Payment cards have grown in importance at credit unions over the past few years, and the following data illustrates the current performance and future potential for credit cards,debit cards, and other subsections of the payments ecosystem. Read on to see how your institution might further benefit from these valuable business lines.

CREDIT CARD PERFORMANCE

The credit union credit card portfolio has changed dynamically over the past decade. Historically, credit cards were not a major source of revenue for many cooperatives, but member demand along with high yields in a low-rate environment has increased the attractiveness of this line of business.

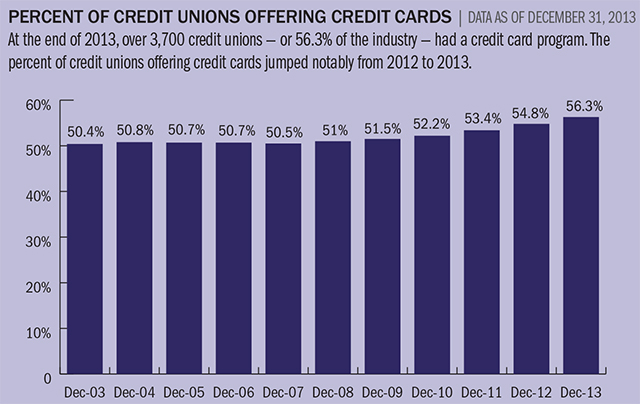

More than 56.3% of the industry today offers credit cards to members; that’s up from 50.4% 10 years ago. Given the rising importance of credit cards in the industry’s loan portfolio, it is not surprising credit card concentration is also increasingand has topped 6.6% as of year end 2013.

Although the pace of balance growth slowed after the financial crisis, this metric is regaining momentum amid an improving economy. Total outstanding credit card balances have increased 7.7% in 4Q13 to reach $43 billion, marking the highest year of annualcredit card loan growth since the recession. The average credit card balance also increased 69 basis points year-over-year to reach $2,771 as of the fourth quarter.Moreover, the total number of credit card accounts has steadily increased to top 15.5 million.

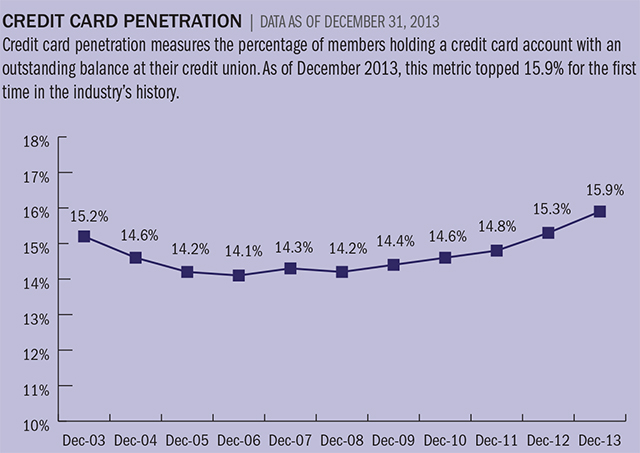

Credit card penetration was generally in decline prior to the financial crisis. However, since 2011, the percentage of members holding a credit union credit cardhas been growing. What’s more, the average credit card rate at credit unions has trended downward since 2009 despite concerns that the Credit CARD Act would cause financial institutions to raise interest rates.

DEBIT CARD PERFORMANCE

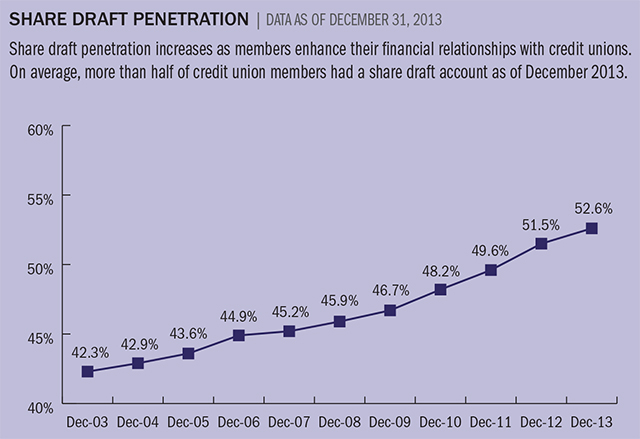

Because credit unions do not report account or transaction-level data on debit cards to the NCUA, Callahan & Associates uses share draft accounts as an indicator of creditunion debit card performance. Share draft products whether structured as free or rewards-based are perhaps the most important tools credit unions have to attract and retain members. It is important to track share draft penetrationbecause this metric helps gauge members’relationships and level of interaction with the credit union. If a member is satisfied with their credit union share draft account, they are more likely to use other products and services.

Over the past decade, share draft penetration has consistently increased at credit unions. The industry average for share draft penetration topped 52.6% as of 4Q13, up 6.7 percentage points from five years ago and up 10.3 percentage points from 10 yearsago.

Annual growth in the number of share draft accounts has outpaced membership growth, leading to an annual increase in share draft penetration. The 7.0% annual growth in the number of share draft accounts was nearly three times greater than the 2.5% annualmembership growth reported in the fourth quarter of 2013. Credit unions have excelled in growing share drafts, but they still have ample room to improve penetration, as half of all credit union members do not hold a share draft account.

Credit unions often offer debit cards to members when they open a share draft account under the general belief that once a member has a debit card, they will use it and generate interchange income for the credit union. And debit card interchange fees,listed under other operating income on the call report, has indeed been one of the major sources of non-interest income for credit unions. According to Callahan & Associates’ 2013 Non-Interest Income Survey, debit card interchange and fees wasthe second-largest component of this income type and accounted for 22.0% of total non-interest income at credit unions. All but a handful of credit unions are exempt from the Durbin Amendment, which limits debit interchange fees, yet credit unionsof all sizes are feeling the indirect effects this pricing squeeze is having on the market.

PREPAID, MERCHANT PROCESSING, AND EMV

The prepaid market offers one area in which there is new opportunity for credit unions. Prepaid payment options allow a consumer to load money onto a card for use in point-of-sale transactions. When the consumer exhausts available funds, they must re-loadthe card. This gives the consumer the convenience of a payment card without the ability to overdraw an account. According to MasterCard’s 2012 Global Prepaid Sizing Study, the U.S. prepaid market is expected to grow at an annual rate of 16% through2017 and top $421 billion within three years. Despite the strong potential for prepaid in the United States, few credit unions currently offer this option to their members.

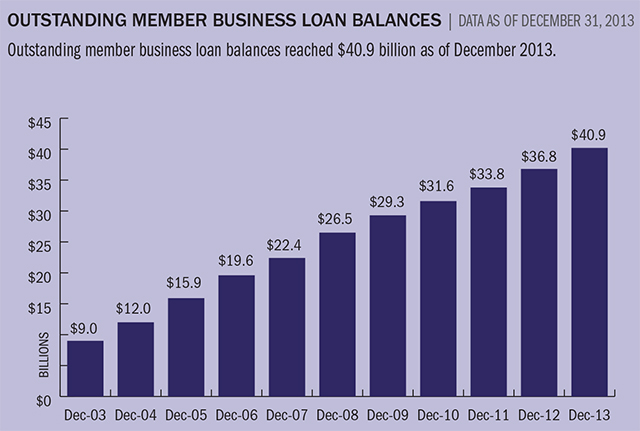

Merchant processing is also playing an increasingly integral role in the payments sector of credit unions. A growing number of credit unions that are working to build and enhance their relationships with community businesses are entering into or expandingexisting member business lending (MBL) programs. MBL is particularly attractive for institutions with low-income designation, which allows additional lendingcapacity beyond traditional MBL caps. And payment processing solutions allow credit unions to provide a full suite of services to these businesses and attract more holistic merchant relationships.

Payment technology and security provides yet another new opportunity for credit unions. Although more than 80 countries around the world have abandoned magnetic stripe cards in favor of the more secure Europay-MasterCard-Visa (EMV) chip standard, mostAmerican ATMs and merchants are not currently equipped to handle this technology.

Soon, however, EMV will be accepted as frequently in the United States as in other countries. That’s because major card companies are shifting the liability for non-EMV transactions. After October 2015, the liability for fraud will shift from cardissuers to merchants who have not adopted a terminal to read EMV-enabled cards. A credit union that does not convert to EMV cards, on the other hand, will retain responsibility for the financial consequences of fraudulent card transactions made withoutthe technology.

Although the cost of replacing traditional magnetic stripe cards will not be insignificant, EMV is poised to generate huge cost savings through decreased fraudulent transactions.In fact, an estimated 90% of counterfeit card fraud could be eliminated through EMV deployment, according to Aite Group. Increased safety in the payments space is also likely to improve consumer experiences and increase member satisfaction.