A large shift continued in the third quarter as loan growth tripled share growth, a complete reversal from the environment in 2020 and 2021. Changes in the economy, namely interest rates, were primary drivers of changes to credit union strategies. Although historically strong, asset quality is under close scrutiny as credit unions prepare for economic factors to impact their members’ ability to repay their loans. Unemployment finished the third quarter near historic lows, and wages and salaries continue to rise across the United State, but consumers and businesses are bracing for tougher times ahead.

Callahan’s quarterly Trendwatch webinar covered these topics and more, highlighting key trends in the credit union industry and economy. Read on for five takeaways from the webinar.

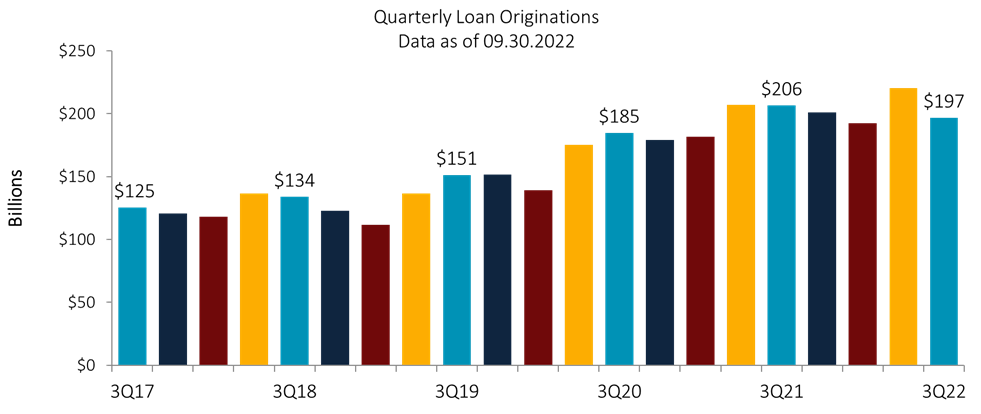

No.1: Quarterly Loan Originations Are Down

Quarterly Loan Originations

FOR U.S. CREDIT UNIONS | DATA AS OF 09.30.22

© Callahan & Associates | CreditUnions.com

- High asset prices kept the dollar amount of originations elevated despite falling on an annual basis.

- Coming off a prosperous second quarter, originations totaled $196.8 billion in the third quarter, down 10.8% quarter-over-quarter.

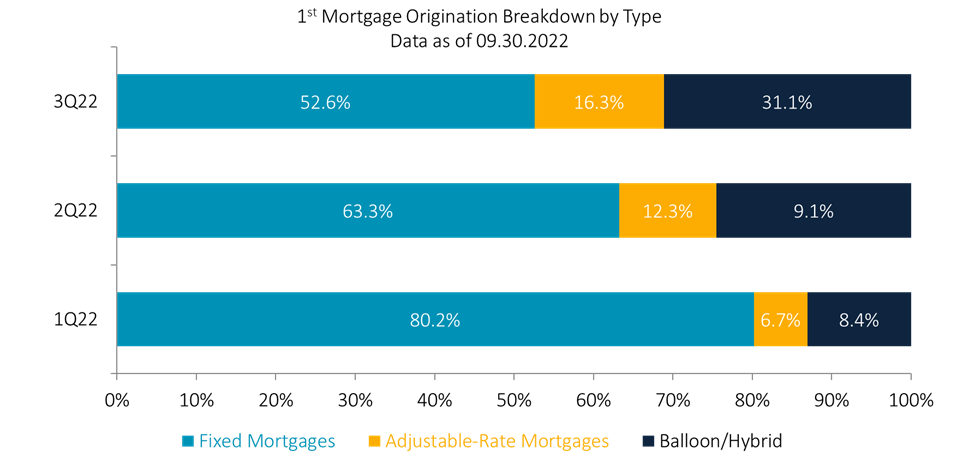

No. 2: Fixed Rate Mortgages Are Losing Ground

First Mortgage Originations By Type

FOR U.S. CREDIT UNIONS | DATA AS OF 09.30.22

© Callahan & Associates | CreditUnions.com

-

- High home prices and rising rates have priced some members out of fixed rate mortgages, turning them to ARMs instead. Fixed rate mortgages comprise 27.6 percentage points less of the first mortgage portfolio than at the start of 2022.

- The national average 30-year mortgage rate was 7.3% as of Nov. 7, up 400 basis points over the past year.

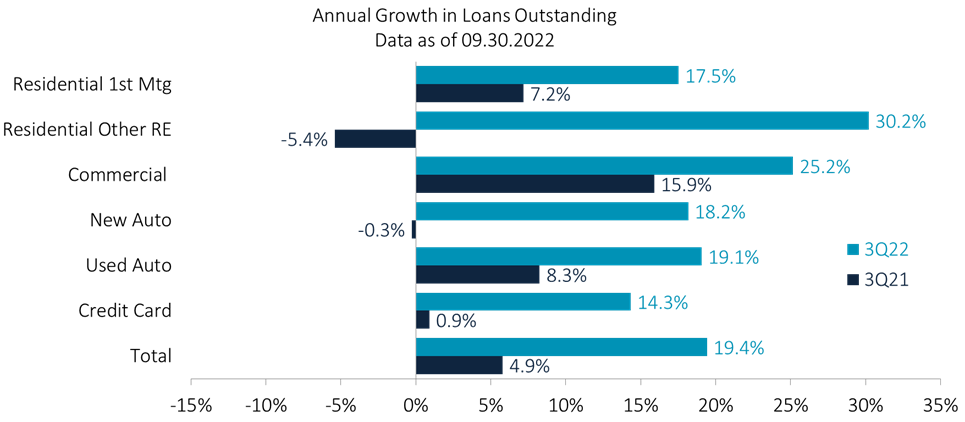

No. 3: Balances Are Up Across All Loan Categories

Annual Growth in Loans Outstanding

FOR U.S. CREDIT UNIONS | DATA AS OF 09.30.22

© Callahan & Associates | CreditUnions.com

- Across the board, balances in all major loan types grew by double-digits year-over-year, leading to a record quarter for lending. Total loan balances increased 19.4% year-over-year.

- New auto loan balances were up 18.2% after a tough year for the auto industry in 2021. Supply challenges seem to be resolving, and credit unions are making up for the lack of lending in the auto space during the pandemic.

- HELOCs guided the residential other real estate category to 30.2% annual growth.

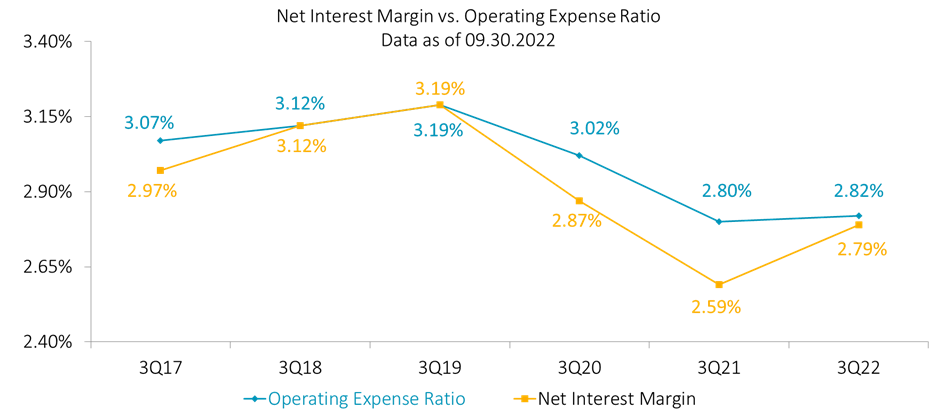

No. 4: Key Ratios Are Nearly Even

Net Interest Margin vs. Operating Expense Ratio

FOR U.S. CREDIT UNIONS | DATA AS OF 09.30.22

© Callahan & Associates | CreditUnions.com

- The spread between the operating expense ratio and the net interest margin (NIM) narrowed to 3 basis points in the third quarter, meaning credit unions are almost covering their operating expenses with the NIM. Higher interest earned on loans and investments, and lower interest paid on deposits, improved the NIM.

- The operating expense ratio increased to 2.82% after two years of declines when expense growth lagged behind asset growth.

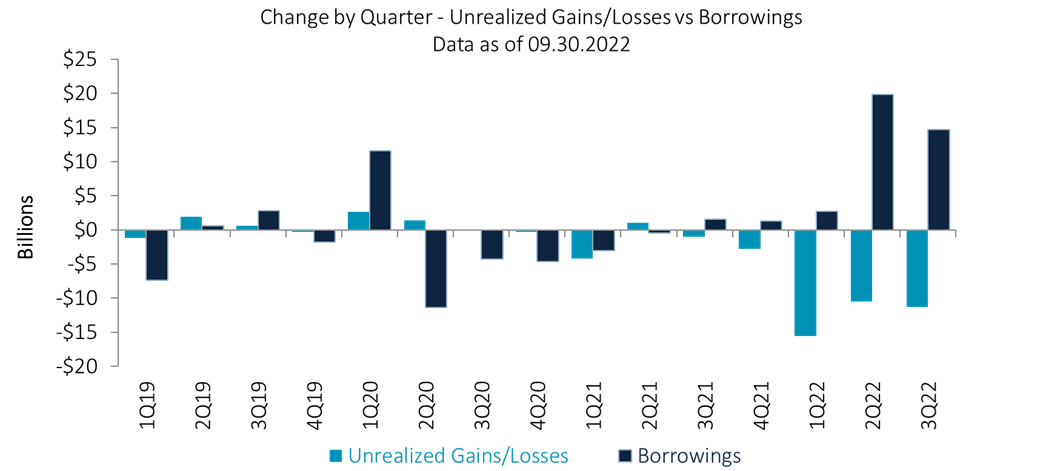

No. 5: Securities Losses Continue

Change by Quarter – Unrealized Gains/Losses vs. Borrowings

FOR U.S. CREDIT UNIONS | DATA AS OF 09.30.22

© Callahan & Associates | CreditUnions.com

- Unrealized losses swelled to $39.6 billion year-to-date and won’t rescind until securities mature or market conditions improve.

- Credit unions have avoided realizing these losses by choosing to fund loans with cash balances, which might cause liquidity issues for some credit unions if fixed income performance doesn’t improve.