Supplemental Capital Is No Panacea

Supplemental capital is a useful tool that is long overdue; however, it is not without risk and potential complications.

Look beyond the headlines to better understand what is driving current market trends and how they could impact credit union investment portfolios.

A rethink of closing costs, rate relief, and employer partnerships helped 7 17 Credit Union build an affordable housing mortgage program that works.

Where is mortgage growth coming from right now? This week, CreditUnions.com covers a mix of home equity campaigns, targeted affordability programs, and niche lending strategies that are bringing borrowers back into the market.

Home equity lending is a winning option for credit unions in today’s mortgage environment. Learn how three different shops meet members’ needs.

Manufactured home loans can provide members access to affordable housing, including those in rural areas. Two credit unions share how they approach the niche product.

After a prolonged slowdown, signs of life are returning to mortgage lending. Growth is uneven, with first-time buyers and shifting rate dynamics driving activity in select segments.

The Michigan cooperative keeps everyday payments working and members happy by using a common friction point to build brand loyalty.

How a former Sam’s Club finance leader adapted his member-first mindset to a not-for-profit credit union.

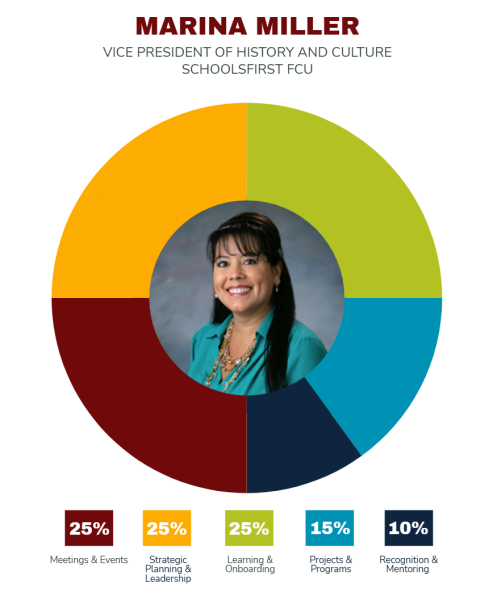

How a novel role instills SchoolsFirst FCU’s future leaders with an appreciation for its past.

Arriba Advisors co-founder Tom Russell explores how credit unions can bridge the gap between a growth mindset and their technical reality.

Supplemental Capital Is No Panacea