As dwindling deposits cast a shadow over the financial industry, credit unions may find themselves fighting for every dollar, challenged to maintain liquidity, and unable to leverage their cheapest source of funding for loans.

While most competitors battle for consumer deposits, a more strategic deposit-building move may be to focus on merchant services. As a non-interest income generator, a quality merchant services program can help credit unions grow their commercial book of business while capturing a new stream of deposits.

The downturn in deposits can be tied to consumers desire to earn a better return than what most traditional checking accounts offer them. Many checking accounts are considered a layover stop for paycheck funds on their way to more attractive destinations, such as healthcare spending accounts, peer-to-peer payment tools, savings tools, money market funds, or high-yield savings accounts.

Further complicating the situation is the rise of digital-only competitors capable of offering attractive deposit interest rates. For example, one online bank offered rates 25 times higher than the industry average in 2018. Thanks to low overhead costs and tech-driven efficiencies, these digital players are capturing deposits that have historically been a brick-and-mortar credit union’s bread and butter.

Without a solid foundation of deposits, credit unions must turn to more expensive funding sources for lending or reduce lending altogether, which would negatively impact profits. For many credit unions, the growing strain on liquidity and capital requirements is worrisome.

There are many ways to compete for deposits, but one potentially overlooked growth strategy is leveraging a merchant services program. By leveraging a merchant services program, credit unions have a tremendous opportunity to gain deposits from retail stores, hospitals, hotels, restaurants, public works, and other businesses that regularly accept payments during their day-to-day operations.

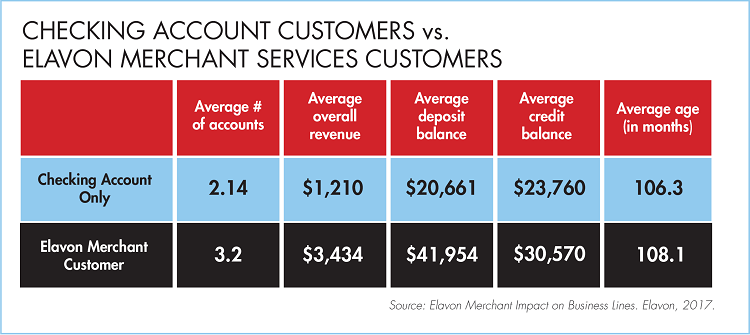

Not only is there an abundant opportunity in the merchant space, that opportunity comes with real benefits to a credit union’s deposit base and revenue goals. While not guaranteed, data from merchant services provider Elavon suggests members that utilize its solution have deposit balances on average two times higher than members with just checking accounts.

Revenue-wise, these members generate three times more than their checking account-only counterparts. These members are also typically stickier, averaging three solutions with their credit union compared to an average of two solutions among those with only checking accounts.

To capitalize on the merchant services opportunity, credit unions must provide a quality program that caters to the unique needs of payment-accepting businesses. Some items to consider when implementing or fine-tuning a merchant program include:

- Culture and brand alignment: Successful partnerships between credit unions and merchant services solution providers occur when both parties share the same culture.

- Program onboarding: Credit unions can start off on the right foot by facilitating a positive onboarding experience. A strong merchant services program should utilize digital applications and efficient processes that decrease overall onboarding time and speed up the first date of deposit.

- DDA deposit speed: Businesses benefit from swift access to their daily earnings. A sound merchant services program should quickly place member funds into their chosen demand deposit account (DDA).

- Additional business solutions: To maximize the value of a merchant services program, credit unions can offer additional business solutions, such as a business credit card and commercial card.

Partnering With Elan Advisory Services

Elan Advisory Services can provide expertise on deposit-building strategies, including how to bolster deposits with a merchant services program. Credit unions that engage with Elan Advisory Services have access to Elavon, one of America’s leading merchant solution providers. Elavon offers a range of software solutions, mobile and tablet-based solutions, ecommerce offerings, POS terminals, and loyalty programs designed to meet the needs of numerous merchant industries.

Boasting a best-in-class onboarding process, Elavon provides a concierge service that is focused on decreasing the number of days to activation, thereby increasing the speed to earning revenue. The member experience is further enhanced through beneficial program features such as loyalty programs, same-day funding, reporting tools, and robust security.

To learn more about building deposits with a merchant services program, click here to download a complimentary whitepaper.

About Elan Advisory Services

Elan Advisory Services provides strategic consultation to ensure your credit union has the right products and services to compete in your market. Through Elan Advisory Services’ internal partners, we deliver best-in-class products and exceptional service to more than 3,000 financial institutions across the United States. With solutions such as end-to-end agent credit card services, mortgage services, and merchant processing, Elan Advisory Services can help your credit union increase revenue and efficiencies. For more information, visit Elan Advisory Services at www.elanadvisoryservices.com.