When it comes to improving an efficiency ratio, a metric that reveals how much money a credit union spends to earn one dollar of revenue,there are really just two ways an institutiin can go. It can cut costs, which can affect service quality, or it can increase revenue. That’s the path Maroon Financial Credit Union ($40M,Chicago, IL) chose.

After the financial crisis, the credit union faced a tenuous economic climate. Institutions around the country cut expenses drastically to improve their balance sheets, and many smallercredit unions that couldn’t survive independently merged with larger institutions. Maroon Financial, though, invested in itself, increased its mortgage originations, and eventually grew its assets. Today, Maroon Financial has an efficiency ratio of 75.47%, which is down a staggering 24 percentage points in just 12 months from 99.33% at year-end 2011.

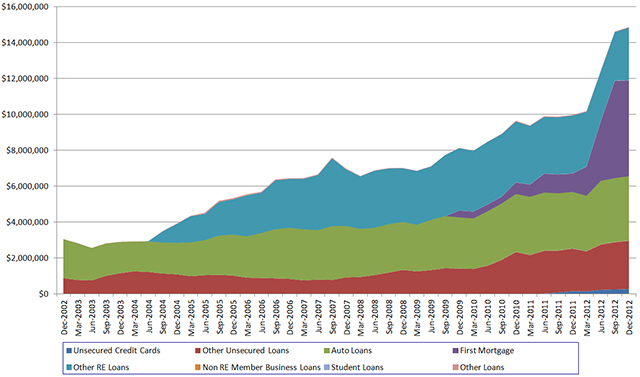

LOAN COMPOSITION MAROON FINANCIAL

DATA AS OF DECEMBER 31, 2012 | www.creditunions.com

Generated by Callahan & Associates’Peer-to-Peer Software.

After the credit crisis, we realized we couldn’t survive by cutting costs, says Cristian Hernandez, CEO of Maroon Financial, which has only one branch and 12 employees. There really weren’t many places to cut. But increasingour size created economies of scale that allowed us to offer new and better products and more efficiently structure offerings to our members.

A Difficult Decision

In hindsight that decision might seem like a no-brainer, but in 2008 Maroon Financial was a $15 million institution, nearly two-thirds smaller than it is today. It couldn’t afford to make any mistakes, but the alternative to investment was grim. Watching from the sidelines, Hernandez could see what was happening to other small players in the market.

Many were going to end up having to merge, and we didn’t want that to be our fate, he says. We needed to make sure our franchise was as strong as ever.

In one respect, the credit union had an advantage. Maroon Financial is a single-sponsor credit union serving about 5,600 members at the University of Chicago Medical Center. That relationship bought the credit union some time so that it could pursue its strategy for growth.

We were shielded from a lot in 2007 and 2008 because our sponsor is pretty strong and economically stable, Hernandez says. Had it been a steel mill or a manufacturing company, we would have been in trouble.

Byinvesting in its infrastructure, products, services, and people, Maroon Financial hoped to be in a stronger position to expand when the economy recovered. Because mortgage origination was Maroon Financial’s main revenue source, that was the obvious place to invest. Plus, it was logical to assume that one employee could handle $400,000 in loans just as easily as $100,000.

INCOME COMPOSITION

DATA AS OF DECEMBER 31, 2012 | www.creditunions.com

Generated by Callahan & Associates’Peer-to-Peer Software.

In the past, Maroon Financial had acted as a broker for several mortgage wholesalers in the country. The mortgage originations brought in good income about 1 percentage point per loan but the credit union’s leadership saw several weaknesses in the mortgage arena. Once the loan was originated, for instance, the credit union lost control of the member relationship because the usual servicer of those mortgages was almost always a big bank, which then would target Maroon Financial’s own members for new products and services.

We realized that in order to better compete we had to service our own mortgage loans even if we were to sell them, Hernandez says. We became members of the Federal Home Loan Bank of Chicago. The relationship allowed us to retain complete control of the transaction for the life of the loan without carrying the interest rate risk associated with a mortgage loan.

Staying The Course

But the strategy was not a quick fix. It took the credit union nearly three years to see any benefits and rewards. Between 2008 and 2011 there were more questions than answers. Is this the right strategy? Do we need to grow this fast? Should we have takena more drastic cost-cutting measure? In 2010 the credit union barely broke even, and in 2011 it took a loss. Times were tough.

To weather the storm, communication was key, if only for the board and management to prepare the staff for an essential salary freeze in 2011.

We explained it’s temporary and eventually we’re all going to reap the rewards of work well done, Hernandez says. We convinced the staff it was the best bet, and they stayed; we basically had no turnover from that.

The staff was wise to hang around because redemption came in 2012. That year Maroon Financial’s loan portfolio took off, growing 40%. As expected, expenses went up too, rising 14% over the same year. Larger volumes result in greater expenses, but,for Maroon Financial, revenues went up even higher: nearly 66% from 2011 to 2012. That year, Maroon Financial’s staff received pay increases in the form of bonuses rather than raises because the credit union was only just emerging from its lossthe year before.

Today, the credit union services nearly every mortgage it originates, and in 2012 it increased net yield per loan to about 1.75 points, generating servicing income in every loan. In fact, Maroon Financial has been so successful at generating income this way that it plans to expand its business by brokering loans for other credit unions.

Although the economic environment is still challenging, Hernandez expects business in 2013 to look a lot like 2012. The credit union’s strategy has worked well so far, and its leadership sees no reason to change course after those stunning returns last year. Plus, the drop in its efficiency ratio will enable Maroon Financial to invest in more new products and expand its enterprise.

One area for investment that the credit union is considering is technology and IT infrastructure. The goal is to create the foundation necessary to bring the credit union’s outsourced services in house.

The initial investment can be daunting, Hernandez says. Among other things, the credit union will need to invest in more servers. In the long run, though, Hernandez expects the move to pay off.

We’re planting seeds for the next wave of growth, he says. We can’t just rely on our past success and say,We’ve done a great job,’ and let it be.