Total operating revenue reached $31.7 billion in the first half of the year; that’s an increase of 8.8% over the first six months of 2016. This continued the recent trend of accelerating revenue growth for credit unions.

Interest income totaled $23.1 billion for the first six months of the year, representing annual growth of 9.7%. Non-interest income grew at a slower 5.8%. Relatively strong fee income growth of 7.4% as opposed to other operating income growth of 5.7% drove second quarter NII.

The industry’s income composition so far in 2017 remains consistent with previous years. Net loan income accounted for 63.9% of total revenue at $20.3 billion through the first six months of the year. ContentMiddleAd

Comparatively, investment income grew faster than any other component of the earnings pie. Its growth rate picked up 56 basis points and jumped from 8.4% at mid-year 2016 to 8.9% at mid-year 2017.

As interest rates gradually rise, the margin at credit unions across the country likewise slowly improves. The net interest margin for the industry has increased 5 basis points over the past 12 months to reach 2.93% as of second quarter 2017. This rate marks a 16-basis-point improvement over the 2.77% from second quarter 2013.

Credit unions once again posted gains in efficiency, thanks in part to a keen eye trained on expense management. As such, the operating ratio decreased 3 basis points year-over-year to 3.06%. The efficiency ratio excluding the provision for loan loss was down to 72.41%, which is the lowest second quarter rate since the industry posted 72.36% in mid-year 2012.

Despite gradual improvements to expense management and earnings growth, the 7.6% growth in assets outpaced the 6.9% increase in net income. As such, return on assets remained flat year-over-year at 0.77% as of June 30, 2017.

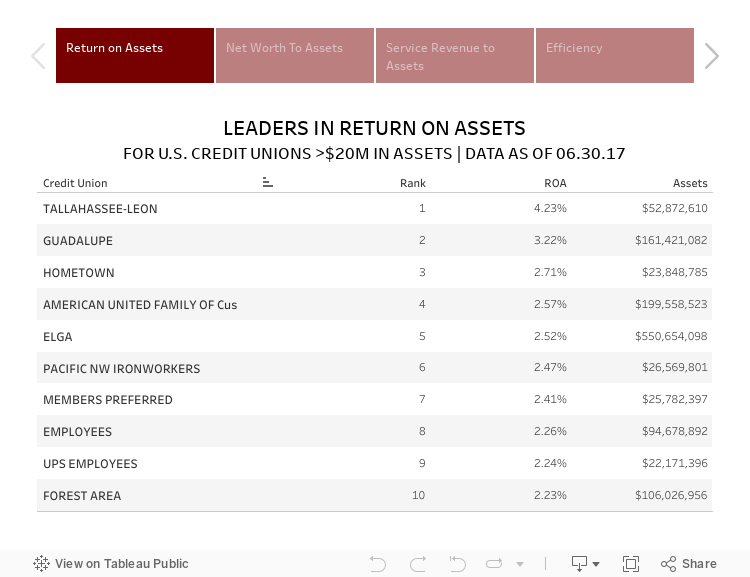

Click through the tabs below to see the top 10 credit unions in each leader table.

var divElement = document.getElementById(‘viz1513978392669’); var vizElement = divElement.getElementsByTagName(‘object’)[0]; vizElement.style.width=’750px’;vizElement.style.height=’577px’; var scriptElement = document.createElement(‘script’); scriptElement.src = ‘https://public.tableau.com/javascripts/api/viz_v1.js’; vizElement.parentNode.insertBefore(scriptElement, vizElement);

See the rest of these tables and explore dozens more along with hundreds of pages of credit union performance data in the 2018 Callahan Credit Union Directory. It’s the gold standard for reliable insight. Read the digital download today.

CASE STUDY

Growing Earnings Through Different Revenue Streams

Purdue FCU | West Lafayette, IN | Assets: $1.1B | Members: 73,065

HopeSouth FCU | Abbeville, SC | Assets: $19.7M | Members: 3,454

KCT Credit Union | Elgin, IL | Assets: $225.8M | Members: 17,697

Purdue Federal Credit Union is using rate swaps and hedging to simultaneously dampen interest rate risk and generate revenue.

Lending continues to dominate the earnings stream accounting for two-thirds of the movement’s income but also important are investment strategies, fee income, and other operating income.

HopeSouth Federal Credit Union has an average loan yield of 10.35% more than twice the national average of 4.51% a result of its commitment to keeping 30% to 35% of its lending in D and E paper.

We can afford to lend to [D and E] members if we price ourselves right, says CEO Faye Crocker.

That approach helped HopeSouth consistently post well-above average ROA, including 2.20% in the second quarter of 2017, nearly three times the national average of 0.77% for all U.S. credit unions.

Credit unions can also generate significant revenue in low-risk investments.

Kane County Teachers Credit Union, for example, generates up to $13,000 a month using the Federal Home Loan Bank’s liquidity and funding services for investment arbitrage.

It’s swinging for the fence that gets credit unions in trouble, KCT CEO Mike Lee says. We’re looking for singles and doubles.

When it comes to fee income, overdraft charges and excessive withdrawal penalties can become overly punitive. But what about non-network ATM fees?

HopeSouth serves a primarily low-income field of membership, and many members come in nearly daily for $20 withdrawals. CEO Crocker says the credit union needs those ATM fees to keep the doors open.

We have three tellers and do 6,000 to 8,000 transactions through our lobby, CEO Crocker says. We have to be there to accommodate that.

Then there’s other operating income: GAP insurance, gains from mortgage sales, loan participations, and debit and credit interchange income.

High penetration equals high interchange income at Purdue Federal Credit Union. The cooperative boasted a second quarter 2017 credit card penetration rate of 50.1%, highest among the nation’s community-chartered credit unions. The average for all credit unions: 17.4%.

The Indiana credit union’s share draft penetration rate of 72.4% also was much higher than the national average of 56.7%. The total result: more than $8 million a year in interchange income.

Read The Whole Story

How Do You Compare?

NCUA and FDIC data is right at your fingertips. Build displays, filter data, track performance, and more with Callahan’s Peer-to-Peer analytics. More insightful performance comparisons start here.

![]()