Credit unions require skilled managers and consistent management. Executives manage everything from branch profitability to interest rate risk, and a variety of factors can cause financial and operational challenges to arise.

In today’s changing economic environment, balance sheet management specifically, liquidity management is top-of-mind with credit union executives as they push and pull a number of levers to make the most of their monies.

Here are three popular ways for credit unions to manage liquidity.

1. Pricing Strategies

To maximize member value, credit unions must provide competitively priced savings and loan products. A credit union’s ability to provide the latter is largely dependent upon its ability to attract members through the former.

Traditionally, credit unions have strengthened their balance sheet by increasing share balances and distributing those funds in the form of loans. All things being equal, a credit union can use its members’ share balances to make loans. Even becoming loaned out, the term applied when loan balances equal share balances, has not stopped some prolific lending shops.

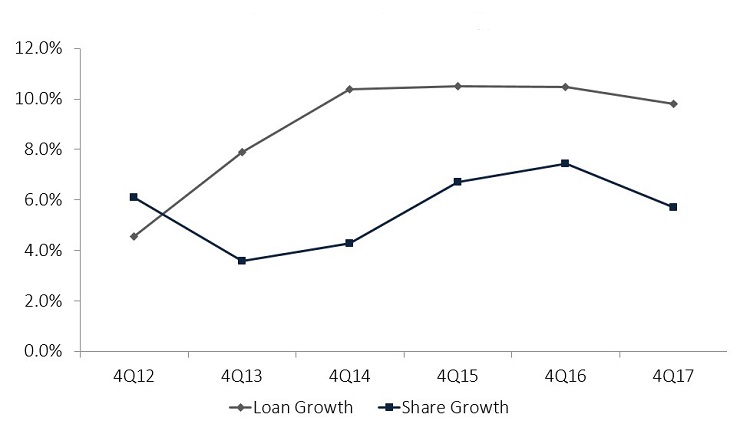

Loan growth and share growth have an inverse relationship. In times of economic prosperity, consumers demand more or larger loans. During periods of economic contraction, consumers seek safe havens for their savings.

LOAN GROWTH VS SHARE GROWTH

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.17

Source: Peer-to-Peer Analytics by Callahan & Associates.

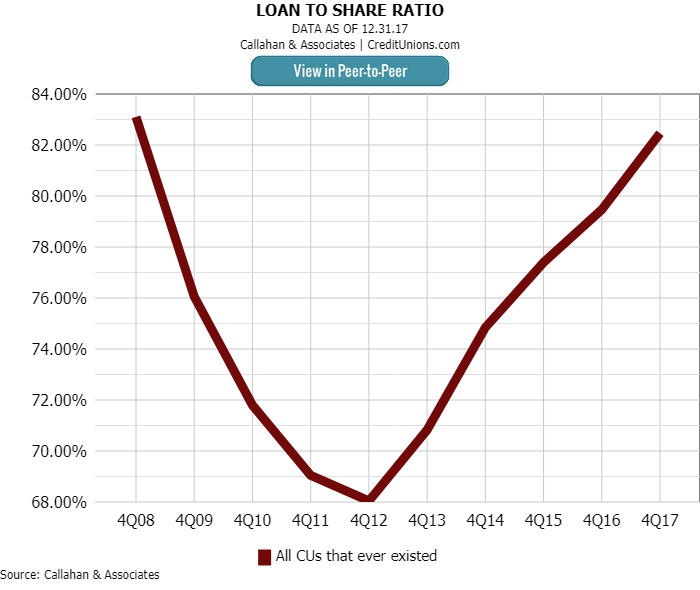

During the Great Recession, the average credit union loan-to-share ratio peaked in December 2008 at 83.1%. In the difficult quarters and years to follow, it steadily declined until hitting a low of 68.0% in December 2012. Since then, the loan-to-share ratio has steadily risen and reached 82.5% as of December 2017. That’s only 60 basis points below the 2008 high.

Over the period of decline, financial institutions generally tightened their underwriting standards and pulled back their appetite for risk across nearly every lending category. This greatly reduced consumer access to credit. However, the increasing loan-to-share ratio over the past five years indicates the economy has been growing.

Although higher loan-to-share ratios are generally indicative of a stronger economy, rising loan-to-share ratios present a dilemma for credit union executives.

On the one hand, a growing loan portfolio is proof-positive of the credit union’s success in satisfying loan demand; however, at times it can be at the expense of deposit growth.

There are several options available to a credit union faced with a steadily growing loan-to-share-ratio. One of the easiest strategies is to spur deposit growth. Credit unions do this typically in the form of limited-duration savings specials, e.g., a 2% special on a three-month share certificate.

If a targeted deposit growth strategy alone does not ease the upward pressure, a credit union can also slow loan growth by limiting marketing and promotion activities or becoming more selective in its underwriting.

2. Sales To The Secondary Market

For credit unions that do not want to limit lending, there are other options to manage liquidity.

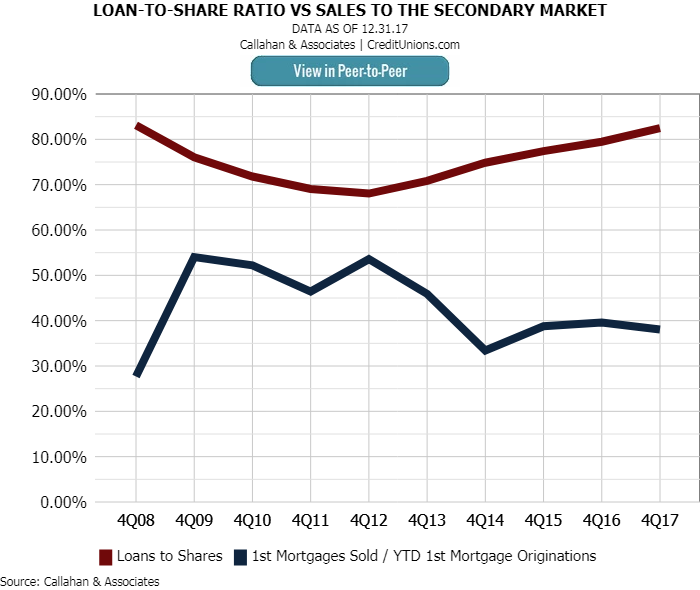

For example, fixed rate first mortgage loans have both the largest capital requirement and longest average duration on a per loan basis of any product in the portfolio of most credit unions. Because of these requirements, 38.0% of credit unions that originated a first mortgage loan as of the fourth quarter of 2017 also sold them.

The most popular avenue to sell first mortgage loans is to the secondary market. The primary parties that purchase loans on the secondary market are government-sponsored enterprises including Fannie Mae, Freddie Mac, Ginnie Mae, and Federal Home Loan Banks other government affiliates such as the Federal Housing Administration (FHA) and the Department of Veterans Affairs (VA), and to a lesser extent other financial institutions and insurance companies.

For lenders that want to serve their members but are wary of adding loans to their balance sheets, the secondary market can be an attractive option. From a directional perspective, sales to the secondary market as a percentage of first mortgage originations will generally lag behind a rising or falling loan-to-share ratio.

For example, in the quarters leading up to December 2008, sales as a percentage of originations hovered around a historically low level of 27.7%. This incrementally ticked up as credit unions sought to make loans while selling a majority of their first mortgage originations 54.0% in December 2009.

Mortgage sales continued to climb, contributing to the December 2012 loan-to-share ratio low.

As the chart above shows, when consumer confidence rebounded in 2013, credit unions had ample capital available for lending. Consequently, the loan-to-share ratio for the credit union industry began to increase while sales of mortgages as a percentage of originations declined.

Learn More With Media Suite

Like what you’re reading? Gain greater access to the content available on CreditUnions.com with a Callahan Media Suite subscription. Learn more today.

![]()

3. Loan Participation Sales

Selling loans to the secondary market can be an effective way to manage the liquidity and interest rate risk of a credit union’s first mortgage portfolio. So, too, is selling loan participations to other financial institutions.

The end result of selling loan participations is similar in principal to selling first mortgage loans to the secondary market. However, loan participations are not limited by loan type. In fact, credit unions can sell real estate, member business loans, and consumer loans alike.

The broader industry dynamics associated with secondary market sales holds true for sales of participation loans. When loan growth consistently outpaces share growth, there is an incremental increase in sales of participation loans. As credit unions seek to free up capital, they convert assets into liabilities they can redeploy to areas that better fit their operational goals for the given economic environment. For example, in times of economic growth, credit unions might find it advantageous to sell less-profitable portions of their portfolio and increase their activities in higher-yielding areas.

ContentMiddleAd

Looking ahead, liquidity management will continue to be a necessary practice for executives to properly guide their credit union. Regardless of the financial climate during economic expansion and contraction alike different liquidity management strategies exist to help credit unions better position themselves.