When Suzie Kisslan joined Credit Union of Southern California ($1.2B, Whittier, CA) from Altura Credit Union ($1.2B, Riverside, CA) in July 2016, the new chief lending officer inherited a decentralized loan operation spread across 19 branches.

While at Altura, Kisslan had implemented a lending system wherein branches sent applications to a centralized underwriting division responsible for approving loans. After an approval, branches set appointments, drew documents, and had members sign documents, Kisslan says.

CU SoCal tasked her with doing the same.

CU QUICK FACTS

Credit Union of Southern California

Data as of 12.31.16

HQ:Whittier, CA

ASSETS: $1.2B

MEMBERS:92,119

BRANCHES: 19

12-MO SHARE GROWTH: 18.9%

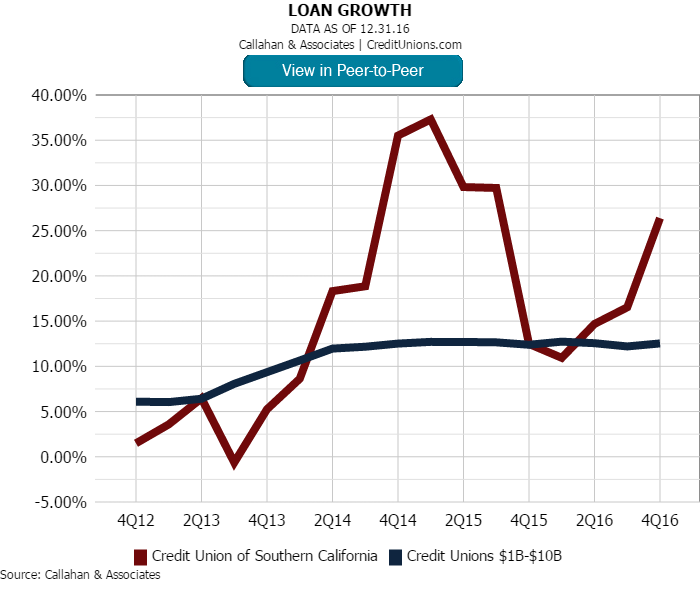

12-MO LOAN GROWTH:26.4%

ROA:1.25%

In this QA, Kisslan discusses the benefits of shifting to a centralized environment, what greater automation means for the consumer loan process, and how she built a team from the credit union’s best of the best.

Why did CU SoCal move to a centralized lending environment?

Suzie Kisslan: Because of inefficiencies as well as overall branch focus. Our focus for branches is to open accounts and get new members. Loans were sort of an afterthought. Plus, the branches didn’t have the expertise or structure that lent itself to loan processing efficiencies.

What were the first changes you made?

SK: We started with the inefficiencies in the details and the sophistication of the policies and procedures. There were vanilla, conservative guidelines and procedures in place. To my eyes, it was like the credit union didn’t want to make loans.

So, my first task was to evaluate the policies and procedures to identify areas where we could make more loans in a more efficient manner without requiring the borrower to give blood.

How did you make policies and procedures less conservative?

SK: From a policy standpoint, the biggest change was the implementation of a six-tier risk-based pricing model. This allowed us to look at members differently and appropriately price based on FICO score for the risk we would take. We also implemented DocuSign, so now we can fund loans without members needing to come into the branch.

We also required too many different steps. We required proof of income on every borrower whether it was an A borrower or a D borrower, we needed to see the vehicle before we funded the auto loan, we needed to verify employment over the phone. Things that made it too cumbersome to get a consumer loan we weren’t as competitive as other credit unions or banks.

My first task was to evaluate the policies and procedures to identify areas where we could make more loans in a more efficient manner without requiring the borrower to give blood.

Did you do anything in regards to technology?

SK: We were using a platform called Meridian Link for our loan origination system, which feeds into our core data processor. But we weren’t using that system the way we could, and should, to improve efficiency. So, we worked with Meridian Link in person and on webinars to see how we could implement some of the system enhancements the company already offered, like instant approvals.

How did you build your team?

SK: When I joined the credit union, we had a team of eight. I was given the opportunity to build my entire team from underwriters, back-office processors, and loan sales. Now we have 17 total.

I looked for a specific talent and skillset for each area, and, along with other managers, I choose from anyone in the entire organization, the best of the best here at CU SoCal. They could have been in our call center, back office, front office it didn’t matter. After we did that we still had four or five openings, so we went outside the organization and brought in some talent that way as well.

Click the tabs below for a deeper dive into CU SoCal’s financial performance. Click on the graphs to open Peer-to-Peer and add your credit union for comparison.

1. Loan Growth

2. New Used Auto Loan Balances

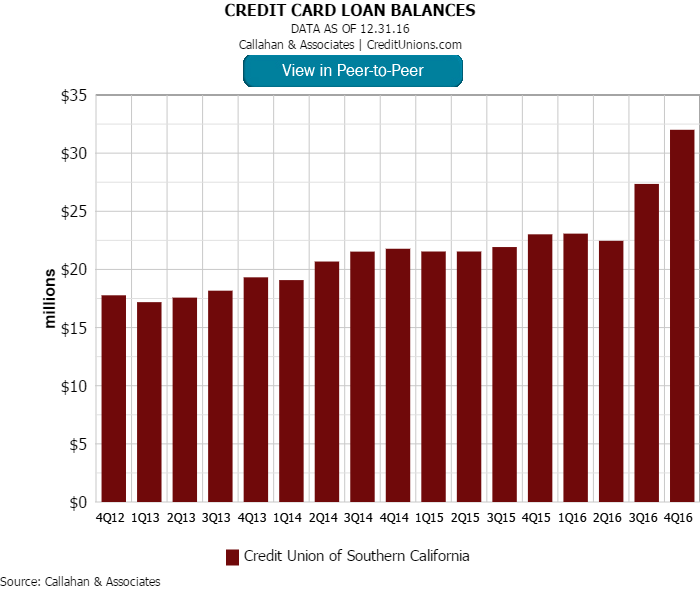

3. Credit Card Loan Balances

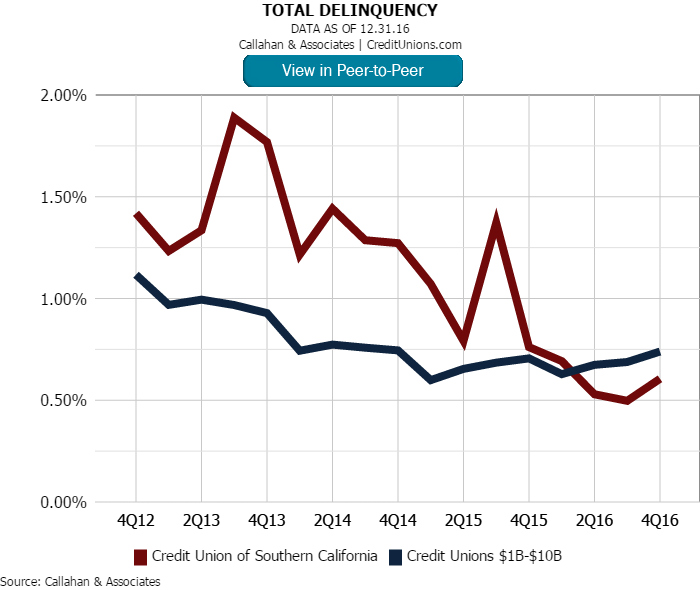

4. Total Delinquency

You mention skillsets. What were you looking for specifically?

SK: For back-office processing, I was looking for someone who was detail oriented, organized, quick, and efficient. And I always look for individuals who aren’t afraid to question why do certain processes certain ways.

On the sales side, I looked for individuals who loved sales and could educate members on our products and services. They also had to be able to overcome objections that our members might have and convincing as to why the services and products we offer are better than what they can get somewhere else.

For underwriters, I was looking for experience. And all our underwriters are internal hires.

The credit union has had success selling ancillary products like insurance and debt protection. Why?

SK: The credit union already offered GAP, mechanical recovery care, and debt protection coverage. But we’ve tripled GAP product sales from 175 to 200 a month since we instituted centralized lending and improved our policies and procedures. We’ve doubled mechanical recovery sales as well. The one area with which we are struggling is debt protection.

How Do You Compare?

Check out Credit Union of Southern California’s performance profile. Then build your own peer group and browse performance reports for more insightful comparisons.

Why is that?

SK: It has a lot to do with comfort and the knowledge of what the product offers. We have a young sales team, and I don’t think they see the value in the coverage so they’re struggling with finding stories and sharing why it will help the borrower. So, we’re offering more education about the features and the benefits of the product.

What are the results of moving to centralized lending? What are the credit union’s future goals?

SK: In first quarter, before I started, the credit union averaged $4.6 million in consumer loans per month. Centralizing lending allowed us to see an immediate impact on volume. We booked $9.1 million in October 2016, $10.6 million in November, and $13.4 million in December. (Editor’s Note: In 2016, CU SoCal also merged four credit unions for a total of $110 million in assets).

My goal is by first quarter 2018 we will be at $20 million a month in consumer loans.

We’ve got the right people in place now, so we need to make sure we can handle the volume we need to continue to grow. And the way to do that without throwing bodies at that goal is to continue to streamline our processes.

This interview has been edited and condensed.