Much opportunity still exists for credit unions to take advantage of the mobile channel for onboarding members and account and loan applications, but the window won’t stay open forever.

Bob Meara, longtime Celent payments and service delivery channels analyst, says that many retail industries make 15% to 20% of their sales on smartphones, tablets, or computers these days, but that credit unions and banks still lag far behind.

Meara told a recent webinar that based on Celent research twice as many people visit a bank’s website as a branch when shopping for a new account and more than half of all transactions are now completed in virtual banking channels.

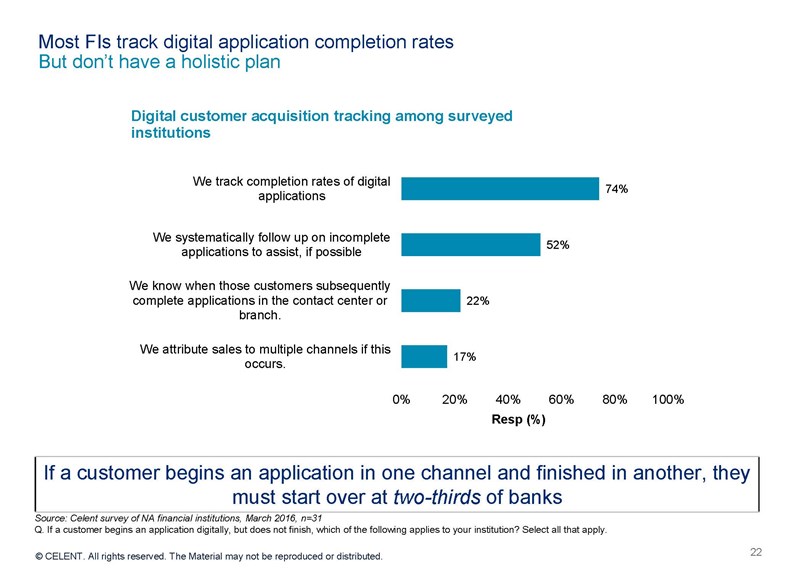

This Celent slide shows how financial institutions the think firm studied handled digital customer interaction.

The disconnect? Fully 85% of new account openings were in the branch. Only 2% were mobile and 6% were opened online. The other 7% were through a contact center. Even fewer non-mortgage loan applications were done on a mobile device: a mere 1%. Eleven percent were done online.

The fact that banks and credit unions are lagging behind retailers means there is a huge opportunity, Meara says. There is verifiable evidence that you can move the needle in a dramatic way by investing in a good customer experience, training front line staff, and integrating digital account technology across marketing channels.

He cited strong 2Q 2016 results by Bank of America as an example, and left the Bluepoint Solutions webinar attendees with this takeaway: There’s still time for credit unions to catch up with digital account opening but that time might be short, since consumer expectations might finally be driving channel integration.

The growth trajectory for all things digital is very clear, Meara says. Look, for many years, annual surveys of consumers told us that branch proximity and convenience were the top factors in decisions about where to do their banking. But mobile and digital capabilities have been gaining steadily and will soon overtake most other answers.

The Celent analyst said now’s the time, and that it won’t get easier for those who wait and then must come from behind.

Along with the need to understand the omni-channel customer journey including knowing how many prospective accountholders are turning away Meara made these points:

- Most FIs track completion rates for digital account opening and say they are well below goals, even two decades into online banking.

- Just 40% of surveyed banks and credit unions have specific, measurable goals for increasing digital onboarding.

- Most FIs are flying blind as to why consumers abandon the process, and there’s rarely any follow up. Meara said he thought that was crazy, given that these are qualified, clearly self-motivated sales leads who came to buy your product.

- A big problem is that there is very little to no integration between the channels branch, mobile, web, phone. They don’t talk to each other. Meara said he was referring to people and processes.

- Omnichannel integration does exist and should be used to allow the end user to halt an application and then pick it up, at the exact same spot, in a different channel.

- AML/KYC compliance is no longer the sticking point that has made channel integration and completing the process on remote channels so difficult.

- Avoid cross selling during the process until after the accounts are opened. That can always come later.

- The new Uber app is stinking fabulous and that company has again raised the bar on the customer experience. Meara cites it as a strong example of the experience being customer-driven rather than employee-driven.

Meara cited one credit union in his talk USAlliance Federal Credit Union ($1.2B, Rye, NY) as a financial institution that gets it. He said says it’s used digital tools to lower its account opening abandonment rate from 85% to 35%.

Bottom line: The number of consumers relying on mobile and online banking for account opening is still in the minority. But it won’t stay that way for long. And unless you follow dropped account apps and fix the reason they happen, you won’t know even a small piece of the opportunity cost, much less stop it from happening.

Now’s the time to get your ducks in a row while the stakes are still relatively low, Meara says.

You Might Also Enjoy

-

Don’t Just Onboard, E-Board

-

Mobile Onboarding That Works In And Out Of The Branch