Consumers expect safety and reliability when traveling and making everyday purchases with their credit cards. Despite efforts to limit fraud through EMV chip technology, fraudsters are shifting their focus and moving elsewhere. Overall, identity fraud impacted 15.4 million consumers in 2016, an increase of 2 million victims from the prior year, according to Javelin Strategy Research. Even though there are alternative payment options for travelers, such as cash, traveler s checks and prepaid cards, those options come with risk of theft and high fees.

According to Experian s Summer Travel and Budgeting Survey Report from 2015, consumers used credit cards 82% of the time when making purchases during travel, compared with traveler s checks which were used only 16% of the time. The study also found that consumers use of credit cards during travel increased 11% in 2015 from the prior year, while the use of traveler s checks fell 12% year-over-year.

Another notable consumer behavior change is travelers use of mobile devices. Consumers use mobile devices during travel 64% of the time, an increase of 22% from 2014. Mobile usage is on the rise due in part to the fact that 81% of U.S. consumers over 13 own a mobile phone as of December 2016. That number has nearly doubled since 2011, according to the 2016 U.S. Mobile App Report.

How can technology help overcome the challenges of travel, while taking advantage of the increased prevalence of mobile technology?

In an effort to leverage the increasing ownership and use of mobile technology to fight fraud, geolocation has made its way into the payments space. Geolocation technology was developed by Visa in 2015 to bring increased safety and convenience to cardmembers.

This technology integrates into the issuer s mobile credit card app and enables the location of a card transaction to be matched to the location of the user s phone. By matching the two, the issuer has more data about the transactions to use in making approval decisions when cardmembers make out-of-pattern purchases.

Enabling geolocation both domestically and internationally can help avoid disruption to cardmembers, easing their travel challenges and ease concerns about fraudulent point-of-sale purchases. In particular, this technology can help reduce the occurrences of false positives, a decline at the point-of-sale based on an unexpected transaction. These false positives are one of the most challenging issues travelers experience when using credit cards.

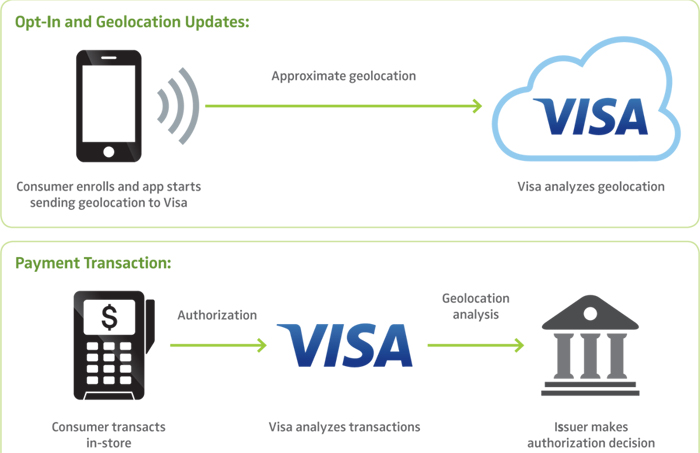

How Does Geolocation Technology Work?

Cardmembers can enroll in geolocation through their issuer s mobile application. Once they have opted in, the app will use mobile geolocation data in real-time to further enhance Visa s predictive fraud analytics ― matching the device location with the transaction location in less than a millisecond right at the point-of-sale (note: Visa uses the data for no other purpose).

In other words, when a cardmember transacts in a store, Visa can tell his or her issuer in the payment authorization message whether the cardmember s mobile phone is located near the merchant. The issuer can then factor that intelligence into its decision to approve or decline the transaction. This prevents fewer mistaken declines to occur, especially when cardmembers are traveling.

The technology has a limited impact on mobile battery life and data usage. It is not dependent on a phone number, allowing cardmembers to change SIM cards when traveling and even turn off data usage. The technology requires connection to wireless or Wi-Fi at least once daily to receive location signal.

Finding solutions to maintain convenience, safety and reliability in the ever-changing global commerce environment is important to all card issuers. Geolocation is one example of a technology that takes into account mobile devices, domestic and international travel and looming fraud to provide a solution that increases the security of cardmembers transactions. Other traditional forms of payment, along with new technology such as mobile wallets, will continue to be tested, and consumer behaviors likely will change as the functionality and safety of these forms of payment are tweaked and the limits of fraudsters are tested. Credit cards as a payment option have evolved and proven to be one of the safer and more reliable universal forms of payment. Geolocation will continue to strengthen credit cards longevity as a form of global payment.

Click here to download the full geolocation white paper.

Elan is a leading credit card provider in the industry that offers partners a suite of credit card products that competes with the national issuers, technology solutions that cater to audiences across the credit spectrum, and free access to a marketing engine to help generate new accounts. By partnering with Elan, financial institutions can offer cardmembers valuable mobile payment options such as Apple Pay, Android Pay, Samsung Pay, and Microsoft Wallet. For almost 50 years, Elan has delivered exceptional credit card products and service to more than 1,400 financial institutions.

For more information, call 1-800-223-7009 or visit www.cupartnership.com.