Two credit unions on opposite sides of the country have cracked the code on what it takes to engage young members from their school years into adulthood.

Those developments come as the industry’s average member age remains in the mid-40s, and credit unions of all sizes search for ways to attract young members and hold them over the long haul.

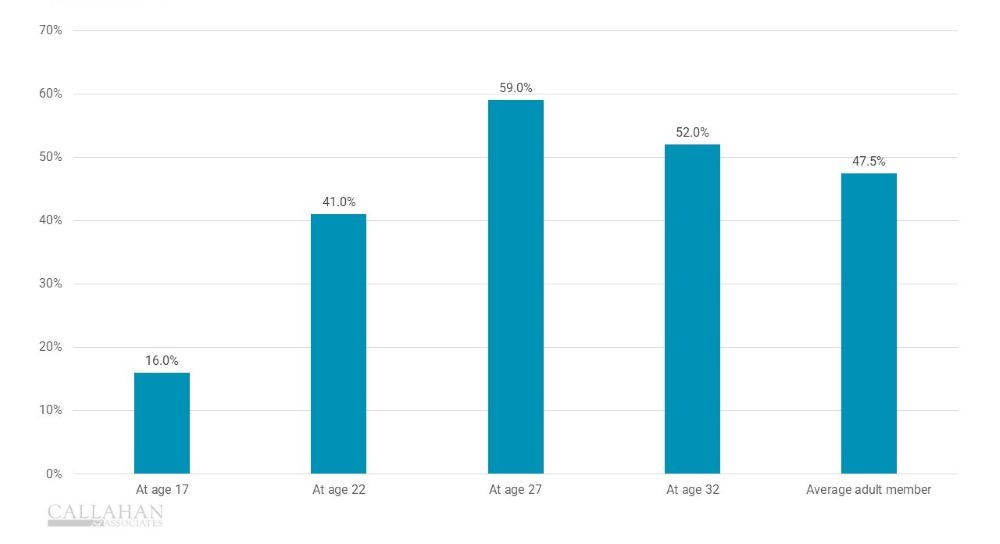

From First Account To Adulthood

In 2025, SchoolsFirst Federal Credit Union ($36.7B, Tustin, CA) had more than 139,000 members who were age 17 or younger. That’s a triple-digit increase of 142% since 2010. Even better, the credit union has tracked that cohort’s engagement upon reaching adulthood and has noted a steady uptick in participation and engagement that rivals its average adult member.

SCHOOLSFIRST FCU MEMBERS WITH 4 TO 7 PRODUCTS

FOR SCHOOLSFIRST FCU | DATA AS OF 2025

SOURCE: SCHOOLSFIRST FCU

Young members of SchoolsFirst FCU have two youth account options, depending on their age. Those up to 12 years old may join the credit union’s Junior Varsity Club, whereas 13- to 17-year-olds may join the Varsity Club.

Parents generally open youth accounts when children are approximately 6 years old, although enrollment is balanced across all age groups. Regardless of age, the credit union offers age-appropriate products and services for each cohort, such as the College Saver Share Certificates and a Youth Debit Mastercard with spending and withdrawal limits. A whopping 69% of Varsity memberships carry the youth debit card, with 53% of those members actively using it.

CU QUICK FACTS

SCHOOLSFIRST FCU

HQ: Tustin, CA

ASSETS: $36.7B

MEMBERS: 1,568,368

BRANCHES: 73

EMPLOYEES: 2,985

NET WORTH: 9.44%

ROA: 0.80%

A full 87% of youth memberships are opened in the branch, but the credit union notes a growing number of youth membership application coming in across digital channels, including online and mobile. To bolster that growth and highlight its youth offerings, the cooperative is producing web content, print materials, educational workshops, and more.

Once the credit union signs up a young member, it offers financial workshops as well as online and mobile services to serve them as they grow into adulthood. It also leans on modern communication platforms, including social media video, to connect with young members on channels they prefer.

SchoolsFirst FCU builds its youth-to-adult engagement model around four key areas:

- Early Financial Education And Workshops — This includes money management, in-school events, digital and print resources, and more.

- Youth Products — From youth debit cards to savings accounts and beyond, SchoolsFirst FCU supports all its youth products with education, resources, and guardrails like ATM usage limits to encourage responsible use.

- Parental Engagement — Those overseeing the accounts have guidance on different product tools and features, best practices to support youth financial development, and more.

- Automatic Transition To Adult Membership — This step at age 18 ensures continuity and minimizes friction to preserve member relationships. It also provides immediate access to checking and debit products, savings tools, credit-building opportunities, and more, with no new onboarding required.

No Substitute For School

Jeanne D’Arc Credit Union ($2.2B, Lowell, MA) has operated in-school branches since 1997 and currently runs three, the newest of which has been in place for a decade. The credit union tracks member engagement for those who start their accounts as students and reports 80% are still active 15 years later.

What does that engagement look like? The cohort holds more than a single savings account, and credit union leaders are digging into whether those members have taken out loans and how their participation has changed over time.

“We build their trust and get them at the start of their banking relationship,” says Robin Lorenzen, chief marketing officer. “They trust us because we were there when they were growing up.”

Jeanne D’Arc recruits high school branch managers to engage with the students, teaching the basics of banking and writing scholarship recommendation letters. It also offers student interns class credit for working the in-school branch. Those interns also help spread the word about the credit union.

Even with modern digital banking and financial education tools, Lorenzen says there’s no replacement for the in-school branch experience and classroom-based financial education.

“They’re engaged on multiple levels because we’ve come to them instead of trying to get them to come to us,” she says. “We’re meeting them where they are, and those high school branches create a unique relationship with the students.”

“This generation wants to do it themselves, but they want somebody there when they need help,” she says.

CU QUICK FACTS

JEANNE D’ARC CREDIT UNION

HQ: Lowell, MA

ASSETS: $2.2B

MEMBERS: 101,075

BRANCHES: 8

EMPLOYEES: 155

NET WORTH: 8.9%

ROA: 0.35%

But branches alone aren’t enough, Lorenzen adds. The credit union also has a six-person financial education team that supplements the in-school branches and teaches in the classroom. Those multiple touch points reinforce themselves over time, building a relationship with the students that leads to trust and long-term engagement.

The credit union provides in-person support and builds relationships through high school branches. As those members age out, they know they can still turn to a branch when they need help, but they also know how to navigate online banking and self-service resources.

The growth of self-service channels in the past 15 years has been instrumental in forging long-term engagement, Lorenzen says, because graduating students know they don’t need to find another bank or credit union after high school.

“They know they can still bank with us,” the CMO says. “That trust is there, so they take us with them.”

Lessons Learned

To replicate the success of SchoolsFirst FCU and Jeann D’Arc, both credit unions say it’s important to understand this a long-term commitment to member development, not short-term product growth.

SchoolsFirst FCU also says its crucial to empower front-line staff to act as advocates for members. Thoughtful questions paired with the right solutions, not a focus on pushing products, builds trust early and establishes the foundation for a durable relationship.

For Jeanne D’Arc, maintaining touchpoints with students is key. This includes the in-school branch as well as the classroom, student activities, Reality Fairs, and more.

Equally important? Try to keep it light.

“In high school it’s not all about selling and teaching,” Lorenzen says. “There are ways to bring in the kids to interact, whether it’s trivia or giveaways or something like that. It’s not always about banking; it’s about connection.”