CU QUICK FACTS

Innovations FCU

Data as of 03.31.19

HQ: Panama City, FL

ASSETS: $272.5M

MEMBERS: 20,259

BRANCHES: 6

12-MO SHARE GROWTH: 39.0%

12-MO LOAN GROWTH: 8.2%

ROA: 0.96%

Prior to 2013, business lending was never an area of strategic emphasis for Innovations Federal Credit Union ($272.5M, Panama City, FL), says chief operations officer Scott Gladden, who’s been at the Florida cooperative since 2005.

We made some business loans here or there, he says. But it was never our focus.

Then the Great Recession hit. In the three years following the economic shock, the financial institution market in Bay County the only county the community-chartered cooperative serves changed entirely. Many community banks closed their doors; when that happened, the community lost its only source of business loans.

There was a void in our market, Gladden says. The big banks didn’t want to offer loans and other services to the small business owners in our market, and the community banks who traditionally served these populations were gone.

Located in Panama City, an economic market dominated by tourism and the service jobs that support it, Innovations serves a predominately low-income membership. To more fully support their business needs, the credit union made a choice to fill the business services gap.

A Note About Business Loans

In third quarter 2017, the NCUA changed how credit unions report member business loans, creating a category for commercial loans that are not subject to the cap. Despite the category distinction, there are several loan types that are classified as both member business and commercial loans, making a like-for-like comparison difficult.

In the fall of 2013, Innovations hired commercial banker David Powell as its new business development officer to jumpstart interest and activity in its business services, which includes a full suite of loans, fee-free accounts, and cards. In the years since, the credit union’s member business and commercial lending portfolios have grown well, with the potential to grow larger as the community rebuilds in the aftermath of Hurricane Michael, the Category 5 hurricane that ravaged the Florida Panhandle in October 2018.

In this QA, Gladden discusses growth, team-building, and rebuilding in the wake of environmental disaster.

Why did you decide to offer a full suite of services?

SG: We asked ourselves, if we were small businesspeople what services would we need? We realized the need for business accounts from checking and savings to money markets and certificates that we wouldn’t charge for. We can do anything. We can handle your account, and if you need a small loan, we’ve got that for you, too.

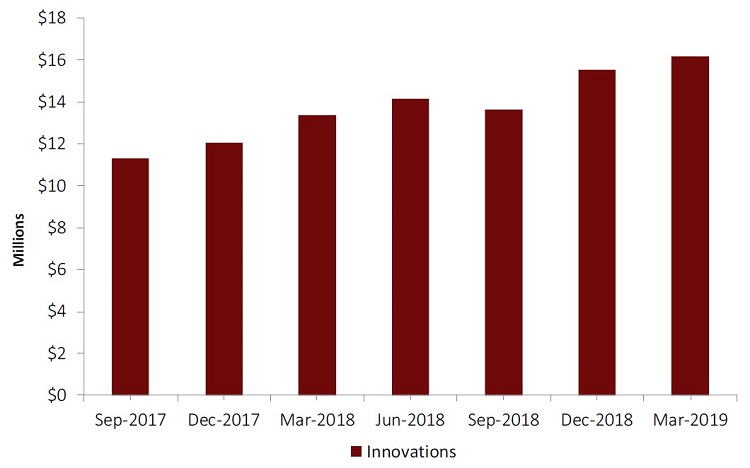

COMMERCIAL LOAN BALANCES

FOR INNOVATIONS FCU | DATA AS OF 03.31.19

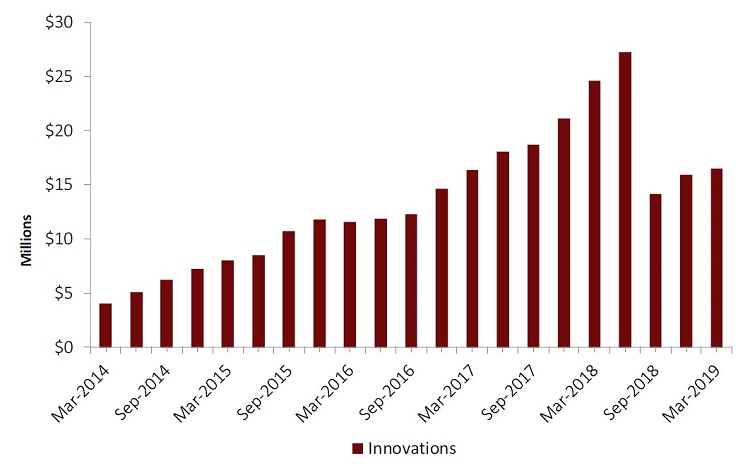

MEMBER BUSINESS LOAN BALANCES

FOR INNOVATIONS FCU | DATA AS OF 03.31.19

Since jumpstarting its business services offerings in 2013, Innovations’ business loan portfolios have added millions to its balance sheet and provided service to a community in need. One note: NCUA’s reclassification in the reporting standards for single-family residential properties caused a one-time drop in member business loan balances between second and third quarter 2018.

Your total business lending portfolio has grown consistently since 2013. Who is your target borrower?

SG: There was that void in our market, but we wanted to find a niche within that where we could live and operate that fit our credit union. Really, when we started trying to grow we looked for our members who were also small business owners, and those small business owners who weren’t members but should have been. The big banks didn’t want them, the small banks were gone, and the other credit unions in town weren’t ready to offer those services. We were.

How much of an impact has the hiring of your business development officer had on the success of your program?

SG: That was a big hire for us, because David [Powell] was already well-known in the community. He knows everybody, from chamber presidents to committee members, and he’s opened people to the idea that credit unions can offer these types of services. He’s helped us grow this program at the pace we want to grow it. We’re not trying to put up big numbers, though it’s grown well. We’re a low-income designated, CDFI credit union. We’re trying to serve members and take care of people.

What pace of growth are you looking for from this portfolio?

SG: We look at how these loans fit with the rest of our concentration analysis. Right now, we’ve got nearly $35 million in our business portfolios. We’ll see how this line of business fits our budget and the overall loan growth projections for the credit union. I think this will change from budget year to year.

We try to grow our total loan portfolio around 10% each year. I’ve seen credit unions that try to grow faster, and put up big numbers, give up something somewhere else, like underwriting. 12-18 months later their delinquencies and charge-offs spike, and we don’t want to do that. Plus, regulators don’t like big, fast growth numbers. They put you under more scrutiny, even if you’re doing it well. We prefer to approach it in a consistent, safe, sound manner.

The big banks didn’t want them, the small banks were gone, and the other credit unions in town weren’t ready to offer those services. We were.

Starting with that business development officer in 2013, how has the team grown? Who is responsible for what?

SG: David really started it, and then he hired an assistant who helps him keep track of all the moving parts. Other loans, you can put them on the books and forget them. With business and commercial loans, you have to monitor: are they giving you updated financials? Are they paying their taxes? Insuring their property? Following covenants that may be part of the agreement? Then, you have to continually risk-rate them.

Since then, we’ve added a loan officer, who really helps those looking for business services know where to start. Do they have a business plan? Do they know how to incorporate their business? He talks them through those initial steps and helps them understand what information they need to provide before they can apply for a loan.

That’s our department, but other folks help as well.

Like who?

SG: Me, our CEO (David Southall), and the head of our mortgage department, Mark Harwell. We’re on the loan committee, evaluating loans, though Mark does all the underwriting. For our document processing and more complex underwriting, we use third-party Lucro Commercial Solutions from Tallahassee, FL.

Sustainable Business Strategy

Learn more aboutSustainable Business Strategy with Rebecca Henderson, in collaboration with Harvard Business School online. The Callahan Academy combines Harvard teachings and credit union industry discussions to explore:

- Business models that drive change.

- Tactics that demonstrate the competitive advantages of being a purpose-driven firm.

- Why collective efforts are important and how business can be a catalyst for system-level change.

- What you can do to become a purpose-driven leader and how you can develop purpose-driven leaders within you organization.

How has this program grown within the community?

SG: We’ve just started to advertise, but our business development officer is connected to everybody. And he attends Chamber of Commerce meetings, sits on committees. He’s often asked to emcee events. He’s everywhere. What happens is, once someone finds out we offer business services and they have a good experience with us, they tell their friend, who tells their friend.

People still don’t think credit unions offer these services. But once you can develop a network like that, we get enough business to keep us busy.

With Hurricane Michael now a few months in the rearview, what are you doing from a business lending perspective to help your community rebuild?

SG: We don’t necessarily offer rebuilding loans. We’ve seen members with building damage or who’ve needed to expand their businesses to serve hard-hit areas. We’ve helped in those cases, and we recently applied for a second CDFI grant more specifically for rehabilitation and rebuilding loans.

We also offered deferments during the hurricane, but that hasn’t affected our credit quality thus far. Many of them collected on insurance claims and they’re still sitting on a lot of cash. That’s actually helped many people.

In 2018, you received a CDFI financial assistance grant from the U.S. Treasury and have applied for another this year. How much were you awarded and what will these grants help you accomplish?

SG: We’re the credit union for Bay County. And as we thought of all the ways we can help improve our community, we decided applying for a grant to benefit business lending was a good way to achieve that. If we can help to start a business, or expand one, it’ll provide a perpetual benefit. Starting or expanding means they’re able to employ more people who can shop in more stores and eat in more restaurants. For me, if we can help small businesses grow in our community, the effect of that is going to be bigger than helping someone remodel their house.

We were approved for $500,000, and the funds are divided into three categories: micro-enterprise loans, startup business loans, and business readiness loans. Along with that, the grant allotted funds for technology upgrades, account reserves, capital, and staff hiring.

How much of that have you awarded to members?

SG: $250,000 since December. We were awarded the funds in September, but when the hurricane hit it pushed our scheduled rollout to members back a few months.

But the need is certainly there over the course of 2019?

SG: It’s ramping up now, and we expect to award more in the next several months. We started to advertise in the Bay County and Panama City Beach chambers of commerce trade magazines, but we want to be strategic about it and put it in publications small business owners are more likely to see.

We’ve already awarded funds for hurricane cleanup. Some are helping existing businesses buy another truck or trailer or piece of equipment, others are working on building fences because everyone’s fence is gone. There’s five-years’ worth of fence building left in this town.

This article appeared originally in Credit Union Strategy Performance. Read More Today.

Wait, There’s More!

This is just one section of the Anatomy Of Innovations Federal Credit Union series that appears in Credit Union Strategy & Performance. Read the whole discussion today.

READ MORE