As the economic ramifications of COVID-19 swept through the country, consumers moved their savings into deposit accounts. According to FRED Economic data from the Federal Reserve Bank of St. Louis, the personal savings rate in the United States reached33.5% in April, its highest rate on record. Although the Federal Reserve is keeping interest rates low to spur economic activity, the safety of deposit accounts attracted consumers nationwide. The slowdown in day-to-day spending as a result of businessclosures contributed to this trend, but as economies reopened, the personal savings rate dropped to 19.0% as of June 30.

Key Points

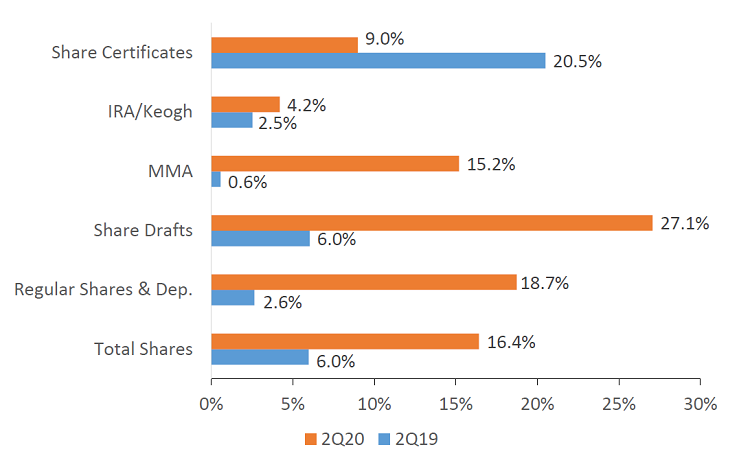

- Total share balances increased $212.7 billion year-over-year and surpassed $1.5 trillion as of the second quarter. This equated to an all-time high growth rate of 16.4%.

- Share draft balances increased 27.1% annually to $263.7 billion. As interest rates remained low, these accounts provided an attractive liquidity insurgence for credit unions nationwide.

- Share certificates increased 9.0%, an 11.5 percentage point deceleration year-over-year. Low interest rates have incentivized members to core deposits in lieu of interest-bearing accounts.

- Average share balance per member increased $1,364 in the past year to $12,082. This is a 12.7% annual increase.

SHARE GROWTH BY TYPE

FOR U.S. CREDIT UNIONS | DATA AS OF 06.30.20

Callahan & Associates | CreditUnions.com

Core deposits were the catalysts of deposit growth at credit unions nationwide. These products accounted for 87.1% of annual deposit growth as of the second quarter.

DEPOSIT PORTFOLIO

FOR U.S. CREDIT UNIONS | DATA AS OF 06.30.20

Callahan & Associates | CreditUnions.com

Regular share balances neared $562.0 billion in the second quarter, the largest balance ever recorded. These deposits continued to make up the largest proportion of credit union shares.

LOAN TO SHARE RATIO

FOR U.S. CREDIT UNIONS | DATA AS OF 06.30.20

Callahan & Associates | CreditUnions.com

The loan-to-share ratio continued to decrease and has fallen 7.1 percentage points in the past 12

The Bottom Line

Despite the Federal Reserve keeping interest rates at all-time lows, credit unions reported an influx in share balances as members sought safe channels to park their money. Furthermore, loan deferment programs allowed consumers to save loan payments andbuild savings. Balances in share drafts, regular shares, and money market accounts increased 19.6% year-over-year. Certificate growth decelerated 11.5 percentage points. Combined with lower interest rates, this drove a slowdown of 8 basis points inthe average cost of funds, which dropped to 0.89%. The industry’s loan-to-share ratio decreased 7.1 percentage points in the past 12 months to 76.2% as of June 30, alleviating concerns about liquidity following a decade of loan growth.

This article appeared originally in Credit Union Strategy & Performance.