Top-Level Takeaways

-

UWCU and First Tech are early adopters of Zelle, a digital payments network launched banks, credit unions, and technology suppliers launched in response to Venmo and PayPal.

-

Adoption has been promising, with thousands of members moving millions of dollars.

CU QUICK FACTS

University Of Wisconsin Credit Union

Data as of 12.31.18

HQ: Madison, WI

ASSETS: $2.8B

MEMBERS: 259,054

BRANCHES:27

12-MO SHARE GROWTH: 10.5%

12-MO LOAN GROWTH: 19.9%

ROA: 1.30%

Only five minutes had passed when the first member of the University of Wisconsin Credit Union ($2.8B, Madison, WI) used the cooperative’s new Zelle person-to-person payments offering.

That was on Jan. 24 this year, and by the end of March, more than 13,000 members had used Zelle through the UWCU app or website, moving nearly $4 million through approximately 15,000 transactions, says Eric Bangerter, UWCU’s vice president of e-commerce.

Those 13,000 or so members represent 6.5% of the credit union’s online banking base, but that’s a pretty good adoption number considering the real marketing doesn’t begin until this summer, Bangerter says.

CU QUICK FACTS

First Tech FCU

Data as of 12.31.18

HQ: San Jose, CA

ASSETS: $12.2B

MEMBERS: 554,529

BRANCHES:43

12-MO SHARE GROWTH: 7.2%

12-MO LOAN GROWTH: 5.4%

ROA: 1.05%

Right now, Zelle exists as an unadvertised menu option on the credit union’s website and app. An indication of how receptive the audience is: Bangerter says about 3,000 members signed up as new users recently after UW simply added a popup screen about it on its website.

A partnership of banks, credit unions, and technology suppliers, along with Early Warning Services as the operator, launched the Zelle Network in September 2017 to compete against the likes of Venmo and PayPal. As of March 18, Zelle listed 14 credit unions among the approximately 110 financial institutions now live on the P2P service through mobile app and online banking.

First Tech Federal Credit Union ($12.2B, San Jose, CA) is among those front-runners.

Zelle is a fast, safe, and easy way to send money to friends and family, says Frank Choy, vice president of digital products. We jumped at the opportunity to partner with Zelle to simplify P2P transactions so our members can move money 24/7 in the First Tech app.

Frank Choy, Vice President of Digital Products, First Tech FCU

First Tech was a particularly early adopter, going live in September 2017, and had 28,117 members signed on at the end of 2018. The new payments channel handled 206,133 transactions last year, moving $81 million from person to person.

Zelle helped us get the word out to employees and members with a coordinated campaign that worked well with our brand, Choy says. Email, social media, website, and video tools have been used so far.

We’ll continue to run awareness campaigns throughout the year, and we expect adoption to grow, Choy says.

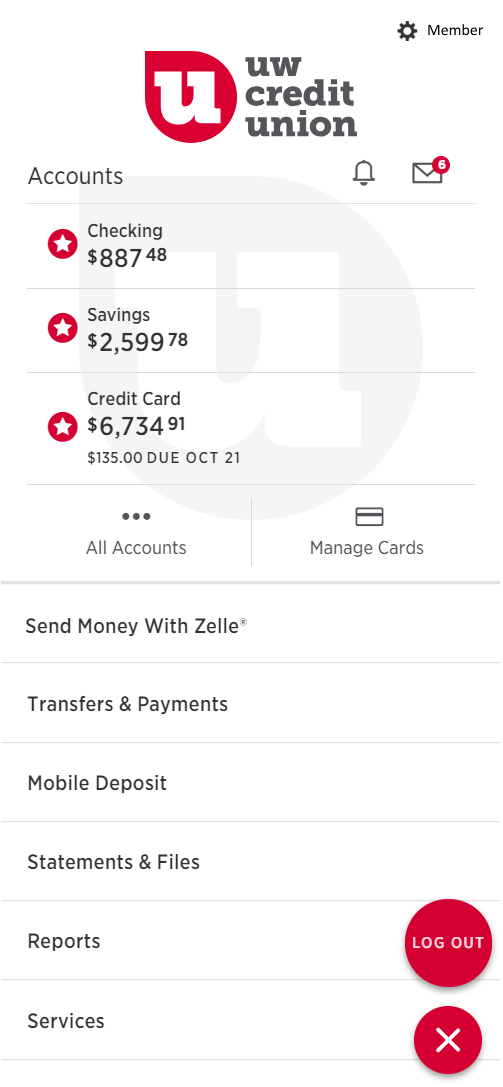

Click the tabs below to see what Zelle looks like for members who use the UWCU mobile app.

UWCU ZELLE HOME

The Zelle screen is simple and direct and includes splitting the bill functionality.

UWCU ZELLE MENU

A link to Zelle resides on the home menu on the UWCU mobile app.

Halfway across the country, UWCU is still planning its advertising push. Bangerter says Zelle will be part of the digital offering marketing the credit union does each summer, which last year included bus wraps, billboards, and direct emails.

Eric Bangerter, Vice President of E-Commerce, UWCU

EWS says the Zelle Network processed $119 billion in payments on 433 million transactions last year, with year-over-year transaction volume up 81% from the fourth quarter of 2017 to the fourth quarter of 2018.

Zelle transactions are basically real-time if they occur between network member institutions, but consumers can also use the service by registering their debit card in the Zelle mobile app. EWS says more than 100 banks and credit unions signed on in the fourth quarter of 2018 and are in line to get connected. Customers of more than 5,100 financial institutions overall already are using the Zelle Network.

For consumers, using Zelle takes nothing more than an email address and a linked debit account, but it involves an intricate dance behind the scenes. That’s why technology providers are critical to the process, too.

Find your next partner in Callahan’s online Buyer’s Guide. Browse hundreds of supplier profiles by name, keyword, or service area.

2 Ways To Win With Zelle

Frank Choy has been vice president of digital products at First Tech Federal Credit Union for the past five years. During his tenure, he planned and executed First Tech’s Zelle strategy. Here’s his advice for launching the P2P payments network.

- Align for a smooth kickoff. Implementation is a major money movement functionality, so First Tech involved stakeholders across all teams and consulted all business functions during the architecture and requirement-gathering.

- Be clear about customization. Zelle has strict design, user experience, style, and marketing guidelines. First Tech was transparent about the adjustments needed to fit its clientele and digital platforms.

JHA, owner of the Symitar core processing platform, has just launched the JHA PayCenter, a proprietary payments hub that provides a single integration point to faster payments networks including Zelle and the RTP network from The Clearing House.

The hub can onboard approximately 25 financial institutions per month, JHA says, and provides real-time messaging, posting to the core, data contribution, and settlement and reconciliation processes. The first client is scheduled to go live in May, the company says.

CO-OP, meanwhile, is in Zelle beta with several credit unions with plans to go live this year and expand the roster, says Angel Siorek, vice president of debit channels.

And Fiserv is offering its Turnkey Service for Zelle, which Tom Allanson, president for electronic payments, says offers financial institutions a simplified path to implementing ubiquitous, frictionless, person-to-person payments.

UWCU is using Fiserv to move data and money between its FIS Miser core processing system and the Zelle Network. The service hosts and integrates the various interfaces needed to make the system work and provides the risk management tools needed to vet and challenge users.

Fiserv currently has six credit unions live on Zelle with more added every month, says Mike McCoy, Fiserv’s vice president for the Zelle Enterprise Program. He says clients live on Zelle are reporting transaction increases anywhere from 100% to 300% as compared to prior P2P solutions within a few months of going live.

The real-time capability required to offer Zelle can be leveraged by the institution to enable additional types of payments in real time, McCoy says. This brings a substantial amount of value to the credit union as compared to a one-off project.

Value like bill pay and account-to-account transfers.

You Might Also Enjoy

-

All Aboard Zelle: A New Train Takes Off On An Old Rail

Data integrity is critical to successful Zelle use, Bangerter at UWCU says. The wrong phone number or email can bring a transaction to a screeching halt, and Class A identification information such as Social Security and driver’s license numbers also need to be clean and correct.

UWCU had been working to confirm such data in its core system every six months and added extra programming before and after the Zelle launch just to make sure.

Along with vendor help, Bangerter says UWCU is drawing on its own unusually long record of hands-on experience with P2P. UWCU began offering its own service called Money Link back in 2005, working with payments specialist CashEdge (which Fiserv acquired in 2011).

That’s an ACH-based system and UWCU knew it had to find a faster way to move money to keep up with the times and to expand its reach.

We’re a Wisconsin credit union with no national brand, Bangerter says. By joining Zelle, we’re part of a well-known, established network, instead of going it alone.

Bangerter says he had an aha moment when he saw the Zelle commercial during Super Bowl 2018 and realized it was really becoming recognizable. However, recognition also creates expectation.

When a member sees a commercial for Zelle, they’re likely to start looking to their credit union to offer it, says CO-OP’s Siorek.