Top-Level Takeaways

-

First Tech put in nearly three years of research before launching three student loan refinancing options, which now comprise nearly half of its outstanding student notes.

-

A team of advisors at First Tech works with student borrowers to help them choose the right refinancing.

First Tech Federal Credit Union ($12.1B, Mountain View, CA) is $45 million into addressing the nation’s trillion-dollar student debt issue the Silicon Valley credit union says is hitting hard among its membership and SEGs.

CU QUICK FACTS

First Tech FCU

Data as of 06.30.18

HQ: Mountain View, CA

ASSETS: $12.1B

MEMBERS: 529,290

BRANCHES:41

12-MO SHARE GROWTH: 10.4%

12-MO LOAN GROWTH: 18.1%

ROA: 0.98%

The cooperative is three years into a deliberative process of discovery and creation that took it out of lending to students for school and put it into refinancing their existing debt.

First Tech offers three different loan products that are tailored to members at different life stages and repayment capabilities. The loans have been available for approximately 18 months the credit union soft launched them in April 2017 and already account for approximately 700 of the 1,600 student loans currently on First Tech’s books.

Although they account for only $45 million, roughly, of the nearly $9 billion loan portfolio at the nation’s sixth-largest credit union by assets, the refinanced loans speak to the program’s larger point.

ContentMiddleAd

Our goal is to help our members live the lives they want, have the careers they want, and make the choices they need to make based on what they want and not on what they have to do because of student debt, says Sandi Papenfuhs, First Tech’s senior vice president of consumer lending.

First Tech doesn’t originate student loans anymore. Instead, it refinances student loans, primarily federal student loans.

Best Practices For The Long Run

Student loans are a discipline unto themselves and as such, require a different approach. Here, Sandi Papenfuhs, SVP of consumer Lending at First Tech FCU, shares best practices for researching and launching a line of refinancing products.

Understand the member. Needs and desires of student borrowers is not the same between credit unions or members. Devote the time and energy to find out what drives borrowers within your organization.

Understand the product. There are significant differences in loan delivery, compliance, and legal requirements that credit unions must understand before entering the student lending market. There are providers of student loan products, both in-school and refinancing, who can help, Papenfuhs says.

Understand the risk. According to Papenfuhs, the market for student loan refinancing is much smaller than for in-school loans and rating risk can be more challenging. There’s not a lot of good data out there, the SVP says. We spent a lot of time developing and understanding credit risk models for these loans.

Staffing and training. First Tech is in this line of business for the long run. As such, it has built a team of eight advisors and a manager from the ground up. It also created a manual and certification program.

We put a pause on in-school loans in 2013, Papenfuhs says. Many are still on our books, but we understand our membership and their needs better. We did that by listening to them.

The formal effort to understand members’ needs began two years after the credit union suspended in-school lending. Through emails, anecdotal information, member analysis, and SEGs conversations, First Tech found that borrowers fall roughly into two categories: students themselves and parents who borrowed for their children.

It also found that, because of student debt, the former were often delaying life events such as buying homes and forming families and the latter were often delaying retirement.

We spent almost a year researching the regulations, the rules, the providers, and the pain points consumers feel around student loans and debt, Papenfuhs says. We did a tremendous amount of research not only because we wanted to understand the issue but also because we wanted to see if we could execute products on our own and do it well. The answer was yes.

That was in 2015. The credit union then spent another year determining the specific needs of its SEGs those high-tech companies dependent on productive, engaged employees and the members themselves. That’s how it ended up with the three refinance products it has, Papenfuhs says.

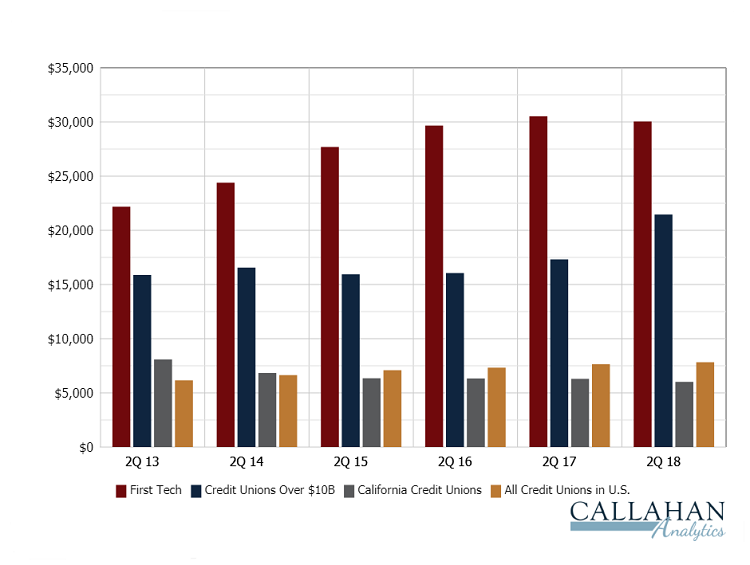

AVERAGE STUDENT LOAN BALANCE

FOR U.S. CREDIT UNIONS | DATA AS OF 06.30.18

First Tech’s average student loan balance is $30,040, compared with $21,456 for credit unions with $10 billion or more in assets. The average for all 714 U.S. credit unions that participated in student lending as of the second quarter of 2018 was $7,827. The average for California credit unions was $6,014.

Source: Callahan & Associates.

The data in this article is from Callahan’s Peer-to-Peer. Want to analyze your performance against relevant peers in the industry? Learn more about Peer-to-Peer today.

Fixed-term loan: The fixed-term loan allows borrowers to pay off student loan debt in equal monthly payments of principal and interest. Papenfuhs says this option accounts for approximately 90% of the refinancing activity so far and is aimed at getting the borrower out of debt as quickly and inexpensively as possible.

Balloon loan: The balloon loan allows borrowers to pay smaller monthly payments now and one large payment at the end of the loan term. First Tech designed this option to appeal to borrowers with unusual income types, Papenfuhs says, such as a lower base wage supplemented by bonuses, stock options, and futures. We see that a lot in the tech space here, she says.

Interest-only loan: The interest-only loan offers borrowers a lower monthly payment for the first few years of the loan with payments increasing as principal and interest are added. With this option, First Tech aims to serve members who currently have a lower income but expect it to increase.

Each of these loans solves different needs, but the point is the same: We want to enable our members to live the life they want, Papenfuhs says. We’re pretty certain that doesn’t include paying 40 years on a student loan.

Sound Advice

Approximately 90% of First Tech’s student refinance options are fully amortized, fixed-term loans. It determines which option is best for the individual borrower through a personalized, digitized advisory process. Members can reach out through any channel and engage with a student loan specialist specifically trained for the job.

There are a lot of options available, particularly when the debt is with the federal government, that can include deferment and even in some limited cases, forgiveness, Papenfuhs says. We want to make sure they understand all their choices. Then, we can help them decide what’s best for them.

Sandi Papenfuhs, SVP Consumer Lending, First Tech FCU

The size of the debt can be considerable, from a few thousand dollars to a couple hundred thousand for professional and graduate degrees, and the borrowers often have multiple loans to manage, not just a single debt.

Helping pull those obligations into a single, goal-appropriate loan can be not only a relief but a game-changer for borrowers making life decisions based on their student loans.

Employers benefit, too, when they can hire employees who have a passion for the job and not just the paycheck.

As we talked to members about their needs and desires and financial obstacles, student loans came in loud and clear, Papenfuhs says. This also challenges our sponsor companies because borrowers are people who might not be where they want to be but are there because they have to be.

The lending SVP adds, The student debt burden is a national issue, and we felt like we needed to do something. Now, we are.