Firefighters First Credit Union ($954.5M, Los Angeles, CA) expects to make $250,000 in net income this year from its in-house insurance agency, a revenue stream the California credit union expects to push to $1 million per year in the not-too-distant future.

The credit union which has five branches in Los Angeles and Northern California and primarily serves professional firefighters and their families opened Firefighter Insurance Services in 2010 and currently offers 4,800 auto, home, commercial, motorcycle, RV, boat, umbrella, life, and earthquake policies from 10 different insurance companies, including Mercury, CSE, and Safeco.

CU QUICK FACTS

FIREFIGHTERS FIRST Credit Uniondata as of 3.31.15

- HQ: Los Angeles, CA

- ASSETS: $954.5M

- MEMBERS: 31,587

- BRANCHES: 5

- 12-MO SHARE GROWTH: 7.87%

- 12-MO LOAN GROWTH: 16.54%

- ROA: 0.75%

The credit union’s president and CEO, Mike Mastro, says the insurance agency serves two goals. First, it creates a reliable source of non-interest income; second, it provides members and non-members alike an essential product under a brand they trust.

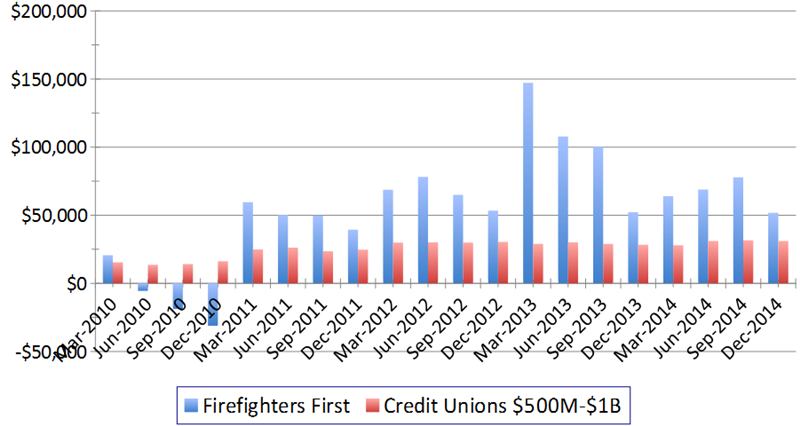

Firefighter Insurance Services achieved profitability within 18 months of its launch and has helped Firefighters First Credit Union post strong performance since. For example, the credit union’s net income per FTE has risen from below its peer average five years ago to now sharply higher than peers, according to data from Callahan Associates.

We’ve always felt there was an opportunity to derive value from the marketplace and share that with the membership, Mastro says.

There’s more to come, too. Firefighters First owns the agency under a holding company structure and is focused on growing additional non-interest income through acquisition and organic growth as opportunities arise.

Net income Per Full-time Employee

For all U.S. credit unions |Data as of March 31

Callahan Associates | www.creditunions.com

Source: Callahan Associates’ Peer-to-Peer Analytics

From The Beginning

|

| Mike Mastro, CEO, Firefighters First Credit Union |

During the past recession, margin compression and growing competition forced Firefighters First then Los Angeles Firemen’s Credit Union to consider new income streams.

We believed there were positive, non-punitive ways to grow non-interest income, Mastro says. You just have to be creative in discovering where they are and what their risk profiles are to ensure the business is sustainable and will grow.

The credit union researched its options, brought in its board, and created an insurance agency in partnership with a 50-year-old firm that focuses on firefighters and other civil servants as its customer base.

We are 51% owners, Mastro says. From the beginning we felt it was important that we had appropriate control of what we were doing.

You Might Also Enjoy

- How To Buy A Participation Loan

- 3 Strategies To Manage Liquidity

- Earnings Performance By The Numbers (3Q 2015)

- How To Make Investments Pay Dividends

Along Insurance Lines

Firefighters Insurance Services combines the institutional knowledge and back-office operations of its partner Crusberg Decker Insurance Services, a company owned by the family of a Pasadena battalion chief and the internal expertise the credit union has developed as the operation has grown to comprise a CEO, a commercial underwriter, and two front-line staffers.

Firefighters First markets the policies through the agency’s own website as well as through regular conversations its staff has with members.

When someone comes in for a home loan, we’ll talk to them about insurance on their home, Mastro says. Our members tend to like the idea of wrapping those two things together around a brand they trust.

When someone comes in for a home loan, we’ll talk to them about insurance on their home. Our members tend to like the idea of wrapping those two things together around a brand they trust.

The same thing happens with commercial insurance, which along with auto and home are Firefighters Insurance Services’ three most popular lines.

Member business lending is a big deal at Firefighters First. Its portfolio of $78.7 million more than doubled the $38.9 million average for the 231 credit unions with $500 million to $1 billion in assets at year-end 2014.

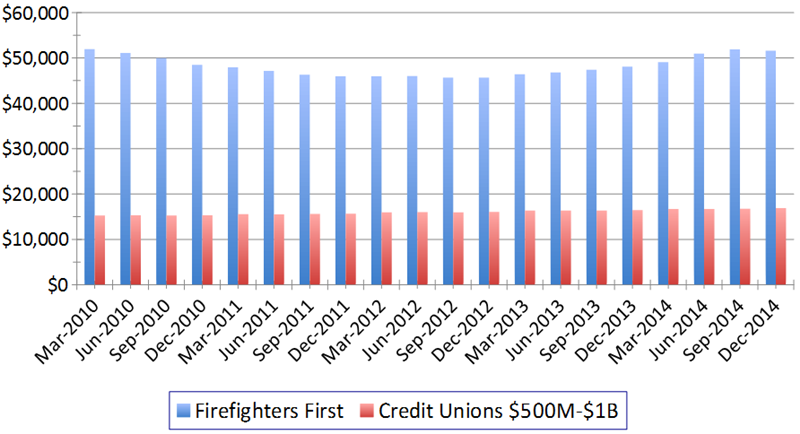

That exemplary performance carries over to Firefighters First’s average member relationship, which was $51,612 in 2014 compared with $16,892 for its peer group, according to Callahan data. Meanwhile, its loans per member was 1.05, twice the peer average, and its average loan balance per employee was $25,545, also twice the peer average as well as fourth highest among its peer group.

Loan Balance Per Employee

For all U.S. credit unions

Callahan Associates | www.creditunions.com

| Rank | State | Credit Union | December 2014 | December 2013 | Growth |

|---|---|---|---|---|---|

| 1 | NY | Progressive | $21,700,178 | $20,567,616 | 5.51% |

| 2 | NY | NCPD | $9,820,755 | $9,609,147 | 2.20% |

| 3 | IL | Deere Employees | $7,043,737 | $6,483,216 | 8.65% |

| 4 | CA | Firefighters First | $6,243,635 | $5,802,027 | 7.61% |

| 5 | NY | Quorum | $6,122,346 | $5,770,236 | 6.10% |

| 6 | PA | APCI | $5,769,088 | $6,004,171 | -3.92% |

| 7 | UT | Utah Power | $5,011,537 | $4,880,402 | 2.69% |

| 8 | MA | St. Mary’s | $4,832,032 | $4,215,285 | 14.63% |

| 9 | IL | Motorola Employees | $4,687,000 | $4,506,406 | 4.01% |

| 10 | NV | Boulder Dam | $4,662,773 | $4,585,951 | 1.68% |

Source: Callahan Associates’ Peer-to-Peer Analytics

Average Member Relationship

For all U.S. credit unions | Data as of March 31

Callahan Associates | www.creditunions.com

Source: Callahan Associates’ Peer-to-Peer Analytics

The credit union also has a 99.92% loan-to-share ratio, according to year-end Callahan data. Perhaps most importantly, its Return of the Member score of 100 is tops in its peer group nationwide. That’s Callahan’s measure of product usage and value and Mastro says member value is what it’s all about.

Our board insists that quality of service and service to the member drive every decision we make, Mastro says. Our members obviously appreciate that and we intend to protect that relationship while using it to boost our bottom line.

A Cooperative Concept

Firefighters First expects its internal business to continue growing and has now begun creating insurance agencies for other credit unions. It has launched four so far and has two more in the pipeline. The credit unions can enter a 51/49 ownership deal, with Firefighters Insurance Services as the minority partner, or they can become a referring agency and commit a share of the commission but not contribute capital.

Mastro says those credit unions are all in the Los Angeles area. He intends to move at a measured pace, adding perhaps two to four new partners a year as his credit union exceeds the billion-dollar mark in assets and the insurance business moves toward adding $1 million a year in net income.

That’s while continuing to look for other ventures, as well.

We’re on a quest to understand what’s in the marketplace in terms of additional non-traditional businesses, Mastro says.

This article originally appeared on CreditUnions.com on June 1, 2015.

Four Tips To Ensure Insurance Success

Firefighters First CEO Mike Mastro says moving into a new line of business can be disconcerting. That’s why he offers this advice for credit unions considering it:

- If it’s important to the credit union, make sure someone owns it. It has to become an important part of who you are and what you believe is important, Mastro says.

- Ensure the board down through the management team discusses and embraces the idea. Everyone has to be aligned and in support of what you’re doing, Mastro says.

- Ensure the front-line staff is on board. You have to put appropriate incentives in place for your staff to be attentive, Mastro says.

- Ensure you educate staff on the products as they’re rolled out and as they change. Education around our insurance program especially to our members while they’re in front of us is an important part of our success, Mastro says.