When executives at TruStone Financial Federal Credit Union ($1.0B, Plymouth, MN) decided to leverage retail branch staff for outbound cross-selling calls, even they couldn’t have predicted the enthusiastic response.

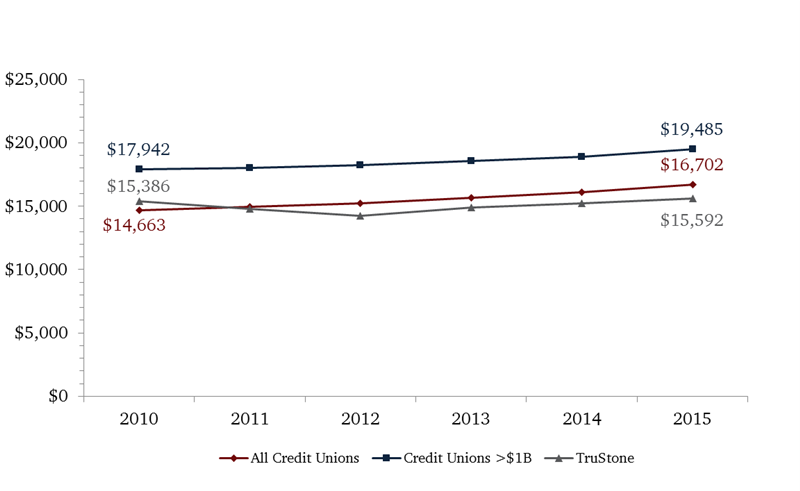

Through outbound calling and a focus on cross-selling additional products and services, credit unions across the country are capturing more of their members’ wallet share, as evidenced by the 37% growth in average member relationships over the past10 years.

AVERAGE MEMBER RELATIONSHIP

For FirstLook credit unions | Data as of 09.30.15

Callahan & Associates | www.creditunions.com

Source: Peer-to-Peer Analytics by Callahan & Associates

TruStone Financial has traditionally run all outbound calling through its contact center, supplementing these efforts through a third-party vendor during high volume campaign periods. In early 2015, management decided to deploy the credit union’sbranch network in a new calling campaign focused on building relationships with existing members.

CU QUICK FACTS

trustone financial FCU Data as of 09.30.15

- HQ: Plymouth, MN

- ASSETS: $1.0B

- MEMBERS: 90,832

- BRANCHES: 12

- 12-MO SHARE GROWTH: 6.43%

- 12-MO LOAN GROWTH: 17.52%

- ROA: 1.28%

Over time, TruStone Financial has built a sophisticated call center structure. The department employs three distinct positions. Phone Banker 1s take inbound member calls. Phone Banker 2s support this role as well as take inbound loan inquiries. PhoneBanker 3s concentrate on outbound calling to the credit union’s existing membership base, building deeper relationships around product marketing campaigns.

TruStone Financial has also introduced a separate TruPartner Network Team to develop relationships with local business partners, such as homebuilders. These partnerships allow TruStone to offer indirect and lifestyle financing options to their membersat point of sale.

The most recent addition to the calling team is the branch network. Since the beginning of the year, representatives at each of the cooperative’s 11 branches in Minnesota and Wisconsin regularly call their current members to offer additional productsand services and grow the relationship.

Characterizing its approach as a hybrid model, TruStone Financial also uses a third-party vendor, LSI, primarily to support overflow during heavy outbound calling campaign periods. Yet the credit union has seen its strongest results comefrom the branch staff, with response rates approaching 12-13% since the program began.

Through our transition to an in-house call program, we’ve seen better results than using a third-party because we know our members better than anyone else, says Jeff Smrcka, director of lending.

Smrcka and Lisamarie Meyer, vice president and director of Minnesota branches, visit each of their locations regularly to review outbound calling scripts, discuss campaign results, and provide coaching and mentoring to the branch management staff.

The most impactful part of the implementation of our in-house calls has been the enthusiasm of our employees and the success stories from our membership, Meyer says.

Through our transition to an in-house call program, we’ve seen better results than using a third-party because we know our members better than anyone else.

Using the Synapsys CRM system, the credit union mines its member database for opportunities. The credit union also leverages Experian credit bureau data as well as internal analytics to identify cross-sell opportunities for its calling lists.

As a recent example, Smrcka says, we scrubbed our entire membership looking for automatic payments that were coming out of TruStone checking accounts but going to other financial institutions.

When the cooperative tapped retail branch staff to make outbound cross-selling calls, it did so without setting specific goals. Retail employees are eligible for variable compensation through an organization-wide incentive program, but leadership focusesits efforts on motivating its sales team through coaching and friendly competition among branches rather than trying to tie success to specific metrics.

We don’t really have a magic number, Grindeland says. For us, it’s understanding the campaign, what our baseline is telling us and which way we’re trending.

It’s very difficult to set a percentage, Smrcka adds. The program is in place to make sure we have a positive environment for our employees. The focus is on benefitting our members and looking for opportunities to financiallyhelp them. The percentage takes care of itself if you focus on the member.

The credit union supports the branches by providing lists of leads, detailed calling scripts that cover nearly every possible scenario, and extensive staff development and training.

Marketing helps create the scripts, Grindeland says. They are comprehensive, 18 to 20 pages of options. We then use our staff development department to educate and coach our employees on these call scripts specifically and to talkthrough the marketing campaign to make sure everybody is on the same page.

We educate our staff to make sure they understand the entire relationship, Grindeland continues. We train our people to take the time before they call the member to understand what might be happening in their life or to notice ifthere is a bad address warning code on their account. It really does turn into a service call as much as it is capitalizing on a sales opportunity.

TruStone Financial has accrued several benefits in bringing its outbound calling program mostly in-house. These include cost savings as well as building an even deeper understanding of members.

When it’s TruStone calling, members recognize their financial institution and we have a better opportunity to have a conversation and build on the relationship, Meyer says. Our tagline is We’re the neighborhood credit union.’ It’s about reassuring people that we’re there for them, and our lines are always open.

If they had it to do over again, though, these TruStone leaders say they would have done a few things differently.

As we move forward and build on this initiative, we are looking for ways to become more efficient, use our existing capabilities, and plan for growth, Grindeland says.

Those successes have been impressive so far. For example, when a branch representative reactivated an account for a member with a dormant relationship, the member went on to open a new checking account and refinance a loan from another financial institutionfor substantial savings to the member.

Without this program in place, Meyer says, We could have lost that relationship entirely.

You Might Also Enjoy

- How Educators Insourced For Car-Buying Success

- Co-Sourcing: How 3 Credit Unions Collaborate On Back-Office Ops

- What To Consider Before Outsourcing A Credit Card Program

- 6 Questions To Ask Before Outsourcing