpret data to drive smarter decisions and uncover new approaches to measure performance. Callahan clients can access the full version of this article right now on the client portal. Read it today.

For millions of American households, paychecks no longer stretch to cover the basics. As the cost of housing, food, and other essentials races ahead of wages, the financial squeeze is hitting hardest where credit unions are most focused: lower- and middle-income families trying to hold their ground.

Nowhere is the affordability squeeze more acute, and more destabilizing, than in the cost of housing.

Households in the United States are considered “cost-burdened” if they spend more than 30% of their income on housing and utilities. The Federal Reserve Bank of Atlanta estimates buyers today need to earn at least $121,000 a year to afford a typical home without becoming cost‑burdened. In reality, the U.S. median annual income is approximately $84,000, with households earning just over $105,000.

Many factors have contributed to today’s elevated housing prices, chief among them is a lack of inventory. Asset appreciation, higher mortgage rates, and tighter credit are prompting many homeowners to sit tight in their current homes, restricting supply and pushing prices higher. As a result, household equity now accounts for 73% of all real estate value in the United States, nearly an all-time high. In all, the country has an estimated deficit of 2.4 million homes, according to analysis by Apollo and Haver Analytics. As prices rise, existing home sales have dropped to a 30-year low.

For would-be buyers, the challenges continue even when they turn to new construction. The cost to build a new home has jumped in lockstep with material expense, rising insurance premiums, property taxes, and more. Apollo Global Management reports the number of new-construct, privately owned homes that have been authorized but not started has risen by more than 40% since the COVID-19 pandemic.

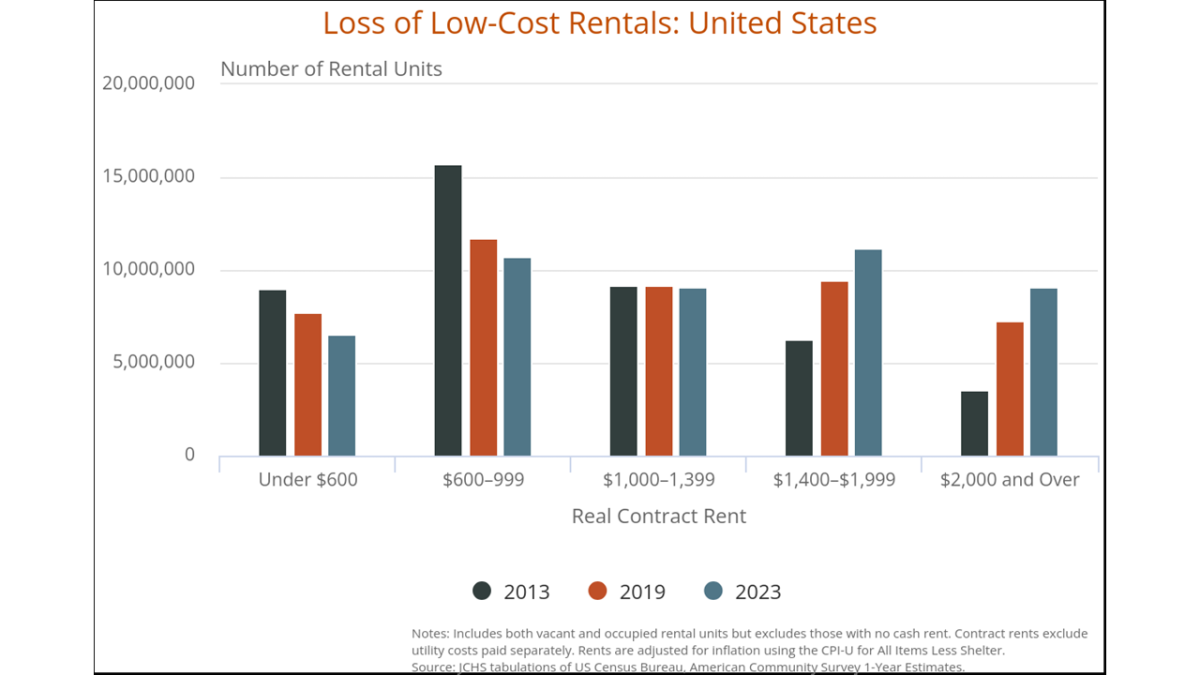

LOW-COST RENTAL AVAILABILITY

FOR THE U.S. HOUSING MARKET

SOURCE: HARVARD UNIVERSITY JOINT CENTER FOR HOUSING STUDIES

The cost of housing has ballooned into a systemic burden that is pinching even those households that aren’t trying to purchase a home. According to Harvard University’s Joint Center for Housing Studies, 50% of the country’s renters are cost-burdened; 27% of renters are severely cost-burdened, spending more than half of their income on housing.

Although rental construction is up — the country added 608,000 new multifamily units in 2024 — much of this development serves the upper end of the market, providing little to no relief for households who need lower‑cost units.

Ready To Read The Full Story? Dive into the rising costs of education, transportation, and everyday necessities to learn what it means for your members. Callahan clients can access the full version of this article right now on the client portal. Read it today. Not yet a client but looking for expert insights to help you adapt to change, develop your organization’s leaders, and stay at the forefront of industry trends? Connect with our team to learn more.