Ongoing changes in the regulatory, competitive, and economic landscape are driving many credit unions to review their credit card program strategy. Some issuers are evaluating whether to invest in growing an insourced program versus exploring an outsourced solution. When weighing this decision, credit union executives should consider:

- The true cost of a credit card program

- Program loss trends

- Meeting member expectations

Uncovering The True Cost Of A Credit Card Program

To accurately evaluate a card program’s total return and efficiency, it is critical to burden program financial statements with all expenses not just processing costs, rewards program management, and network dues. Credit unions must also factor in expenses related to risk, fraud, collections, disputes, third-party provider relationships, compliance, and ongoing investments in product suites and digital integration. Often, credit unions find that with all factors considered, the total cost of an insourced card program is considerably higher than initially assumed.

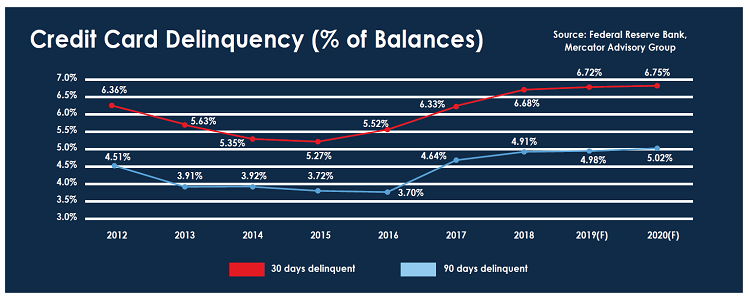

Evaluating Loss Trends

The credit card industry has experienced historically low losses since the Great Recession, but these loss levels may not be sustainable. Self-issuers must ask themselves if they have the ability to nimbly address changing risk dynamics in their portfolio and modify underwriting criteria to manage fluctuating performance across the risk spectrum. Credit unions with an insourced credit card program should complete a sensitivity analysis on returns to test robustness and vulnerability of the portfolio against scenarios such as increased losses, and even doubled losses.

Meeting Member Expectations

Members with the best risk profile typically want the best returns from their credit card and are most likely to get ongoing offers from national issuers. These same issuers are driving up the value of rewards programs. To compete, credit unions must not only offer a strong rewards program, but must also evaluate the program and suite of cards offered over time and adjust the rewards structure to meet the changing needs of members.

Keep in mind, not every member may value rewards. Therefore, a credit union’s card program must also offer a value proposition and marketing strategy that goes beyond rewards or risk adding expense without driving spend. Digital servicing capabilities and marketing the right product to the right members can help create a more comprehensive portfolio management strategy designed to optimize results.

When To Consider An Outsourced Solution?

There are several questions credit unions can ask about the future of their card program that will help them determine if exploring an outsourced solution makes sense, including:

- Can the credit union maintain a competitive credit card program long term?

- Can the credit union invest in digital capabilities to meet member expectations?

- Does the credit union have resources to manage program credit and fraud risk in a changing economy?

If the answers to these questions are unsatisfying, it may be time to evaluate the benefits of an outsourced partnership.

Many credit unions are hesitant to explore outsourcing because they fear losing control over the member experience, but a quality partner should understand the credit union’s culture and provide program visibility and ownership. A successful partnership allows credit unions to leverage the expertise, scale, and investments of the issuing partner and experience relief from expenses and concerns related to managing a credit card program

To learn more, download the complimentary whitepaper titled Insourcing vs. Outsourcing: Would a Credit Card Partnership Be Beneficial? from Elan Financial Services.

Partnering with Elan Financial Services

Elan Financial Services offers a holistic credit card program that focuses on the individual needs of the credit union, with serving members effectively as the ultimate goal. Partner credit unions can provide members with desired digital capabilities and rewards without upfront investment. In addition, Elan’s comprehensive fraud prevention program keeps fraud losses low per event compared to other industry players. Elan also takes on the compliance and regulatory burdens associated with running a credit card program, so credit unions can focus on members. For more information, visit www.cupartnership.com.