Plastic has long been pivotal to the payments strategy at DuPont Community Credit Union ($978.34M, Waynesboro, VA), as evidenced by the Virginia credit union’s peer-busting metrics in credit card penetration and portfolio (see slideshow)

CU QUICK FACTS

DUPONT COMMUNITY CREDIT UNION

Data as of 06.30.15

- HQ: Waynesboro, VA

- ASSETS: $978.34M

- MEMBERS: 73,112

- BRANCHES: 10

- 12-MO SHARE GROWTH: 7.41%

- 12-MO LOAN GROWTH: 7.81%

- ROA: 0.70%

Building on that momentum, DCCU is now doubling down on digital, using business intelligence to drive campaign strategies and launch a new mobile app that features dashboards designed to drive and reward spend.

Mike Tranum, DCCU’s vice president of information technology, says it’s all part of a business strategy that focuses on acquisition, usage, retention, and onboarding. Launching Apple Pay support was one piece of that puzzle, so was bringing on Michael Weiss in January as director of card services.

We had always treated our card portfolio as an operational department, Tranum says. But we felt it was time to focus more on the analytical side of what we could be doing across all our channels: retail, call center, and digital.

Slice, Dice, And Serve The Specials

When the credit union analyzed its regional and national card-issuing competitors, it uncovered several opportunities.

The first thing we did in 2015 was introduce new pricing on credit card accounts, Weiss says.

DCCU also introduced a pre-approval campaign aimed at members who did not carry the credit union’s credit card. DCCU enhanced the campaign’s email blasts, outbound calling, and retail staff sales contests with specifics about individual members’ qualifications for credit lines and other parameters.

The result was a 6% response, our highest response rate ever and the most new accounts 970 that we ever generated in a two-month campaign, Weiss says.

A second campaign focused on members who had dormant credit card accounts including cards not used for 12 months as well as those that had never been activated. DCCU further segmented variables such as frequency of use and average spend to personalize offers that included combinations of credit line increases and 2% cashback or double rewards.

We sent out a mailer and followed that up with an email blast and the result was an 18% increase in June and July card usage for those members compared with the same two months one year ago, Weiss says.

A New App With Dashboards That Deliver

Five years after its first foray into mobile, DuPont Community launched a new app in August 2015 available for iPads, iPhones, Android phones, and Android tablets.

We treat our credit card like any other account and give our mobile users a complete picture inside the same interface, Tranum says. That includes viewing balances, scheduling payments, anything the member would typically want to do.

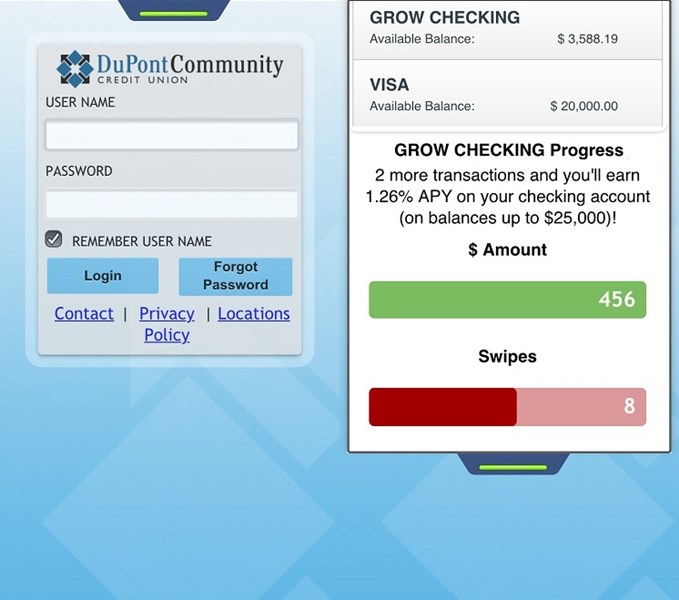

The new app also includes a dashboard that gives members online or on the app a graphical view of balances and rewards activity on debit accounts.

Our users can look at their app and see if they spend $114 more, they’ll hit the double rewards level, Weiss says. It can drive a spending decision. We’re seeing that.

Tranum agrees, saying the rewards products have been around for years but the graphical presentation is empowering an overall increase in debit card usage and checking product adoption.

DCCU recently deployed its online version of the rewards and balances dashboard.

DCCU’s mobile dashboard shows members how much they have and what they need to spend to earn more rewards. It’s part of the credit union’s new mobile app.

The Voice Of The Member

DCCU began supporting Apple Pay in May and now has approximately 500 members enrolled, members who originated more than 2,700 transactions averaging $18 to $20 per ticket in August. Tranum says the credit union will offer Android Pay and Samsung Pay, too, when those payment apps become available.

We want to be there for the member in all the channels they want to use, the DCCU executive says. If you’re going to wait for a winner in the payment space, you’re going to be waiting forever. Offer them all and the winner becomes irrelevant.

But DCCU isn’t offering these mobile wallets just for the sake of it. It is listening to the voice of its members.

In fact, the Voice of the Member is a new program for collecting feedback from members using the retail and call center channels. Before the credit union launches new electronic products, it tests them among employee focus groups composed of varying ages, genders, and other demographics.

That combination of employee and member feedback can reveal some unexpected areas of service improvement. Changing the credit card reissue process is one example, Weiss says.

We kept hearing that online retailers were going by the first day of the expiration month rather than the last day, and that was causing some cards to be rejected, says the DCCU cards director. So we now extend the window for renewals to eight weeks before the plastic actually expires.

That kind of agility does not happen by accident.

You have to constantly evolve your processes and procedures based on industry trends and what you’re learning from and about your members, Tranum says. There’s no such thing here as set and forget.

Strategy Of Segmenting

Michael Weiss, director of card services, shares six reasons why DCCU is focusing on segmenting its card portfolio.

- Michael Weiss, director of card services, shares six reasons why DCCU is focusing on segmenting its card portfolio.

- It helps the credit union understand its current portfolio composition and baseline the portfolio’s performance.

- It helps the credit union formulate treatments or promotions that are more relevant to the member.

- It maximizes marketing investment per account.

- It identifies the biggest opportunities.

- It helps the business lay out the strategic roadmap.

- It introduces a more quantitative approach.

You Might Also Enjoy

- 3 Tips To Price For Risk And Profitability In The Card Portfolio

- How To Get Ready For Speedier ACH

- How To Keep Pace In A Changing Payments Space