Top-Level Takeaways

-

MSUFCU reworked its online membership application to reduce abandonment rates and improve the member experience.

-

Positive results from the new application have prompted the credit union to plan enhancements to home banking options.

CU QUICK FACTS

MSUFCU

Data as of 03.31.19

HQ: East Lansing, MI

ASSETS: $4.4B

MEMBERS: 273,103

BRANCHES: 18

12-MO SHARE GROWTH: 9.2%

12-MO LOAN GROWTH: 11.6%

ROA: 0.81%

The member experience is a powerful motivator. According to recent statistics, nearly 75% of respondents identify experience as an important factor in purchasing decisions and 65% say a positive experience is more influential than great advertising. Research from Walker says experience is on track to overtake price and product as the key brand differentiator by next year.

Michigan State University Federal Credit Union ($4.2B, East Lansing, MI) aims to build a positive member experience by meeting, and exceeding, its members expectations. To do that might require introducing new products or services to meet new needs, but in the case of its online new membership application, MSUFCU knew an update was necessary.

We last touched it in 2010, says Sam Amburgey, MSUFCU’s chief information officer. We needed to revise it.

So, in 2017, the country’s largest university-based credit union dug in to overhaul the process and introduce the ability to apply for loans. MSUFCU formed a focus group composed of stakeholders from across the organization. The credit union knew how applicants used the existing application and what pieces of information that process wasn’t capturing like the ability to originate loans but including different stakeholders from payments, branches, compliance, lending, e-services, and more helped Amburgey and her team tap into a different kind of insight.

What were these individuals hearing from members? Amburgey asks. What did each department need to include in a new application?

MSUFCU created personas to better understand how different members might experience the new application differently. Just thinking about the member journey helped the credit union better grasp the various steps in the process and identify the functionalities it most needed to include and improve.

Sam Amburgey, Chief Information Officer, MSUFCU

By February 2018, the credit union was ready to design and code a new application.

Once They Shop, They Don’t Stop

In building the new application, now referred to as the Online Member Loan Application (OMLA), Amburgey had two clear objectives. The first was to reduce the abandonment rate. The second was to create a better user experience. But for the credit union to really address the former, it had to tackle the latter.

MSUFCU was working with a new member application process that was too long and missed several key components. For example, members couldn’t apply for loans, sign electronically, or electronically transfer money to fund a new account. Instead, members had to write a physical check or transfer money over the phone. Additionally, members had to navigate some 20 screens when inputting personal information.

To improve the experience, the credit union shortened the application, modernized the feel, and added functionality such as the ability to apply for loans and, for new MSUFCU members, the ability to immediately create online banking credentials. Once someone starts the application, the credit union doesn’t want them to stop until they’re set up and fully able to use their accounts.

We want them to get in and engage, Amburgey says.

As important as functionality is, so, too, are the look and feel of the application. To make sure this was on-point as possible, MSUFCU leaned on the research and understanding of the user experience designers on its IT staff.

We tried to model UX best practices in our design, Amburgey says.

One best practice is to follow set standards in website accessibility. For that, the credit union carefully considered color, text, and screen action, among other things.

Another best practice is to test, test, test.

We tested internally with our e-services employees, Amburgey says. Were they looking at what we wanted them to? Did they get our calls to action? Did they see where to click? What were they paying attention to?

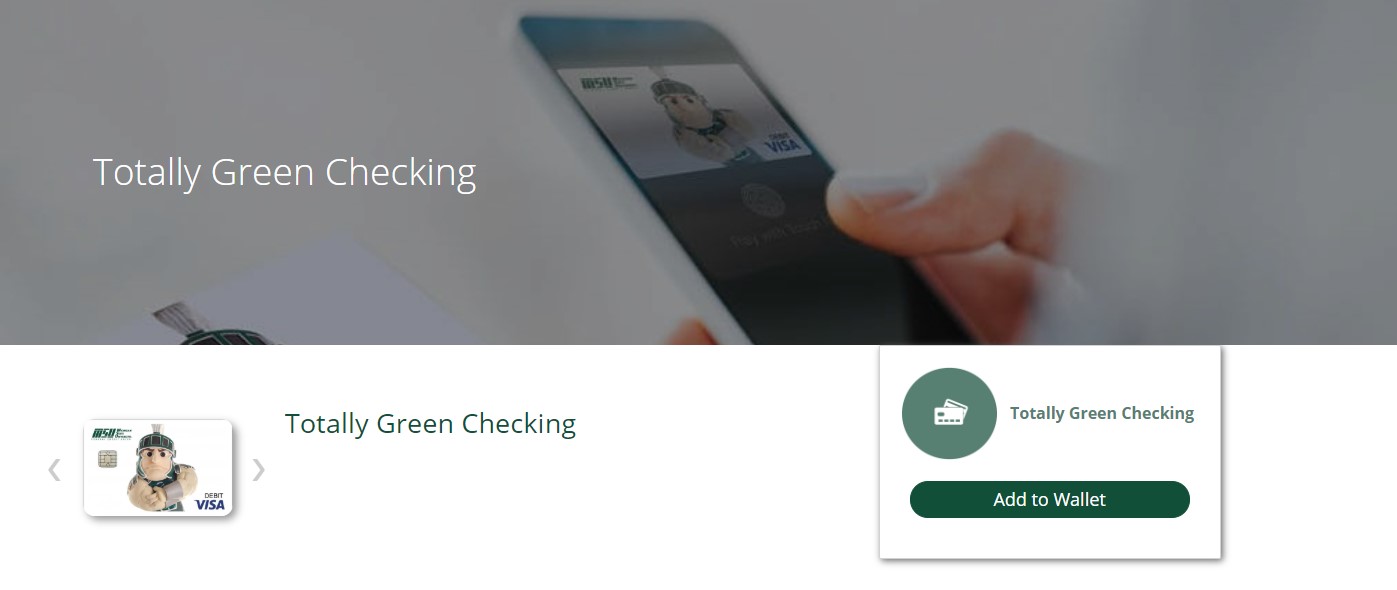

Ultimately, MSUFCU’s goal was to create a retail-like shopping experience with clear messaging that led new members through the application process. Today, members can shop the credit union’s website and add products like a checking account, a VISA card, or an auto loan to their wallet, and check out all through the OMLA experience.

To start the new membership application, members are prompted with a well-known retail-like functionality: Add to Wallet.

Many of our members are familiar with the online retail experience and adding that was something we thought could help them finish our application process, Amburgey says. Members select what they want, fill in their information, and check out.

Launch, Reception, And Feedback

For maximum impact, the credit union needed to launch its OMLA by June 2018, before the start of the new university year. MSUFCU opens accounts for nearly half of the freshman class, and June, July, and August are the busiest months.

MSUFCU uses the Agile Method to manage IT projects. The technology team works in sprints, pushing for a quick release of a minimum viable product and making improvements in subsequent iterations.

In this case, though, the minimum viable product was still a pretty big lift.

There was a lot we needed to include initially, Amburgey says. And there were features we wanted to add after that first release.

Included within the first iteration of OMLA, MSUFCU rolled out the ability to apply for a specific bundle of products that made sense for students. Students could open accounts for the credit union’s core deposit products including certificate, checking, and savings accounts as well as apply for a credit card, signature loan, or auto loan. To complete the process, they also could sign and fund their accounts through the new online process, move through onboarding, and set their preferences for automated email communications.

For three months, the credit union tested the effectiveness of its revamped online application. It tweaked the design and caught bugs. However, it didn’t want to make a slew of changes just as students were getting used to the process.

In September, the credit union added GAP coverage and other insurance products that were initially nestled under a learn more option. In March 2019, MUSFCU added youth accounts as well as products and services tailored to the credit union’s affinity groups.

After we launched, we focused on member feedback, Amburgey says. We wanted to find the pain points for people going through the process.

Perhaps counterintuitively, MSUFCU was able to gauge the effectiveness of the improved OMLA digital experience by monitoring in-branch transactions.

Students tend to open new accounts online in June or July before moving to campus in August. Previously, students had to visit a branch to complete the account application they started online. That’s not the case anymore.

Students were able to finish the application digitally instead of coming in to a branch, Amburgey says. We knew we’d improved the process when students opened accounts and showed up to school.

Feedback from stakeholders and members also has helped MSUFCU refine and improve the process. For example, the credit union has increased the visibility of the online application icon and has added language to reduce the number of members who mistakenly use OMLA to create additional accounts.

A number of existing members were using this application instead of signing into their account, Amburgey says. We interpreted this as the application being much easier and more streamlined than the process we have available elsewhere. We adjusted OMLA and have planned enhancements to our home banking options.

In its first 10 months, OMLA has proven even more successful than the credit union had anticipated. According to Amburgey, the abandonment rate for online membership applications has decreased 31%, and new online account openings have increased 74%. Amburgey attributes much of this to OMLA and the credit union’s willingness to rethink processes and modernize experiences.

There was almost a surprise in the increase in volume, Amburgey says. But I think these two numbers are reflective of the changes we made to the process.