Simplot Employees Credit Union ($18.7M, Caldwell, ID) is Exhibit A about how a small, old-school, single-SEG credit union can survive and thrive, even with members in multiple states.

Although its sponsor, J.R. Simplot Co., is one of the nation’s largest privately held firms, a diversified agribusiness that employs 10,000 people in several states and five countries, the credit union that bears its name is just now planning to install its first ATM at the company’s headquarters in Boise, ID. And the credit union has gotten by with services so plain it didn’t have so much as a locking night drop at its single branch at a major Simplot facility in Caldwell, ID, when Valerie Brooks took over as CEO in October 2011.

|

| Valerie Brooks left the Idaho Credit Union League to take the top spot at Simplot Employees Credit Union in October 2011. |

When I started at SECU we only had loans, shares, share certificates, 82 checking accounts, a few debit cards, and safe deposit boxes, Brooks says.

Now, SECU has more than 400 checking accounts, lines of credit, VISA credit cards, online and mobile banking and bill pay, and student lending. That’s despite a small drop in raw membership numbers because the credit union scrubbed dormant accounts from the rolls.

Brooks was no newcomer to credit unions when she joined SECU. She had been regulatory and governmental affairs at the Idaho Credit Union League, where she spent 11 years after 22 years before that in collections, lending, operations, and member services at two different credit unions.

Simplot Employees Credit Union shares its templates for dormant account closings and more in Callahan’s online Executive Resource Center, available only to Callahan clients.

After Brooks took the helm at SECU, the positive metrics started piling up. For example, SECU’s ROA of 1.48% is among the top 30 for credit unions of $10 million to $20 million in assets as of the second quarter of 2016. That’s also in the top 5% of all credit unions nationally.

And with only eight employees, SECU’s net income per FTE in the second quarter was $34,524, compared with $8,149 for its asset-based peer group and right in line with the $34,671 average for all U.S. credit unions.

CU QUICK FACTS

simplot employees Credit Union

Data as of 06.30.16

- HQ: Caldwell, ID

- ASSETS: $18.7M

- MEMBERS: 4,745

- BRANCHES: 1

- 12-MO SHARE GROWTH: -2.133%

- 12-MO LOAN GROWTH: 7.64%

- ROA: 1.48%

Equally impressive: SECU’s second quarter 2016 operating expense per member was $77, compared with $119 for its peer group and $181 for all U.S. credit unions. And its efficiency ratio stands at 72.78%, compared with 93.69% for its asset group and 80.92% as an average for the nearly 6,000 credit unions regardless of size.

So how does Brooks and her team do it? By investing in products and committing to service. Check out these two Google reviews. They thank the member for the review and promise more to come. For example: You are right we are at one location. However, we make every effort to serve well through phone, mobile, online, and email. Watch in 2016 for even better access with upgraded mobile apps and remote deposit capture.

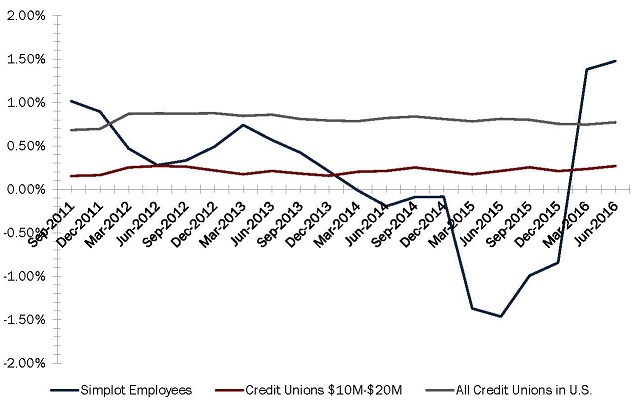

RETURN ON ASSETS

FOR U.S. CREDIT UNIONS* | DATA AS OF 06.30.16

Callahan & Associates | www.creditunions.com

*For 5,976 credit unions

Source: Peer-to-Peer Analyticsby Callahan & Associates.

Simplot Employees Credit Union’s investment in technology and commitment to member service is now paying off in a sharply higher ROA than its peer credit unions.

The Importance Of Vendor Relationships

Brooks says positive vendor relationships have been critical to SECU’s growing success and are a continuation of the ties she’s built over the years.

Each vendor with which I had previously built a relationship has taken me under their wing and provided exceptional resources from which to draw, she says That includes searching for grants and other support for us and championing our success. A good reason to never burn your bridges no matter what the circumstance.

Often loyalty can be bought for one-tenth of a basis point, but if you focus on the essentials and rock star service, you will earn those loans back with the next promotion.

Brooks also relies on advice from other credit unions as she vets possible new vendor relationships. That helps her fully understand SECU’s own needs so she can communicate them to her potential new solutions providers. Those principles got put to the test with a recent selection and conversion to a new core processor.

Our home banking vendor recommended a few core processors that integrate well with their product, she says. We settled on one, and it has made a tremendous difference in what we can offer our members.

The vetting process relies on a simple spread sheet that has a list of all non-negotiable things and a wish list. Brooks puts each potential vendor at the top and goes down the list answering yes or no and the implementation cost, monthly cost, and contract terms. That’s followed by talking to other credit unions and getting their feedback on the vendor.

I try to call more than just the credit union’s the vendor recommends, Brooks says. I never tell one vendor what another says or charges but give them all the opportunity to bid the business equally. I make sure I understand what we need and then make sure the vendor understands what we need. Ongoing management of those relationships takes time as with any relationship. Sometimes it takes patience.

Simplot Employees Credit Union uses the CU Centric core processing system as well as HomeCU for home banking, CU People for payroll processing, and the Illinois Credit Union League for debit and credit cards. Find your next solution in the Callahan & Associates online Buyer’s Guide.

Building Member Relations One Loan At A Time

Brooks attributes her credit union’s growth to member education and to promoting lower rates for re-financing existing loans elsewhere and for new loans. Other tactics have included a VISA balance transfer promotion and a December skip-a-pay for a donation to the Ronald McDonald House.

That’s a charity near and dear to our sponsor group. Doing that put us on the map, getting us interest in our loans from members and potential members alike, Brooks says.

One Member At A Time

So how does a small, single-SEG credit union survive and thrive, even with members in multiple states? Here Valerie Brooks, CEO of Simplot Employees Credit Union, shares some tips in her own words.

- Once you have established safety and soundness, set about building a relationship with the SEG.

- Support what they support (Ronald McDonald House, United Way, etc.)

- Be helping hands to their staff in the community.

- Be champions of their company, partners, and affiliates. Be their biggest cheerleader.

- Honor their name, their company, and their employees.

- Be everywhere they are and be a shining example. Make them proud to be affiliated with your credit union, with you. That means being a good corporate citizen, consistently positive communication, build goodwill, live and work with integrity.

- Be careful how you come across whether it’s at work, at home, or especially on social media. We use social media in a positive way. Sometimes with humor.

- Everyone is our competition. The employees of our SEG can join most credit unions and be customers of any bank. We are a destination and not on every corner. We have to be rock stars in service. We use technology to serve Simplot employees through the country.

- That being said; we are in a cooperative movement and we do not undermine others to succeed ourselves. And we help other small credit unions.

Another big push was expanding new car lending at the local plant and other Simplot facilities nationwide. Members can apply for loans online and the credit union considers credit scores; however, they are not the end-all, be-all.

We’ve worked hard to help some members get out of payday lenders with financial education, listening, and offering better rates as their scores improve, Brooks says.

And, the CEO says, the credit union’s C, D, and E paper do almost as well as its A-B paper.

The results also include a growth in new and used auto loans of 13.90% and 6.37%, respectively, in the second quarter, well above that of the average small credit union. And its ratio of members to potential members is 67.79%, dwarfing the 5.53% of its asset-based peer group.

The staff may be small, the SECU CEO says, but it works hard and smart.

Getting the right team in place, communicating with the entire team how we can be successful, that all naturally helped our efficiency, Brooks says. We eliminated a position while keeping strong benefits and positioning the staff in the best place for their abilities. And as people retired or left, I found exceptional people for our management team.

She also advises not to try to be all things to all members:

You can’t have the lowest-priced loans and pay the highest dividends, plus give everything else for free, she says. You manage a financial cooperative, so make sure the relationship between you and your members is mutually beneficial. Often loyalty can be bought for one-tenth of a basis point, but if you focus on the essentials and rock star service, you will earn those loans back with the next promotion.

Bottom line, Brooks says, a small credit union like hers, or any other, can succeed by building a solid foundation with tight checks and balances, proper compliance, and a great team.

Plug any holes, she says. Find areas where serious losses could arise and fix those. Then you can move to the products and services you can sell to your members with confidence.

You Might Also Enjoy

- The Year Of The Employee

- How Alliant Plans To Triple Down On NII

- 3 Member Service Successes In Second Quarter 2016