Advancements in payments technologies have forever changed member expectations. Digitally minded shoppers now seek real-time solutions that enable quick, easy purchases and payments using online tools and mobile apps. More than ever, they demand financial services in step with their busy, mobile lives.

Credit unions must respond with products and services that deliver new levels of convenience, freedom, and control. By enabling secure and easy digital transactions through debit and credit cards, credit unions can continue to remain relevant to members.

Here are four steps for differentiating a card program.

1. Digitize

Develop and deploy digital solutions, including wallets, alerts, and card controls, that provide an integrated, seamless, and efficient payments experience.

Members have an array of choices for their financial services, and they will go where they find the greatest value. Nonfinancial competitors are adept at capturing consumers via embedded payment options that deliver a streamlined experience. Their goal is to gather cardholder information, cross-sell new services, and extract a growing share of the payments value chain.

Developing a digital strategy focused on driving deep member engagement can help credit unions ensure their cards remain top-of-wallet. Digital wallets are the place to start.

The adoption curve for digital wallets is strikingly similar to that of online banking in its early years. This suggests a sharp rise in the use of digital wallets is on the way. The following research data confirms digital wallets’ growing popularity with retailers and consumers:

- A majority of the largest retailers now accept contactless payments (Boston Retail Partners, 2019 POS/Customer Engagement Survey)

- One in six U.S. banking consumers says they have paid with a digital wallet within the past 30 days (Fiserv Expectations Experiences: 2018 Consumer Payments Survey)

- 72% of cardholders say paying for purchases is more convenient with tokenized mobile payments (Mercator Advisory Group, Mobile Payments: Greater Value Needed for Widespread Adoption, Customer Monitor Survey Series, Insight Summary Report Volume 7, Report 2, 2017)

With available digital tools and others that are rapidly emerging, such as merchant-based geographic reward offers credit unions can deliver significant benefits to members and reap measureable returns.

2. Utilize

Provide members with comprehensive information about how digital solutions can meet their expectations and needs.

By implementing digital tools and providing a frictionless financial service experience, you can empower members to transact in real-time on one or multiple devices including mobile phones, computers, and tablets.

But new digital tools only provide value when members understand their benefits and know how to use them. Once digital products and services are implemented, communications programs are important to encourage adoption and use.

3. Securitize

Balance digital innovation with risk mitigation strategies that keep members safe without disrupting transactions.

Digital payments are highly secure due to tokenization a process in which numerical values replace members’ personal information for transaction purposes. Tokenized digital wallet transactions are an important first step toward preventing mobile payments fraud.

Moreover, mobile apps that enable cardholders to receive transaction alerts and actively manage card usage are significantly improving card security. Fiserv analysis shows use of a card controls app may reduce signature fraud by up to 53% while increasing card usage and spending.

Beyond the security benefits inherent in the technology, there is a need for strategies focused on detecting and preventing fraud in real time without impacting card usage and cardholder satisfaction. This can be a significant point of differentiation for credit unions.

The Federal Reserve System measures basis points (BPS) to convey the average value of fraud in comparison to total transaction dollars. A recent analysis from the Federal Register indicated debit fraud is running at approximately 11.2 BPS. Fiserv debit card clients are experiencing only 5.08 BPS of fraud.

Source: Board of Governors of the Federal Reserve System, 2017 Interchange Fee Revenue, Covered Issuer Costs and Covered Issuer and Merchant Fraud Losses Related to Debit Card Transactions, published 2019.

A prudent approach includes implementing predictive analytics and decision-management technology. And because members want to be involved in managing and protecting their accounts, they should have the option to create customized transaction alerts and controls. Finally, direct access to experienced risk analysts who work to identify evolving fraud threats can significantly improve overall results.

Card issuers are also confronted with balancing risk rules, which help mitigate fraud, against cardholder disruption due to falsely declined transactions. These lost transaction opportunities reduce revenue and increase reputational risk. An experienced risk mitigation partner can help credit unions achieve the right balance between fraud detection and member satisfaction in a way that maximizes profitability.

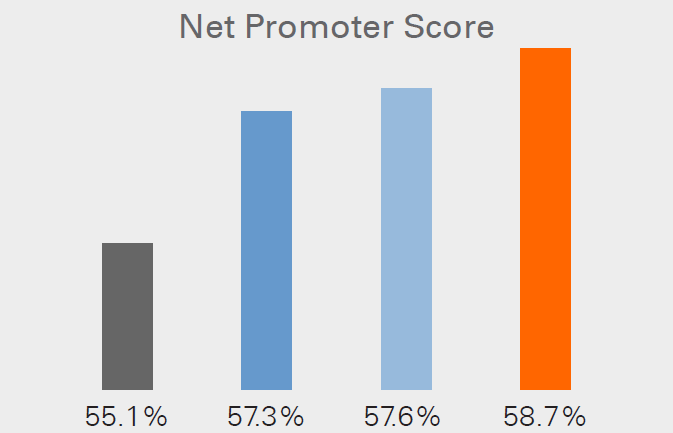

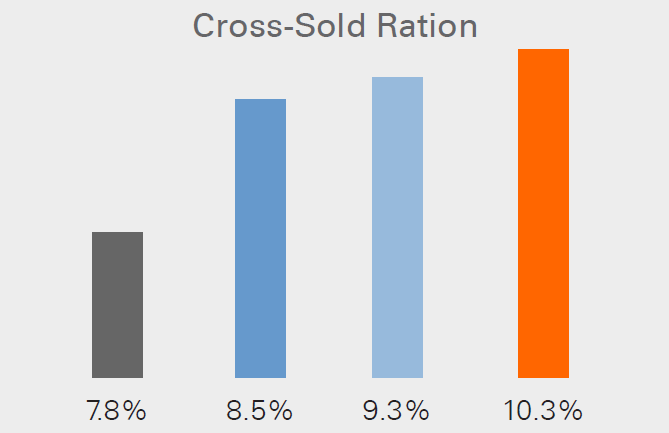

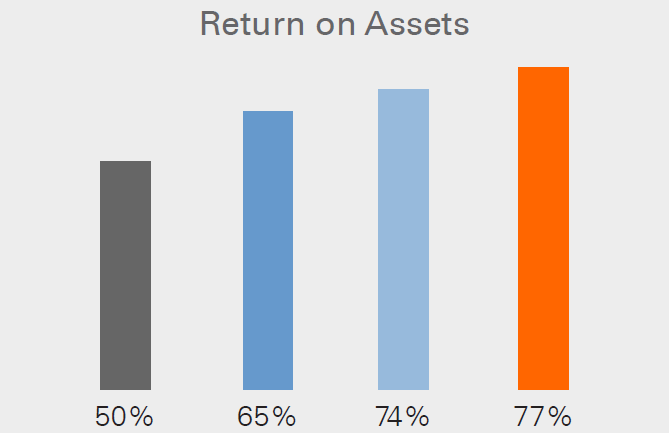

More Engaged Users Are:

HAPPIER WITH THEIR FINANCIAL INSTITUTION

BUY MORE PRODUCTS

MORE PROFITABLE

Based on these average monthly debit transactions:

Gray =Low 12.6

Blue = Casual (medium) 18.3

Light Blue = High 21.4

Orange = Super (highest) 28.4

Net Promoter Score = Measure of cardholder loyalty and value in institution relationship

Cross-Sold Ration = Percentage of householders with a DDA for longer than six months but open a new deposit or loan account in the most recent six months

Return on Assets = Percentage of profit related to earnings

4. Monetize

Turn digital solutions into engines of growth by creating stronger, more-lasting member relationships.

A digital portfolio can be more than just a set of solutions it can drive significant new revenue and growth opportunities. By delivering the secure, frictionless digital services members need, when and where they need them, credit unions can maintain their positions as trusted financial service providers. As The Raddon Performance Index, 2017 by Raddon, a Fiserv company has shown, engaged users are profitable users.

The -ize Have It

Digitize. Utilize. Securitize. Monetize. Achieving the right combination of innovative products and exceptional member experiences will enhance card portfolio growth, operational efficiency, and market share.

For more information, please visit Fiserv.com.