Read the full analysis or skip to the section you want to read by clicking on the links below.

LENDING AUTO LENDING MORTGAGE LENDING CREDIT CARDS MEMBER BUSINESS LENDING SHARES INVESTMENTS MEMBER RELATIONSHIPS EARNINGS SPECIAL SECTION: CUSOS

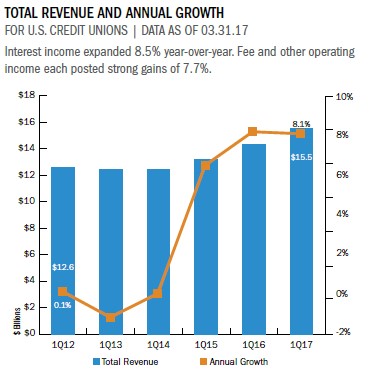

Total revenue reached $15.5 billion in the first quarter of 2017. That’s up 8.1% year-over-year from the $14.3 billion credit unions posted in the first quarter of 2016. Improvements in interest income largely drove this growth. Interest income increased 8.5% year-over-year to $11.4 billion. However, non-interest income, which posted an annual growth rate of 5.7%, also contributed to the rise in total revenue. As of March 31, 2017, interest income comprised 73.1% of revenue, whereas non-interest income was responsible for 27.5%.

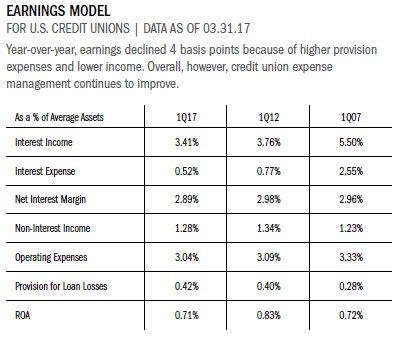

Interest income and interest expense as a percentage of average assets increased 3 and 1 basis point over the past year to 3.41% and 0.52%, respectively. As a result, between first quarter 2016 and first quarter 2017, the net interest margin rose 2 basis points to 2.89%. Non-interest income as a percentage of average assets posted a slight decrease. It was down 3 basis points to 1.28%. However, non-interest expense turned out an even larger decrease. It was down 4 basis points to 3.04%.

With increased loan volume, credit unions have increased their provision expenses. Provisions for loan losses accounted for 0.42% of average assets in the first three months of the year. This represented a 7-basis-point rise over last year’s 0.35%. The increase in withholding for the provision expense has had the largest impact on ROA, which fell 4 basis points year-over-year to 0.71%.

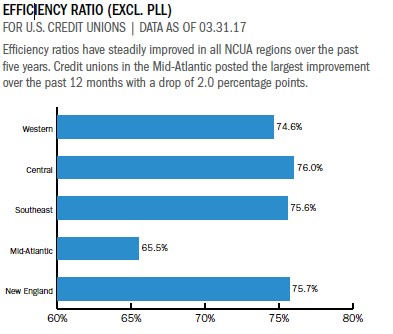

To contextualize the earnings model, it is important to note that assets grew 7.9% year-over-year. Some of the earnings categories either grew at the same pace or lagged slightly, which can partially account for the dip in ROA compared to last year. Credit unions have improved their efficiency (excluding provisions for loan losses), which dropped from 74.6% in first quarter 2016 to 73.3% in 2017.

From a capitalization perspective, the industry remains well above the well capitalized requirement from NCUA; 96.7% of credit unions had a net worth ratio above the 7% threshold set by the NCUA. Credit unions nationally posted a 10.7% net worth ratio at the end of first quarter 2017.

Click the graphs below to enlarge and then continue reading to see how Commonwealth Credit Union finds an avenue for non-interest income that doesn’t require raising rates or fees.

Larger institutions underpinned the growth in average loan balances across the country. Whereas the median growth rate increased 2.8 percentage points, credit unions in the top 20th percentile posted gains of 9.6% per loan.

CASE STUDY

COMMONWEALTH CREDIT UNION

For Commonwealth Cre d i t Union, earning enough to keep the lights on while charging reasonable rates and fees remains a critical operational balance.

If I said non-interest income was very, very important,’ that would still be an understatement, says Commonwealth’s vice president of lending, Alan Davis.

Commonwealth’s non-interest income as a percentage of assets stood at 1.64% as of March 31, 2017. That’s stronger than credit unions in Kentucky as well as credit unions with more than $1 billion in assets, which reported first quarterratios of 1.40% and 1.24%, respectively, according to data from Callahan & Associates.

To earn non-interest income, Commonwealth focuses on income from insurance products, including credit insurance products the institution has offered for more than three decades.

Kentucky’s economic hardship has made Commonwealth’s credit insurance more than a steady source of non-interest income for the credit union it’s made the product a valuable lifeline for members facing grim financial realities.

It’s not just a cross-sale product that generates income, Davis says. It’s a way to improve our members’ financial well-being.

Commonwealth offers two different insurance offerings credit life and credit disability as either standalone products or joint products on all loan products and bases the monthly premiums on the size of the loan.

An incentive structure encourages team members to keep the products at the forefront of member interactions. Incentives are based on the first month’s premium; therefore, team members who sell insurance on larger loans receive higher incentives.According to Davis, incentives run from $25 to as high as several hundred dollars.

Incentives are a way to encourage team members to offer our product to all of our members, Davis says. It’s not something you can get rich from.

Read The Whole Story

RETURN TO INDUSTRY PERFORMANCE BY THE NUMBERS 1Q 2017