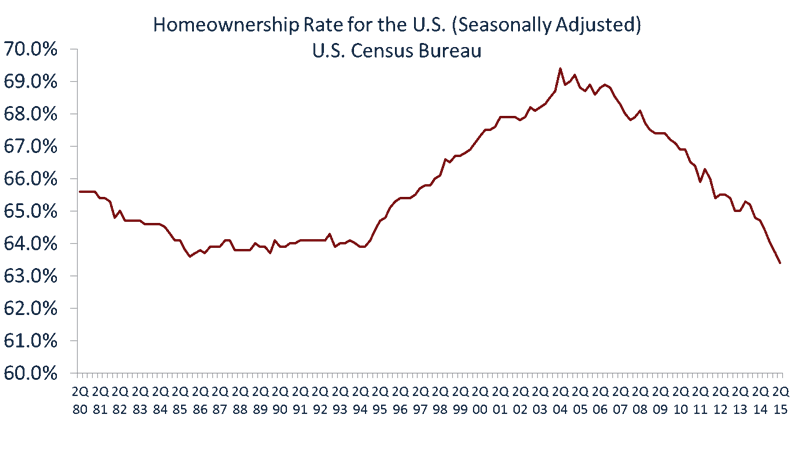

Homeownership in the United States peaked near 70% in 2004. However, it has steadily declined since then, and it is up for debate whether the rate of homeownership will eventually flatten out or continue to decline.

As of third quarter 2015, the homeownership was 63.7%; that’s down from 64.4% in the same period one year ago. Historically, the homeownership rate has hovered around 67%.

Those claiming it will flatten out are looking to millennials who are finally moving out of their parents’ homes and renting their own places to begin starting families and buying homes in the next several years.

Those positing the homeownership rate will continue to decline say millennials are moving into urban centers and baby boomers are downsizing, making the decline in homeownership the new normal.

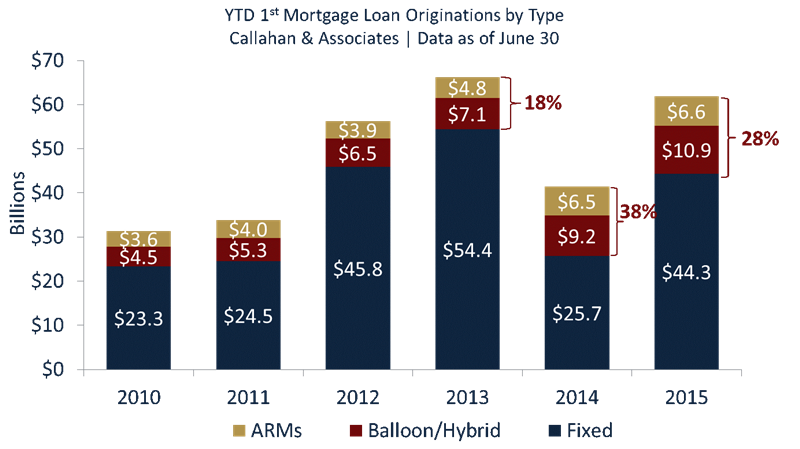

Mortgage originations in the United States have ebbed and flowed over the past several years. A wave of refinancing activity underpinned the surge in originations in 2012 and 2013, but as the supply of homeowners eligible for refinancing began to dry up, originations leveled out in 2014.

This year, however, has marked the return of the purchase mortgage market. Total mortgage originations increased 33% in the first six months of 2015 compared to the same period in 2014.

As a percentage of total first mortgage originations in the first and second quarter of the year, credit unions originated far more fixed rate products in 2015 compared to the same period in 2014.

Why this increase? First, members are locking in low rates while they are still available. Second, to manage their interest rate risk and still serve members, credit unions are originating more fixed rate loans they can sell to the secondary market.

In aggregate, fixed rate first mortgages as a percentage of the total first mortgage portfolio actually declined slightly year-over-year 59.3% in 2015 versus 60.6% in 2014 in part because of the 81% increase in sales of first mortgages to the secondary market.

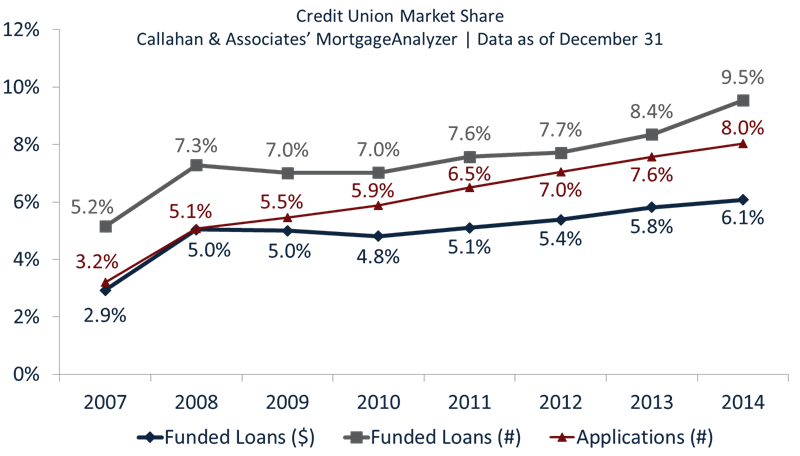

In the newly released 2014 Home Mortgage Disclosure Act (HMDA) data, 7,062 institutions reported originating a mortgage in the 2014 calendar year, totaling roughly 6 million mortgages valued at approximately $1.4 trillion. Although all major metrics declined year-over-year, credit unions fared better than their bank and mortgage company counterparts. The total number of loans originated declined 31.3% but credit unions reported a decrease of only 21.5%. The dollar amount of loans originated fell 27.2% but credit union origination amounts declined only 23.7%. As such, credit unions continued to steadily increase their market share in the three categories noted below.

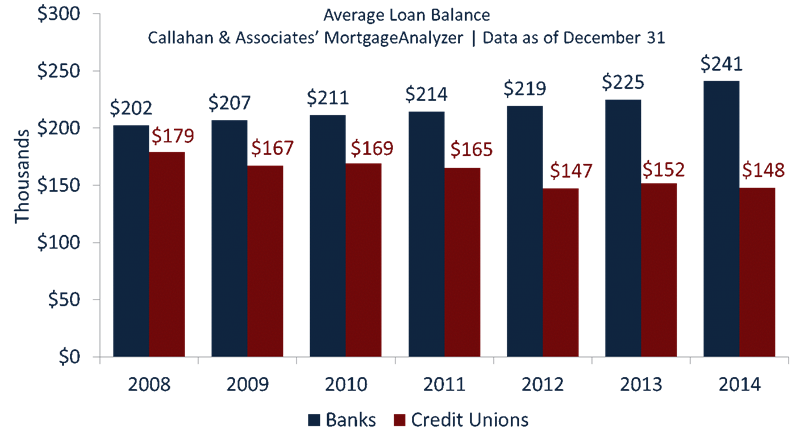

From a market share perspective, credit unions hold a smaller proportion of the pie in terms of dollar amount of loans funded relative to their market share of number of loans funded. When taken in context of credit unions goals and membership demographics, however, this is a positive sign. It demonstrates that credit unions are originating loans with lower average loan balances and helping lower-income families move into homes across the country.

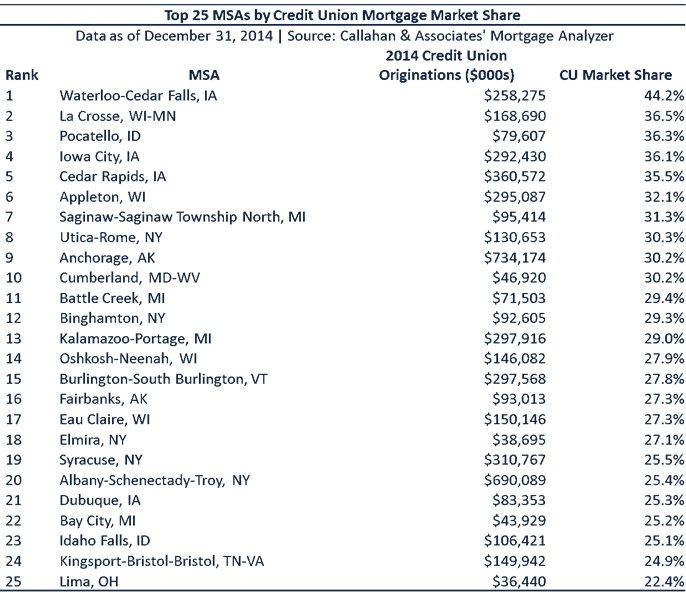

All lenders strive to increase their visibility within the community, and credit unions often face uphill battles in areas where large banks have a foothold in the market. However, as highlighted in the table below, credit unions in specific markets have been able to achieve tremendous success using the right combination of loan products, marketing, and execution.

Want to learn more about the United States mortgage market?Watch the Callahan webinar Trends In Mortgage Lending today.

Watch Now

Struggling with market visibility? Learn how Ent FCU stays top-of-mind with its members and community in this CreditUnions.com article.

Read Now