Concentrating on making home loans to its first-responder members has helped Long Beach Firemen’s Credit Union ($183.2M, Long Beach, CA) stand out among its peers in several measures of member engagement, including the key metric of average member relationship.

Adding up all the shares and loan total among the 3,236 members at LBFCU yielded an average member relationship of $76,652, compared with $18,002 for all the 2,773 credit unions of all sizes that have reported first quarter data so far this year.

Helping to drive that performance is a huge emphasis on mortgage lending. LBFCU has been averaging about 15% in first-mortgage penetration among its membership since at least 1998, when Callahan & Associates first started reporting those figures.

About 98% of its loan portfolio is in mortgages, compared with 40.4% for the national average. And its average loan balance is $94,308, compared with $21,246 for all California credit unions and $11,685 for LBFCU’s asset-based peer group reporting so far in 1Q2017.

Another contributing factor to this high number is the relatively high home prices in Long Beach. According to Trulia, the median selling price in the area is $485,000,whereas the national median is $315,100 (according to the U.S. Census).

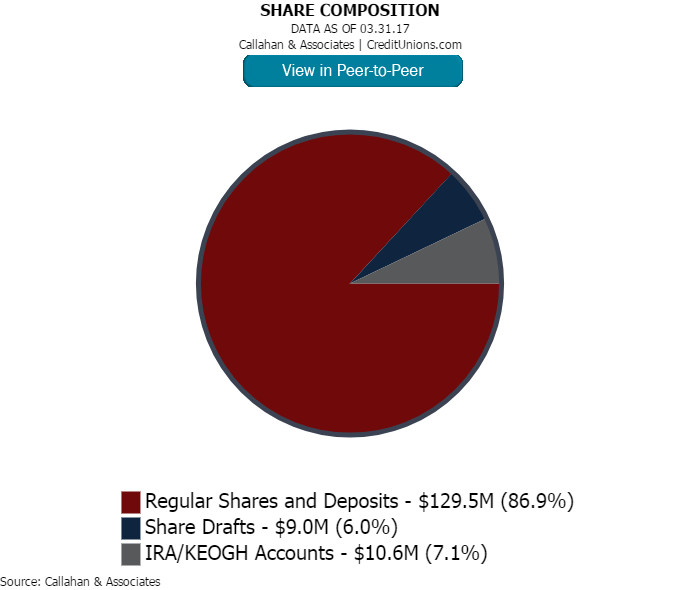

A second major metric of the average member relationship numerator is the dollar amount of total shares. LBFCU has 86.9% of its share portfolio in regular shares and only 6.0% in share drafts. Nationally, the average credit union has only 38.7% regularshares and 15.1% share drafts as of 1Q 2017. Although less diverse than national peers, LBFCU has strong core deposits and has seen total shares grow by 4.4% over the past year.

The credit union also has a strong efficiency ratio, 37.03% compared with 82.01% for its asset class average, and it averages $2.5 million in annual loan originations per FTE, compared with $893,114 for its asset class and $1.5 million for the averageof all reporting credit unions in 1Q2017.

LBFCU’s ROA is also quite healthy, 1.27% at the end of the first quarter of 2017. LBFCU’s business model shows that a smaller credit union can compete for home loans among a loyal membership in a closely knit SEG, and that it’s a businessmodel that can be sustained over time.