Interstate 65 nearly bisects the state of Alabama, running straight from Decatur to Birmingham before curving down east into Montgomery and then taking a hard southwest route into Mobile.

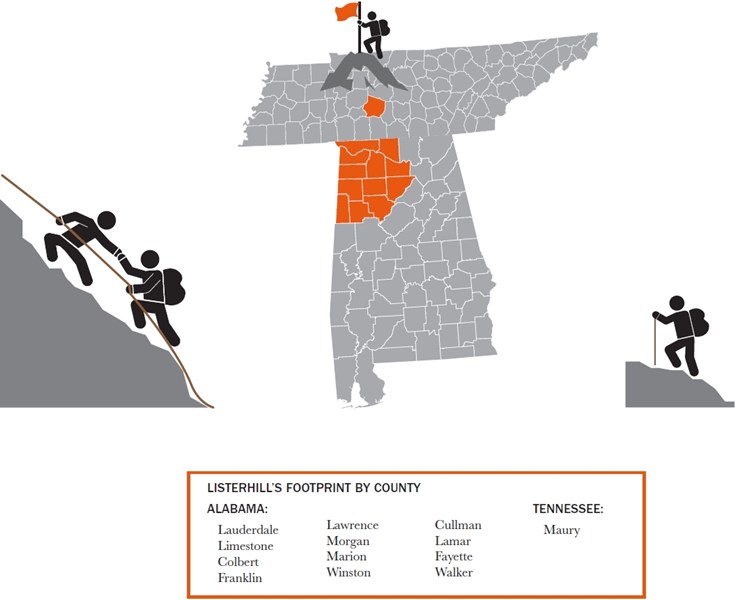

The road also serves as the de facto marker that separates Listerhill Credit Union’s ($674.5M, Sheffield, AL) primarily northwestern field of membership from the rest of the state. It’s a line preserved not only by highway but also by a culture that prioritizes cooperation over competition.

We shy away from anything east of the interstate because there are already credit unions that serve that market well, says Brad Green, Listerhill’s CEO. Why would we want to go over there and try to take market share? That doesn’t make sense to me.

But that doesn’t mean the credit union is opposed to expanding its geographic footprint. In fact, the credit union has a single branch outpost in nearby Tennessee but sees near unlimited opportunity on the horizon.

A Willing Volunteer

In the first quarter of 2012, Listerhill was adding loans faster than many Alabama credit unions, but it was lagging in share and member growth. Leadership at the credit union wanted to improve this performance while also setting up the organization for future growth.

So when First Community Credit Union headquartered in Columbia, TN, and with less than $25 million in assets asked Listerhill to merge in the summer of 2012, it was an opportunity the Alabama-based cooperative was ready to pursue.

They were coming off some troubled times and we told them we’d be glad to give them whatever assistance they wanted to help them back on their feet, says Listerhill CFO Clay Morgan. But they said, no, they wanted to merge.

At the time, Kristen Mashburn, vice president of marketing, had completed research that showed Listerhill’s Alabama market possibly was saturated and growth prospects were limited unless the credit union expanded its geographic boundaries. And due diligence of the area showed that Maury County was home to just two credit unions and nine banks exactly what Green had in mind.

We were looking for places where the concentrations of credit unions weren’t so high, he says. For us, that’s rural areas and smaller towns or communities that don’t have the access of larger areas.

The completed merger on Nov. 1, 2012, yielded the first Listerhill branch beyond the Alabama border.

The Tennessee Market

Maury County in Tennessee is not contiguous with any of Listerhill’s 13 Alabama counties. However, it’s only slightly more than 80 miles north of the credit union’s headquarters.

U.S. Census estimates from 2014 puts the population of Maury County at approximately 85,000. Along with the other counties it’s targeting, this expansion would almost double the credit union’s potential market size, Morgan says.

Maury County’s homeownership rate of 70.3% is greater than the Tennessee average, as is its median household income of $45,300. The percentage of residents below the poverty level, 15.4%, is also below the state average. In short, it’s a market Listerhill is looking forward to tapping.

On the mortgage side, their market is going crazy right now, says Jerry Scarborough, vice president of mortgage lending. Without counting its main office, the Columbia branch ranked third in 2015 for both number and dollar amount of mortgage loans made.

Fred Lindsey, Listerhill’s vice president of business service operations and manager of the institution’s $85 million member business loan portfolio, views the area as a tremendous growth opportunity. Listerhill’s MBL portfolio is mainly composed of commercial real estate, the same loan types Lindsey hopes to make in Tennessee.

We do smaller commercial loans, he says. We don’t chase other types of loans we aren’t comfortable with.

At its sole Maury County branch, the credit union is looking for an outside loan officer to work specifically in real estate and develop relationships with local realtors and builders.

Growing deposit market share, however, has been more challenging. Today, Listerhill’s Maury County branch ranks ninth out of 12 in overall deposit market share after increasing this portfolio by just 4.8% year-over-year.

And overall, Listerhill has budgeted for lower annual deposit growth across the institution than it has in years past, to 6-7% from 8-10%, Morgan says.

We’ll go to local community events in Tennessee, jump on the microphone and say, We’re a credit union. If you’re helping the community you’re doing something we want to support, so come talk to us.’

&

New Marketing For A New Market

Before it first entered Tennessee, Listerhill surveyed its marketplace awareness in Maury County and found it totaled approximately 4%, according to Mashburn.

We’ve since grown tremendously from a brand recognition standpoint, she says.

But it wasn’t time that got Listerhill there, it was strategy. Listerhill knew it needed to better understand both the population and the competition. Mashburn, in particular, had a strong grasp on both, as she commutes to Alabama from Tennessee.

Much like the Alabama city of Florence, home of the University of North Alabama, Columbia, TN, is undergoing a community resurgence focused on supporting local farmers, artists, and businesses. Recognizing the similarities between these two markets, Listerhill refurbished the Pick Five campaign it had used several years ago.

Pick Five checking allows new account holders to donate $50 to a local school of their choosing. Mashburn says the campaign is most effective when her team can attend school events like football games and parent-teacher conferences.

It’s also more cost-effective than other forms of advertising, helping Listerhill open more than 1,100 new accounts and process more than 7.4 million new loans year-to-date. Maury County is one of 13 counties included in the Nashville metropolitan statistical area, which means the credit union would pay full price for 1/13th of the total audience.

Instead, Listerhill focuses on event-based marketing that ties into its mission or a specific goal, including increasing awareness of how Pick Five raises money for the local school system.

We try to be at every local event, Mashburn says. We’ll go to local community events in Tennessee, jump on the microphone and say, We’re a credit union. If you’re helping the community you’re doing something we want to support, so come talk to us.’

As of November, approximately one-fourth of all the requests Listerhill received for financial support came from Maury County.

Challenges To Expansion

Listerhill wants to expand further into Tennessee, but according to Green, Tennessee regulators are more critical about expansion. Although the credit union entered the Volunteer State in 2012, regulators have not yet granted permission to expand that footprint.

Currently, lack of precedent is the main stumbling block. The Southeastern Regional Cooperative Interstate Agreement meant to promote interstate commerce and cooperation among credit unions in Alabama, Florida, Georgia, Mississippi, Missouri, North Carolina, and Tennessee is less than 10 years old. Green believes Listerhill is the first Alabama state-chartered credit union to expand into Tennessee.

I want everything yesterday, jokes CFO Morgan. And if I can’t have it yesterday, I want it tomorrow. The regulator’s timeline is more elongated, I think.

In the meantime, Listerhill is committed to growing the communities it does serve as it waits to move its front line forward in Tennessee.