Top-Level Takeaways

-

Greenwood operates as a full-service credit union for members that live within five miles of the cooperative’s lone branch.

-

It also serves members from all corners of the country that have loan-only relationships.

Greenwood Credit Union($657.4M, Warwick, RI) is a mid-size credit union headquartered not from T.F. Green airport, the largest airport in the small state. The creditunion’s name comes from the neighborhood from which it has been operated for more than 75 years, in that time supporting the needs of a core group of members with its traditional banking services.

But that’s just the half of it.

Greenwood is a state-chartered, federally insured credit union with a single branch but a nationwide charter that allows it to do business across the United States, says CEO Fred Reinhardt.

Fred Reinhardt, CEO, Greenwood Credit Union

We see ourselves having two distinct purposes,Reinhardt says.

First, it wants to help its core members those who live in a five-mile radius around its lone branch achieve their long-term financial objectives. But Greenwood is also an active indirect auto lender and works with correspondent lendersof manufactured homes to add mortgages to its books.

We think this is an important role we can take in the financial services industry,the CEO says.

A Core Member

Checking account penetration at Greenwood shows a clear divide between core members and others. Its checking penetration in the second quarter of 2021 was 10.0%, which lagged state peers by nearly 35 percentage points and asset-based and nationwide peers by even more.

CU QUICK FACTS

Greenwood Credit Union

Data as of 06.30.21

HQ:Warwick,RI

ASSETS:$657.4M

MEMBERS:79,054

BRANCHES:1

12-MO SHARE GROWTH:5.6%

12-MO LOAN GROWTH:5.5%

ROA: 1.19%

But that number by itself is misleading, Reinhardt says. In his experience, most consumers maintain checking accounts with the bank or credit union near where they live or work. Combine that preference to the already difficult challenge of deepening wallet share among indirect members and it explains why Greenwood is happy to maintain a loan-only relationship with a segment of its membership.

Most people have a checking account with an institution that is close to them,Reinhardt says.If we have a member that lives in South Carolina, he or she is not going to have a checking account with us in Rhode Island.

On the other hand, more than 55% of members who live within five miles of the credit union have a checking account with Greenwood, Reinhardt says. For those core members, Greenwood offers, on average, a higher interest rate on checking accounts than asset-based and state peers 0.15% compared to 0.10% and 0.05%, respectively. Additionally, Greenwood ranks second among asset-based peers in total dividends paid, and its dividends/income ratio, 24.7%, far outpaces the 8.0% at those same peer credit unions.

But the majority of the credit union’s members join Greenwood through its lending channels. And there’s a strategy behind that,too.

Lender Partners

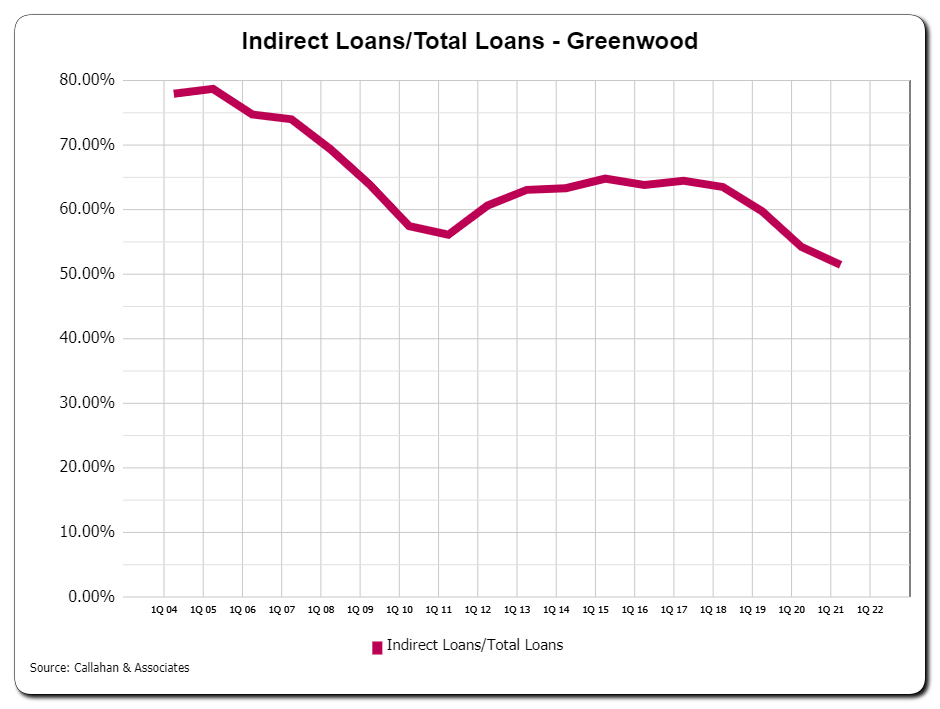

When Reinhardt joined the credit union as CEO in 2016, he inherited an organization that had originated at least half of its loans from indirect channels since 2004,when Callahan’s indirect lending data begins.

INDIRECT LOANS/TOTAL LOANS

FOR GREENWOOD CREDIT UNIONS | DATA AS OF 06.30.21

In the past three years, Greenwood’s indirect loans to total loans has decreased by 12 percentage points, to 51.5% as of second quarter 2021. That’s still more than double state, asset, and national peer average.

Greenwood had developed hundreds of relationships with auto dealers and does business with some 300 dealer partners across the northeast and as far as Wisconsin and Iowa, Reinhardt says. And although the percentage of indirect loans on its books continues to decline, it remains a primary channel of focus.

We continue to refine our strategy to be as effective, profitable, and efficient as possible,the CEO says.

But in a crowded market, it’s not always easy to stand out.

To do so, Greenwood aims to be as efficient and responsible as possible, investing in technology, like automated decisioning software and other digital tools, to make the application process quicky and easy. In fact, its investments in technology stemfrom a long-term strategy to maintain a single branch, despite asset-based peers managing nine on average.

We made the determination that technology and digital channels would replace the need for more branches,Reinhardt says.We’ve continued to operate with a focus to meet the member digitally as best we can.

In addition, Greenwood does not make loan decisions based on credit score alone, an ethos the CEO believes gives it an edge against other lenders when faced with more challenging applications. Rather than focus solely on FICO, Greenwood’s underwritersfocus on the ability to repay, keying in on income, time in current job, and additional debts, among other items.

Akin to its indirect auto strategy, Greenwood works with a smaller, select number of correspondent lenders that originate manufactured homes across the country. Greenwood underwrites the originated loan itself before paying the originator a fee and portfolioing the loan. In some states, manufactured homes are treated as traditional mortgages whereas in others they are considered chattel, but, in the end, they are interest-earning loans on the credit union’s books that provide homeownership opportunity to the borrowers and help Greenwood’s lending partners achieve their own goals.

Ultimately, Greenwood’s strategy is loan-based, but that doesn’t mean it isn’t driven by core values. It wants to help its core members grow financially and its partner dealers and lenders extend capital to those who need loans. Andif that sounds different, that’s the point.

Our employees embrace our core values every day they come to work, whether they are working with a core member or one of our partners,Reinhardt says.That helps differentiate us against all the competition out there.