Financial wellness was my pick for one of the Six Big Ideas for 2016 we’re highlighting here at Callahan & Associates and CreditUnions.com as the New Year begins. I have 16 good reasons why.

Fifteen of those reasons are the 15 credit unions Callahan is working with on a financial wellness initiative through its participation in the Credit Union Financial Services Limited Partnership (CUFSLP).

But the biggest reason is No. 16: Helping working American families achieve financial stability in their lives is the No. 1 way the credit union movement can show it is truly all about people helping people.

This New Year, resolve to create more ways to build financial wellness, stability, and opportunity among the SEGs and communities you serve.

Credit unions have been doing great as an industry. Lending activity has never been higher, both in market share and raw numbers. Membership numbers and total assets have also gone through the roof.

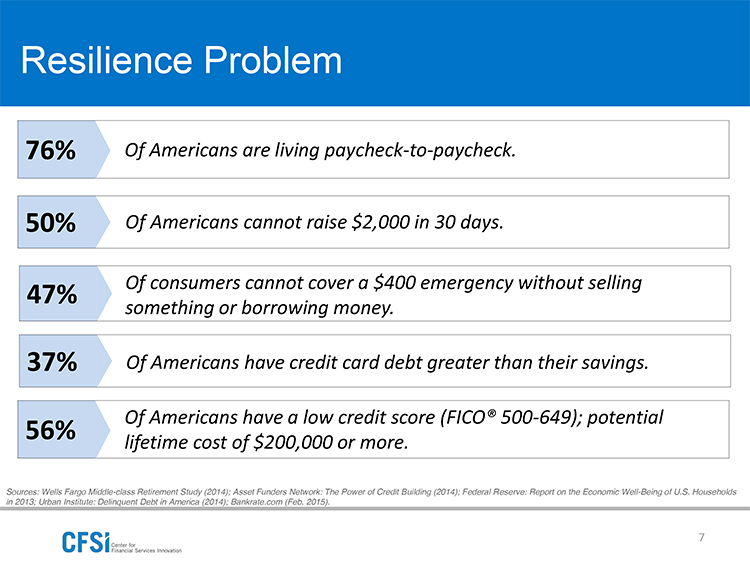

Contrast that with this fact: 47% of Americans cannot cover a $400 emergency expense without selling something or borrowing money, according to the Report on the Economic Well-Being of U.S. Households in 2014by the Federal Reserve. And fully three-fourths of Americans are living paycheck-to-paycheck.

Want To Learn More? Jay Johnson talks about financial wellness in the Callahan & Associates webinar Financial Wellness Is A Big Idea In 2016

There’s more, but you get the idea. Many Americans are living lives of unnerving financial uncertainty, often despite having good jobs with higher-than-average income. That’s where the idea of financial wellness comes in.

The Center for Financial Services Innovation one of CUFSLP’s partners in the financial wellness initiative puts it this way: Financial health comes about when your daily systems help you build resilience and pursue opportunities.

Source: Financial Health In America by CFSI

Financial health is not just about how much money you make, and it’s not just about how financially literate you are. Research and experience has long proven to credit union leaders that financial health is about behavior and a sense of security how you spend your money and how comfortable you are with your ability to take care of yourself and your family.

In other words, it’s about helping members attain a sustainable level of financial wellness. As not-for-profit cooperatives, credit unions alone are positioned to eschew the growth-for-growth’s sake mentality and instead focus on business practices that keep the credit union sound as well as relevant to members for years to come.

Disruption is a buzzword right now, but credit unions have always been disruptive after all, credit unions got their start when people of modest means joined forces to participate in the financial system and gain access to credit, financial stability, and economic opportunity. Credit unions know how to lend. They know how to compete on rates. They know how to be flexible with underwriting to do the most good without taking on undue risk.

Visit the CreditUnions.com Blog Roundup for more Callahan commentary, industry insights, leadership perspectives, and more. Go Now!

The expansion of fields of membership and the flattening of the technology curve means credit unions can provide anything that big banks do and make it available to any American who takes advantage of the credit union difference. Plus, credit unions can do it better and cheaper because they serve member-owners, not investors looking for profit.

That’s so last year, though. So, let’s look ahead.

This New Year, resolve to create more ways to build financial wellness, stability, and opportunity among the SEGs and communities you serve.

There are as many ways to do that as there are credit unions. Our CUFSLP partner CEOs told us their teams were immediately on board with the financial wellness initiative. To date, their own actions to support the initiative include free online and in-person financial assessments and education, sometimes offered alone and sometimes as part of a loan agreement.

Many credit unions are heavily involved in their small-business communities. Others are finding new ways to accommodate the saving and borrowing traditions of ethnic groups among their membership and potential memberships.

These are all great strides forward, but the realities behind the headlines about falling joblessness and booming markets — housing and financial — dictate that credit unions work harder to help our nation move toward greater financial wellness as a people, not just for a business here and a community there.

A rising tide lifts all boats, but someone has to make sure millions don’t get left at the dock as 2016 rolls on.

Please feel free to contact me directly to share your ideas about how to create, and sustain, financial health among your members. I’ll also be happy to put you in touch with the right people at credit unions who might be doing the things you want to adopt or adapt.

Financial Wellness Partners

These credit unions are partners in the CUFSLP financial wellness initiative:

-

Affinity Plus Federal Credit Union ($1.7B, St. Paul, MN)

-

Coastal Federal Credit Union ($2.6B, Raleigh, NC)

-

BECU ($13.9B, Tukwila, WA)

-

Digital Federal Credit Union ($6.5B, Marlborough, MA)

-

Jeanne D’Arc Credit Union ($1.2B, Lowell, MA)

-

Langley Federal Credit Union ($2.0B, Newport News, VA)

-

Patelco Credit Union ($4.6B, Pleasanton, CA)

-

San Antonio Federal Credit Union ($2.8B, San Antonio, TX)

-

SchoolsFirst Federal Credit Union ($11.4B, Santa Ana, CA)

-

Suncoast Credit Union ($6.6B, Tampa, FL)

-

TDECU ($2.7B, Lake Jackson, TX)

-

Teachers Credit Union ($2.8B, South Bend, IN)

-

University Federal Credit Union ($1.9B, Austin, TX)

-

USAlliance Financial ($1.1B, Rye, NY)

-

Wright-Patt Credit Union ($3.1B, Beavercreek, OH)

Financial Wellness Is A Big Idea For 2016

Financial wellness was my pick for one of the Six Big Ideas for 2016 we’re highlighting here at Callahan & Associates and CreditUnions.com as the New Year begins. I have 16 good reasons why.

Fifteen of those reasons are the 15 credit unions Callahan is working with on a financial wellness initiative through its participation in the Credit Union Financial Services Limited Partnership (CUFSLP).

But the biggest reason is No. 16: Helping working American families achieve financial stability in their lives is the No. 1 way the credit union movement can show it is truly all about people helping people.

This New Year, resolve to create more ways to build financial wellness, stability, and opportunity among the SEGs and communities you serve.

Credit unions have been doing great as an industry. Lending activity has never been higher, both in market share and raw numbers. Membership numbers and total assets have also gone through the roof.

Contrast that with this fact: 47% of Americans cannot cover a $400 emergency expense without selling something or borrowing money, according to the Report on the Economic Well-Being of U.S. Households in 2014by the Federal Reserve. And fully three-fourths of Americans are living paycheck-to-paycheck.

Want To Learn More? Jay Johnson talks about financial wellness in the Callahan & Associates webinar Financial Wellness Is A Big Idea In 2016

There’s more, but you get the idea. Many Americans are living lives of unnerving financial uncertainty, often despite having good jobs with higher-than-average income. That’s where the idea of financial wellness comes in.

The Center for Financial Services Innovation one of CUFSLP’s partners in the financial wellness initiative puts it this way: Financial health comes about when your daily systems help you build resilience and pursue opportunities.

Source: Financial Health In America by CFSI

Financial health is not just about how much money you make, and it’s not just about how financially literate you are. Research and experience has long proven to credit union leaders that financial health is about behavior and a sense of security how you spend your money and how comfortable you are with your ability to take care of yourself and your family.

In other words, it’s about helping members attain a sustainable level of financial wellness. As not-for-profit cooperatives, credit unions alone are positioned to eschew the growth-for-growth’s sake mentality and instead focus on business practices that keep the credit union sound as well as relevant to members for years to come.

Disruption is a buzzword right now, but credit unions have always been disruptive after all, credit unions got their start when people of modest means joined forces to participate in the financial system and gain access to credit, financial stability, and economic opportunity. Credit unions know how to lend. They know how to compete on rates. They know how to be flexible with underwriting to do the most good without taking on undue risk.

Visit the CreditUnions.com Blog Roundup for more Callahan commentary, industry insights, leadership perspectives, and more. Go Now!

The expansion of fields of membership and the flattening of the technology curve means credit unions can provide anything that big banks do and make it available to any American who takes advantage of the credit union difference. Plus, credit unions can do it better and cheaper because they serve member-owners, not investors looking for profit.

That’s so last year, though. So, let’s look ahead.

This New Year, resolve to create more ways to build financial wellness, stability, and opportunity among the SEGs and communities you serve.

There are as many ways to do that as there are credit unions. Our CUFSLP partner CEOs told us their teams were immediately on board with the financial wellness initiative. To date, their own actions to support the initiative include free online and in-person financial assessments and education, sometimes offered alone and sometimes as part of a loan agreement.

Many credit unions are heavily involved in their small-business communities. Others are finding new ways to accommodate the saving and borrowing traditions of ethnic groups among their membership and potential memberships.

These are all great strides forward, but the realities behind the headlines about falling joblessness and booming markets — housing and financial — dictate that credit unions work harder to help our nation move toward greater financial wellness as a people, not just for a business here and a community there.

A rising tide lifts all boats, but someone has to make sure millions don’t get left at the dock as 2016 rolls on.

Please feel free to contact me directly to share your ideas about how to create, and sustain, financial health among your members. I’ll also be happy to put you in touch with the right people at credit unions who might be doing the things you want to adopt or adapt.

Financial Wellness Partners

These credit unions are partners in the CUFSLP financial wellness initiative:

Affinity Plus Federal Credit Union ($1.7B, St. Paul, MN)

Coastal Federal Credit Union ($2.6B, Raleigh, NC)

BECU ($13.9B, Tukwila, WA)

Digital Federal Credit Union ($6.5B, Marlborough, MA)

Jeanne D’Arc Credit Union ($1.2B, Lowell, MA)

Langley Federal Credit Union ($2.0B, Newport News, VA)

Patelco Credit Union ($4.6B, Pleasanton, CA)

San Antonio Federal Credit Union ($2.8B, San Antonio, TX)

SchoolsFirst Federal Credit Union ($11.4B, Santa Ana, CA)

Suncoast Credit Union ($6.6B, Tampa, FL)

TDECU ($2.7B, Lake Jackson, TX)

Teachers Credit Union ($2.8B, South Bend, IN)

University Federal Credit Union ($1.9B, Austin, TX)

USAlliance Financial ($1.1B, Rye, NY)

Wright-Patt Credit Union ($3.1B, Beavercreek, OH)

Daily Dose Of Industry Insights

Stay informed, inspired, and connected with the latest trends and best practices in the credit union industry by subscribing to the free CreditUnions.com newsletter.

Share this Post

Latest Articles

Competing For Gen Z, SMBs, And The Future Of Money

The Financial Readiness Gap: Credit Unions Evaluate It Every Day. But Who Builds It?

Defending Your Credit Union Against Fraud Means Fighting Fire With Smarter Fire

Keep Reading

Related Posts

Connection And Caring Matter As Much As Knowledge And Resources

Markets Flip From Pricing Cuts To 50% Chance Of Hikes

New Highs For Equity Markets Despite Iran And Oil Prices

Competing For Gen Z, SMBs, And The Future Of Money

The Financial Readiness Gap: Credit Unions Evaluate It Every Day. But Who Builds It?

The Long Game For Fintech At FORUM Credit Union

Marc RapportView all posts in:

More on: