Credit unions delivered exceptional value to members in fourth quarter 2018 across a host of metrics. Read on to learn the full story.

Macro Economic Trends

GDP Expands; So Does Consumer Debt

-

At 2.6%, annual growth in real GDP hit its highest year-end rate since 2013.

-

The inflation rate closed out the year at 1.9%. This was half the annual wage growth, meaning the average U.S. employee had more purchasing power.

-

The Federal Reserve increased interest rates four times in 2018 but has indicated it will not increase rates in 2019.

Positive GDP growth through the end of 2018, all-time low unemployment levels, and wage growth that outstripped inflation all contributed to U.S. economy expansion in the final quarter of the year. The rate of growth, however, was slower than in the first half, as stock market volatility combined with the Fed’s slowdown in rate hike projections had consumers debating the future of the economy.

Growth dynamics, interest rates, and hiring trends all provide important insight into service opportunities, says Jay Johnson, partner at Callahan Associates. Credit unions would be well-served monitoring broader economic trends as well as their local economies.

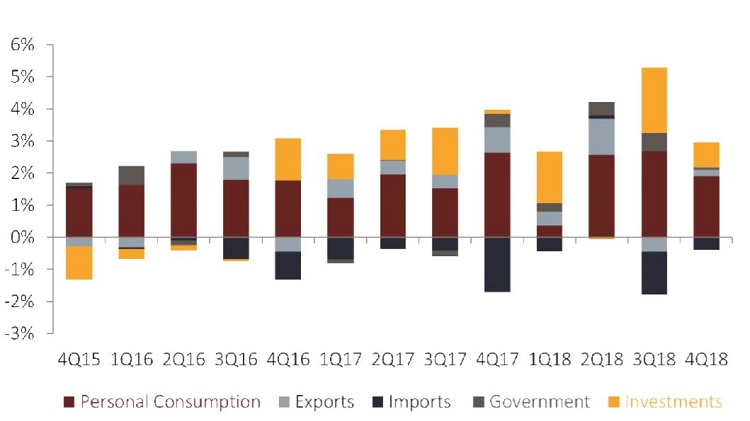

The fourth quarter of 2018 represented the 19th consecutive quarter of real GDP growth. Real GDP grew 2.6% annually to $18.8 trillion. That’s down from 3.4% in the third quarter and 4.2% in June, the high for the year. However, real GDP has remained the same or dipped in the fourth quarter of every year since 2011, and this year’s 2.6% is the highest year-end rate since 2013.

The trend in personal consumption, which accounts for 69.4% of U.S. GDP, was similar to GDP. Adjusted for inflation, consumer spending was up 2.7% annually and surpassed $13.0 trillion in the fourth quarter. Personal consumption increased $337.9 billion through the year and accounted for 1.9 percentage points of total GDP growth.

The total value of U.S. imports increased 3.5% year-over-year to $3.5 trillion as of Dec. 31, 2018. Total exports increased 4.1% annually to $2.6 trillion in the fourth quarter; however, net exports represented a loss of $963.2 billion $64.0 billion more than one year ago. The U.S. trade deficit as of Dec. 31 was the highest on record and deducted 5.1% from total GDP and 22 basis points from annual GDP growth.

Government spending, which has increased for the past five consecutive quarters, was up 1.8% annually to $3.2 trillion; total investment in the economy was up 7.0% year-over-year to nearly $3.5 trillion. These segments made up 17.0% and 18.5%, respectively, of total GDP.

COMPONENTS OF TOTAL GDP GROWTH

DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

Annual growth in GDP slowed in the second half of 2018, closing the year at 2.6%. Of note, the U.S. trade deficit as of Dec. 31 was the highest level ever recorded.

Source: Federal Reserve of St. Louis

Core personal consumption expenditures (core PCE) increased 1.9% annually, slightly below the target inflation level of 2.0%. The Federal Reserve’s preferred measure of inflation, core PCE excludes the more volatile sectors of food and energy to more accurately express the value of the dollar. After growing for four consecutive quarters, core PCE in the fourth quarter was down slightly from 2.0% in the third. According to the Federal Reserve Bank of Atlanta, wages increased 3.8% nationwide in 2018. With wages growing at a faster rate than inflation, the average employee is enjoying more purchasing power.

Additionally, with unemployment at notably low levels, there are more employees enjoying that purchasing power. The national unemployment rate was 3.9% as of Dec. 31, 2018, the lowest year-end rate since 1969. The participation rate for year-ends 2018 and 2017 were the same 62.9% however, the unemployment rate at year-end 2017 was 4.4%, underscoring that an increase in jobs was the primary contributor to falling unemployment in 2018.

The national unemployment rate continued to move downward in 2018, says Sam Taft, associate vice president of analytics and business development at Callahan Associates. Inflation remains low, but continued low unemployment is likely to continue pushing wages higher in 2019.

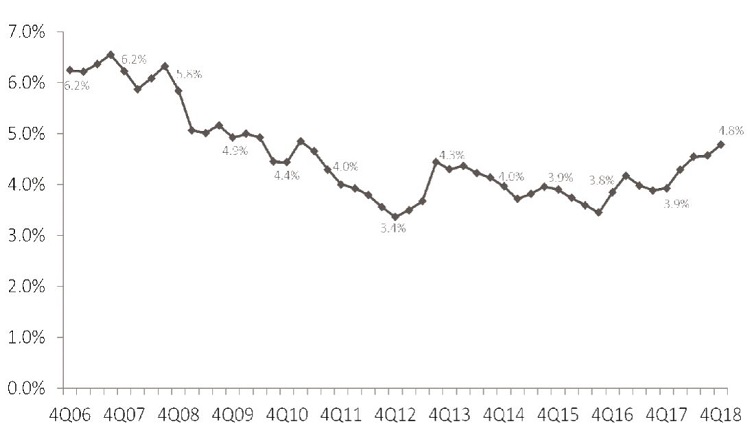

The Federal Reserve raised its benchmark interest rate four times in 2018. Although economists initially expected three more hikes in 2019, the Fed this year has lowered its projection to zero and will keep the federal funds rate at 2.50%, which is within the Fed’s target range of 2.25% to 2.50%. At year-end 2018, the average rate for a 30-year fixed-rate mortgage was 4.78%, 86 basis points higher than at the beginning of the year and the highest rate since the first quarter of 2011 when it was 4.85%.

30-YEAR FIXED MORTGAGE RATES

DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

The average 30-year fixed-rate mortgage increased 86 basis points year-overyear. The Fed raised rates four times in 2018 but has indicated it will not raise rates in 2019.

Source: Federal Reserve of St. Louis

The Mortgage Bankers Association (MBA) reported U.S. financial institutions originated $392.0 billion in mortgages in the fourth quarter. This brought total originations in 2018 to $1.6 trillion, 3.9% less than in 2017. Refinances dropped 23.7% from $600.0 billion in 2017 to $458.0 billion in 2018. The 6.8% increase in purchase originations from $1.1 trillion in 2017 to $1.2 trillion in 20118 was not enough to make up for the drop in refinances.

Read the full analysis or skip to the section you want to read by clicking on the links below.

INDUSTRY AT-A-GLANCE BALANCE SHEET: ASSETS LOAN BALANCES MARKET SHARE ASSET QUALITY INVESTMENTS BALANCE SHEET: LIABILITIES SHARES LIQUIDITYINCOME STATEMENT

Total household debt hit an all-time high of $13.6 trillion. As of Dec. 31, housing debt accounted for 69.9% of total debt in the economy. National housing debt ticked up to $9.5 trillion at the end of 2018, according to the Federal Reserve Bank of New York. This was a $21 billion year-over-year increase as national housing debt inched closer to the prerecession high of $10.0 trillion.

Household debt continues to increase nationwide and is reaching pre-recession levels, Johnson, says. The economy is strong, but consumers and institutions alike must monitor debt levels for indications of financial stress.

The Federal Reserve reported student debt was nearly $1.6 trillion in 2018, a 132.2% increase in the past decade. Of the total student debt balance, 78.8%, or $1.2 trillion, are federal loans. The remaining 21.2% are private. Nationally, student loans had a 90-day delinquency rate of 11.4% as of Dec. 31, 2018; however, different underwriting practices have resulted in far lower delinquency in private loans versus federal. Moving forward, lenders particularly federal lenders must manage the financial toll of high default rates.

Looking forward, the continued strength in the U.S. economy will depend on the management of delinquencies in household debt payments, adjusted projections to rate increases and their effect on loan and deposit pricing, and volatility in the stock market. All of these factors will play a vital role in how consumers interact with the economy and, in turn, how credit unions interact with their members.

Credit unions must continue to monitor macroeconomic trends as they compete in the larger financial services industry, Taft says. Debt dynamics and interest rate trends, in particular, are areas of direct significance to members.

Credit Union Trends

Industry At-A-Glance

Top-Level Takeaways

-

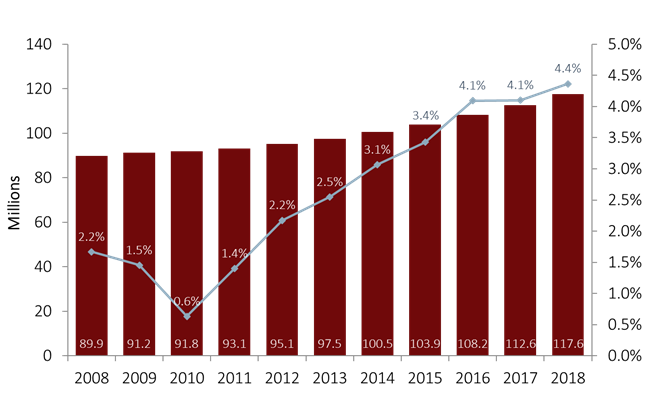

Membership at U.S. credit unions increased 4.4% year-over-year, pushing the industry to 117.5 million members.

-

Share draft penetration, a common measure for determining the percentage of members who use the credit union as their primary financial institution, reached 57.8% in the fourth quarter of 2018.

-

The average member relationship increased $542 in 2018.

2018 was a great year for credit unions nationwide. On the back of a strong economy, with GDP up 2.8% over the year and unemployment levels at record lows, credit unions strengthened member relationships and expanded their balance sheets. In the current climate, cooperatives are reporting notable gains in income and loan but are increasingly facing liquidity pressures.

Membership

Annual membership growth remained a cornerstone of credit union success in 2018. During the year, 5.1 million people joined a credit union and industry membership hit 117.5 million by Dec. 31. Annual membership growth increased 26 basis points year-over-year to 4.4% as of Dec. 31, 2018. In fact, year-end growth has been faster every year since 2010 as more people choose a member-focused, not-for-profit financial services provider.

MEMBERSHIP AND ANNUAL GROWTH

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

Credit union membership increased 4.4% in 2018 to 117.6 million as of Dec. 31. That’s 26 basis points faster than credit unions recorded in 2017.

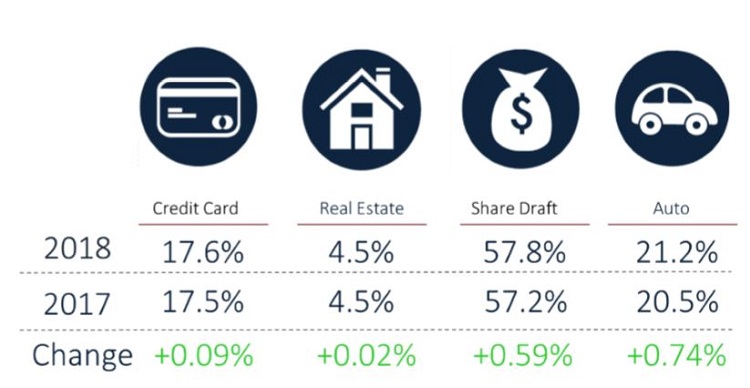

The influx of members, however, has not diluted the ability of credit unions to cross-sell products. Penetration rates were up year-over-year across the board. Share draft penetration, often used as a proxy for the percentage of members who use the credit union as their primary financial institution, increased 59 basis points in 2018 to 57.8% as of Dec. 31.

In addition to deposits, members also expanded their relationship through loan offerings. Auto (21.2%), real estate (4.5%), and credit card (17.6%) penetration rates all increased in tandem with membership growth, and year-over-year were up 74, 2, and 11 basis points, respectively. Today, credit unions finance more than one in five auto loans nationwide. Auto lending continues to be the bread and butter of credit union lending, with 21.2% of members holding an auto loan with their credit union as of Dec. 31, 2018.

PRODUCT PENETRATION RATES

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

Penetration rates or, the percentage of members who hold these accounts at U.S. credit unions increased annually in all major lending categories plus share drafts.

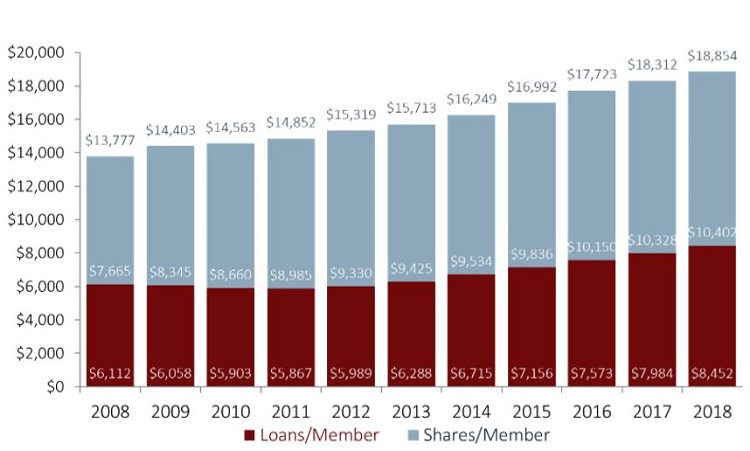

Member engagement consistently appreciates at year-end, but these gains are a byproduct of both adding members and developing deeper relationships, says Johnson. In fact, the average member relationship, defined as the average consumer loan and savings balances a member holds at the credit union, was up $542 in 2018 to $18,854.

AVERAGE MEMBER RELATIONSHIP

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

Overall, members are more engaged with their credit unions, which has pushed the average member relationship higher.

Credit unions reported year-end gains in loan and share balances per member. Average loans per member increased from $7,984 in the fourth quarter of 2017 to $8,542 in the fourth quarter of 2018. That’s a 5.9% year-over-year increase. The average share balance held by credit union members hit $10,402 a 0.7% annual gain. This growth dynamic is consistent with broader credit union industry trends, where loan balances are increasing at faster rates than share balances.

Financial Overview

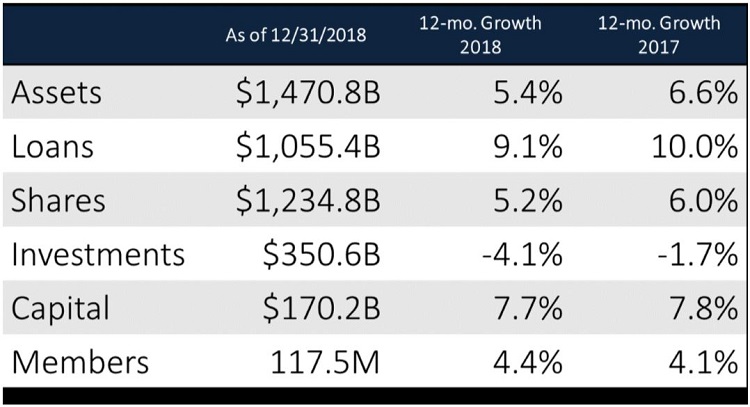

The number of active credit unions continued to trend down in 2018. There were 5,492 credit unions operating at the end of 2018; that’s 197 fewer credit unions than one year ago. The year closed with 3,376 federally chartered and 2,116 state-chartered credit unions. Consolidation through mergers and acquisitions is the leading reason for this decline. Since year-end 2013, 1,121 credit unions have been merged into or acquired by another institution.

Despite a drop in numbers, total credit union assets increased 5.4% in 2018 to $1.5 trillion as of Dec. 31. Investment and cash balances decreased 4.1% annually to $350.6 billion as credit unions increasingly elected to runoff investments to fund loan demand.

Loan balances increased 9.1% year-over-year to nearly $1.1 trillion. Although that growth rate was 97 basis points slower than what credit unions reported in 2017, for the first time ever, credit unions have ended the year with aggregate industry loan balances greater than $1 trillion.

Annual deposit growth also slowed in 2018. It was down 69 basis points year-over-year to 5.3%. Total share balances surpassed $1.2 trillion in 2018 and have been higher than $1 trillion at year-end since 2015. Still, loan growth has outpaced share growth for the past 23 quarters, and the 85.5% loan-to-share ratio recorded in the fourth quarter is the highest on record.

INDUSTRY OVERVIEW

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

Membership growth has accelerated as more consumers embrace the credit union model. However, annual growth on both sides of the balance sheet has slowed.

Balance Sheet: Assets

-

Loan balances increased 9.1% year-over-year.

-

New auto loans were up 11.7% year-over-year.

-

Credit union market share across all major loan products has expanded in the past 10 years.

What’s happening in the broader economy heavily influences trends in the credit union balance sheet. For example, the Federal Reserve implemented four rate hikes in 2018 the fourth occurred in December 2018 and financial institutions are subsequently charging higher rates on their loan offerings.

The average interest rate for a 30-year fixed-rate mortgage was up 86 basis points in 2018 to 4.78% in the fourth quarter. But as loans become more profitable, deposits become more expensive. As credit unions rely largely on deposits to fund lending, they are implementing new ways to meet strong loan demand, including by running off investment balances.

Loan Balances

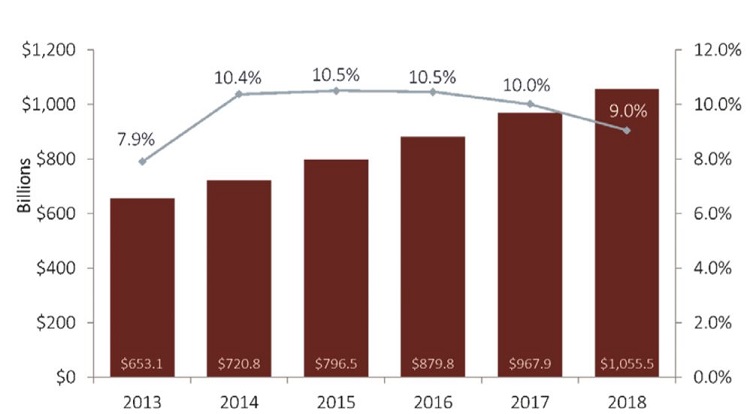

Prior to 2018, U.S. credit unions had reported double-digit loan growth for four consecutive years. Growth for 2018, however, came in at 9.2%. Although still strong, this was 97 basis points slower than credit unions recorded in 2017. What’s more, annual loan growth for the industry has decelerated at year-end for each of the past three years. Still, loan demand remained robust and aggregated credit union loan balances surpassed $1 trillion at year-end for the first time ever.

TOTAL LOANS AND ANNUAL GROWTH

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

Total loan growth dropped below double-digits in 2018, but credit union loan balances surpassed $1 trillion for the first time ever.

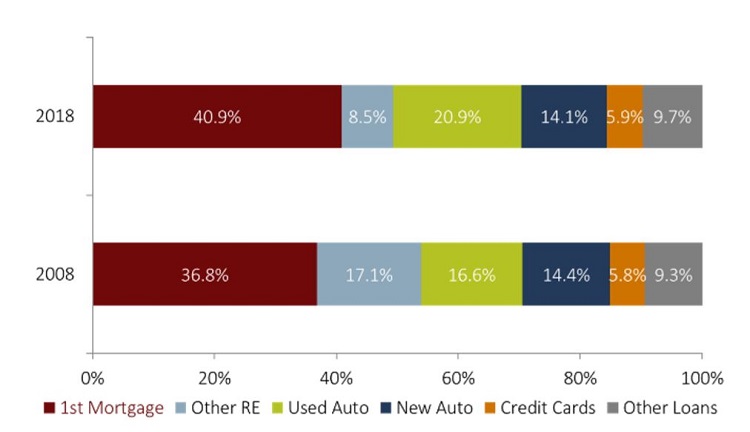

Other real estate was the only loan product in which credit unions recorded accelerated annual growth. Loan growth in that segment increased 6 basis points to 7.0% and balances hit $89.3 billion. By year-end 2018, these loans comprised 8.5% of the overall loan portfolio. Despite the accelerated growth, other real estate loans have grown at the slowest pace of any loan product, and their share of the loan portfolio has declined 8.6 percentage points in the past decade. Consequently, the share of the loan portfolio held by total real estate loans has decreased 4.5 percentage points in the past 10 years to 49.4% as of Dec. 31.

Since the Great Recession, home equity lending has been slow to regain momentum, Johnson says. Sharp declines in home values made homeowners wary of further leveraging their homes. As such, other real estate loans have only recently re-emerged as a leading product.

First mortgages, however, have continued to be a source of growth. Aggregate balances for this product segment reached $431.6 billion at year-end 2018 a 9.2% increase year-over-year. In the fourth quarter of 2018, first mortgages accounted for 40.9% of the industry’s overall loan portfolio, the largest share of any credit union loan product, versus 36.8% at year-end 2008.

First mortgages are and continue to be an integral part of the loan portfolio. They are typically the largest loan a member will take from the credit union and have been a sound asset since the aftermath of the recession. Historically, refinance and recapture loans have provided credit unions a foothold in the mortgage market. However, it is purchase loans that fuel deeper relationships with members, particularly in a rising rate environment. Cooperatives must continue to develop a first mortgage pipeline that expands their exposure beyond refinance and recapture programs.

Credit card loan balances grew 7.5% in 2018 and neared $62.4 billion at year-end. Credit card balance growth, however, decelerated 1.6 percentage points from the year prior. This was the fastest deceleration of any loan product. Unfunded commitments were up 9.5% year-overyear to $134.2 billion as credit unions extended credit at a faster rate than members used it. On the whole, as credit unions push to become their members’ primary financial institution, they need to raise lines of credit and loan balances in unison.

New auto loans grew at the fastest rate of any segment they were up 11.7% to $148.9 billion as of Dec. 31. Despite slowing 1.3 percentage points year-over-year, new auto loans were the only loan product for which credit unions reported double-digit growth. Used auto loans expanded 9.1% in 2018. In total, auto loan balances increased 10.1% year-over-year to $369.8 billion as of Dec. 31, 2017.

Since 2008, the share of the credit union loan portfolio held by auto loans, both new and used, has increased 4.0 percentage points to 35.0% at year-end 2018. During this time, credit unions’ market share for auto financing has grown from 16.1% to 20.5%.

Indirect balances at credit unions, which consist largely of auto loans, increased 14.3% annually to $223.6 billion as of Dec. 31. However, as new and used auto loan production at credit unions has slowed, so, too, has the rate at which credit unions originate auto loans through third parties. The 14.4% growth represents a decrease of 3.5 percentage points from year-end 2017.

Although auto lending is an area of credit union expertise, the challenge of deepening relationships with indirect members coupled with higher indirect balances and increased margin pressures has led many credit unions to explore different avenues for auto loan origination, says Taft.

LOAN COMPOSITION

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

The share of the loan portfolio held by total real estate has decreased in the past 10 years; however, first mortgages have strengthened their hold of the portfolio. They’re up 4.1 percentage points since 2008.

LOAN GROWTH BY PRODUCT

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

Total loan growth decelerated 97 basis points year-over-year but remained relatively robust at 9.0%.

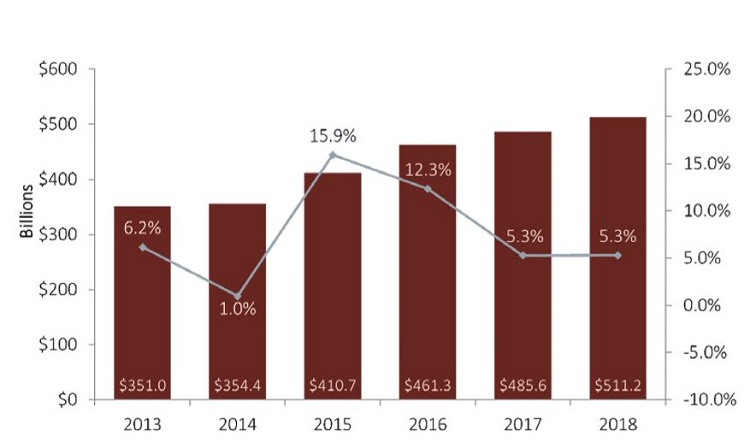

Loan Originations

Total loan originations expanded 5.3% year-over-year to $511.2 billion as of Dec. 31. This is 2 basis points faster than year-end 2017. Driving that growth was consumer loan originations, which were up 8.1% year-over-year to $332.4 billion. The $25.0 billion expansion in this segment accounted for 97.7% of the change in total credit union originations during the 2018 calendar year.

YTD LOAN ORIGINATIONS AND ANNUAL GROWTH

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

Fueled by a strong demand for consumer loans, total originations grew 5.3% year-over-year.

At $139.2 billion, first mortgages made up 27.2% of total loan originations in 2018. However, first mortgage originations contracted 1.2% year-over-year, the only product to do so. This drop could be a reflection of the increased price of mortgages. According to the Federal Reserve of St. Louis, the average rate for a 30-year fixed-rate mortgage was up 86 basis points annually to 4.8% by the end of the year. Since then, rates have trended down and are now close to early 2018 levels.

Mortgage loans were more expensive for the consumer, and even though new home sales slowed in the second half of the year, housing debt continued to climb, Taft says. At $9.5 trillion, national housing debt neared pre-recession levels in the fourth quarter.

Interest rates directly influence the mortgage origination portfolio at credit unions. For example, when the average rate for a 30-year fixed-rate mortgage hit a six-year year-end low of 3.8% in the fourth quarter of 2016, fixed-rate mortgages comprised 70.9% of the mortgage origination portfolio at U.S. credit unions. Balloon and hybrid and adjustable-rate products made up the remaining 19.3% and 9.8%, respectively.

But as interest rates rise, consumers tend to move away from fixed-rate products and toward adjustable ones, which offer lower introductory rates.

Interest rates increased four times in 2018. Consequently, originations for fixed-rate mortgages contracted 4.8%; however, they still accounted for 63.6% of first mortgage originations. Originations for adjustable-rate mortgages as well as balloon and hybrid products expanded 5.7% and 6.1%, respectively. Balloon and hybrid originations reached $34.0 billion at year-end and accounted for 24.4% of all first mortgage originations. With $16.7 billion, originations for adjustable rate products comprised the remaining 12.0%.

In the current economic climate with higher interest rates, improved asset quality, and members moving toward adjustable-rate products credit unions are finding it beneficial to portfolio mortgage loans to alleviate interest rate risk. Thus, first mortgage sales to the secondary market decreased 6.7% annually to $46.1 billion. Credit unions sold 33.1% of their first mortgage originations in 2018, 2.0 percentage points below 2017.

Market Share

Credit unions have increased their market share across all major loan products in the past 10 years. Their strongest foothold is in the auto market, where cooperatives finance more than one in five 20.5%, to be exact auto loans nationwide, according to data provided by Experian Automotive. Auto loan market share for credit unions has increased 4.4 percentage points in the past 10 years. As credit unions slow down their indirect lending, they will need to look to pricing strategies and member services to remain competitive.

The industry’s share of first mortgage lending has likewise expanded, 3.6 percentage points in the past 10 years. By the end of 2018, credit unions financed 8.3% of mortgage loans nationwide. Although first mortgage originations were down 1.1% since the fourth quarter of 2017, market share was up 6 basis points. According to the Mortgage Bankers Association, mortgage originations in the larger financial services industry decreased 3.9% in 2018. Credit unions have been able to alleviate the effects, to an extent, of shrinking origination trends and improve their market share position.

Credit card market share for credit unions has also expanded since the Great Recession. It was up 2.7 percentage points to 6.0% in the fourth quarter. In the past year, banks and credit unions have both expanded credit card market share and squeezed out finance companies. Credit unions increased their market share 29 basis points year-over year, whereas banks expanded theirs 1.4 percentage points. Revolving credit balances at other finance companies have shrunk since the recession, contracting 57.1% in the past decade to $26.5 billion at year-end 2018.

As credit unions work to become the primary financial institution for members, rather than an institution for one-off loans, they need to continue to focus on sound underwriting and a long-term view of relationships, Johnson says.

MARKET SHARE BY PRODUCT

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

Since the Great Recession, credit unions have increased market share across all major lending products.

Asset Quality

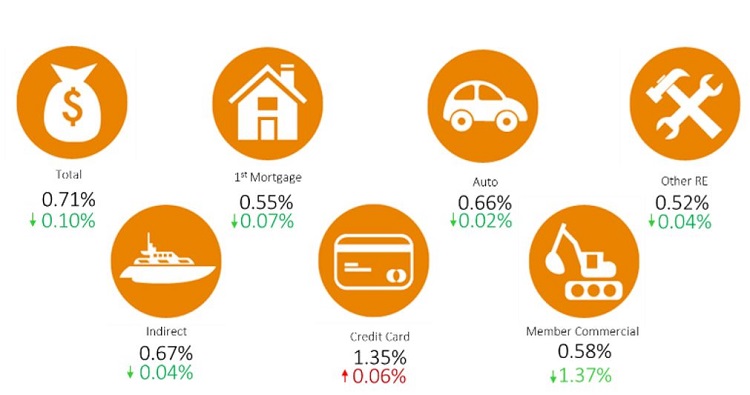

Despite strong lending activity, total delinquency at U.S. credit unions has improved. It fell 10 basis points year-over-year to 0.71%, the lowest year-end level in 12 years. Save a 2-basis-point increase in 2016, loan delinquency at credit unions has decreased every year-end since 2010. In 2018, delinquency improved across all loan products except credit cards.

Credit unions reported the lowest delinquency of any loan type in real estate loans. First mortgage delinquency fell 7 basis points year-over-year to 0.55%. That’s 1.7 percentage points lower than the year-end post-recession high reported in 2010. Other real estate delinquency improved 4 basis points to 0.52% as of Dec. 31.

Credit unions reported the largest delinquency improvements in commercial loans for members. Those decreased 1.4 percentage points year-over-year to 0.59%. Notably, in 2018, the NCUA shuttered two credit unions that struggled to recover from exorbitant delinquency in taxi medallion loans and sold a large percentage of the impaired loans. This heavily diminished the impact of delinquencies in the overall commercial portfolio and led to better asset quality in the loan segment.

Year-end auto delinquency improved 2 basis points year-over-year to 0.66%. Auto delinquency has remained within a 10-basis-point window since credit unions began reporting it in 2013. Although there have been fears of an impending auto bubble in the past couple of years, this segment of the portfolio has turned out the steadiest delinquency levels of any loan product.

Despite the good news across the portfolio, one segment to monitor in the coming quarters is credit cards. Delinquency for this loan product was up 6 basis points year-over-year to 1.35%. In 2018, credit unions increased credit card lines at a faster clip than members used that credit 8.9% versus 7.5%. As a result, credit card utilization was down 40 basis points to 31.7% as of Dec. 31. Unfunded commitments were up 9.5% year-over-year to $134.2 billion. Unused lines increase a credit union’s exposure to delinquency risk by giving members the opportunity to take a larger unsecured loan in isolated circumstances.

DELINQUENCY AND ANNUAL CHANGE

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

Credit union delinquency reached its lowest year-end level since 2006.

Investments

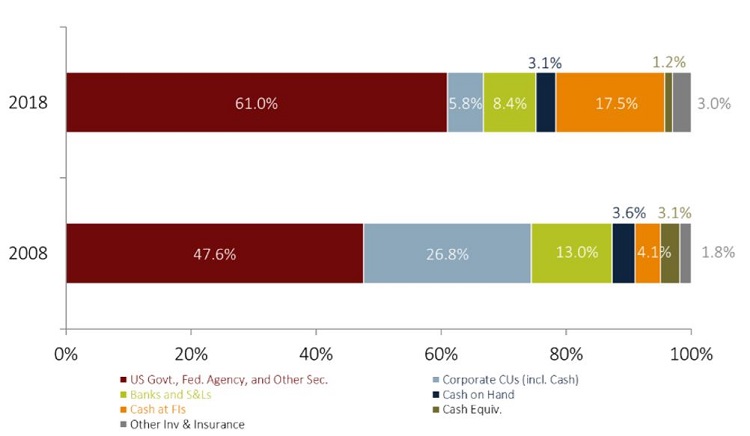

At year-end 2018, credit unions held $350.6 billion in cash and investments, down 4.1% from the $365.7 billion in 2017. As loan growth remains strong and deposit growth lags, institutions with tightening liquidity are rolling off investments and using that cash to fund loans.

The largest change in the investment portfolio since the Great Recession has been the drawing down of cash at corporate credit unions. In 2008, that segment made up 26.8% of credit union investments. Since then, the corporate system has consolidated and the Federal Reserve has paid near market rate on excess reserves. Thus, credit unions have redirected their investments. As of yearend 2018, credit unions placed just 5.8% of their cash investments at a corporate credit union; they placed 61.0% with a federal agency.

INVESTMENT COMPOSITION

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

Since the Great Recession, the share of total investments placed at a corporate credit union is down 21.0 percentage points.

Today, credit unions place the majority of their investments in federal agency securities. At year-end 2018, 60.9% of all credit union investments fell into this category, which includes available-for-sale securities, government obligations, and agency debt instruments among others. At $213.8 billion, the amount credit unions have invested in federal agencies was down 1.7% year-over-year. In the final quarter of the year, credit union federal agency securities contracted 29 basis points. The largest decrease of any product was in bank notes. At $29.4 billion, investments there were down 14.2% year-over-year and 5.7% since the third quarter. However, these investments still comprise the third-largest share, 8.4%, of the credit union investment portfolio.

Balances have declined versus year-end 2017 in every maturity segment across the portfolio except for cash. Cash and equivalents expanded 1.0% quarter-over-quarter, to $93.7 billion, and their share of the investment portfolio was up 42 basis points to 26.7% as of Dec. 31. Investment balances maturing in fewer than three years was down 23 basis points since the third quarter of 2018; those maturing in more than three years was down 2.6 percentage points over the same time. In the current interest rate climate, investment portfolios at credit unions are getting shorter. The weighted average life for the total investment portfolio was down 2 basis points since Sept. 30 to 2.08 years.

Balance Sheet: Liabilities

-

Share certificate growth in 2018 was more than double the rate in 2017.

-

The loan-to-share ratio reached an all-time high, 85.5%, in the fourth quarter of 2018.

-

Credit unions shifted to a negative net liquidity position in final three quarters of 2018.

The Federal Reserve raised interest rates four times in 2018, and despite walking back its projections for hikes in 2019, deposit competition is heating up across the financial services industry. Loan growth at credit unions has outpaced share growth for the past 23 quarters. Fourth quarter stock market performance, however, might lead some members to return to the safety of regular share accounts in the near future. Still, the loan-to-share ratio creeps higher and credit unions continue to feel liquidity pressures.

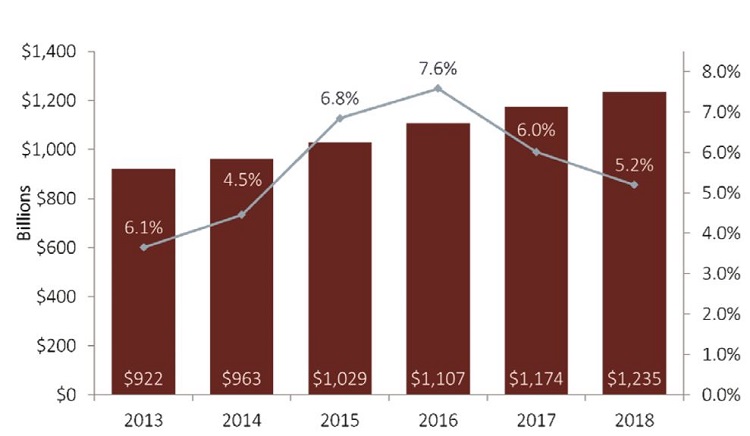

Shares

Total share balances rose 5.2% year-over-year to $1.2 trillion at year-end 2018. This marked the second consecutive year of decelerating share growth. Additionally, share growth continued to lag behind loan growth, increasing liquidity pressures across the industry.

TOTAL SHARES AND ANNUAL GROWTH

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

Share growth at credit unions has slowed at year-end for the past two years.

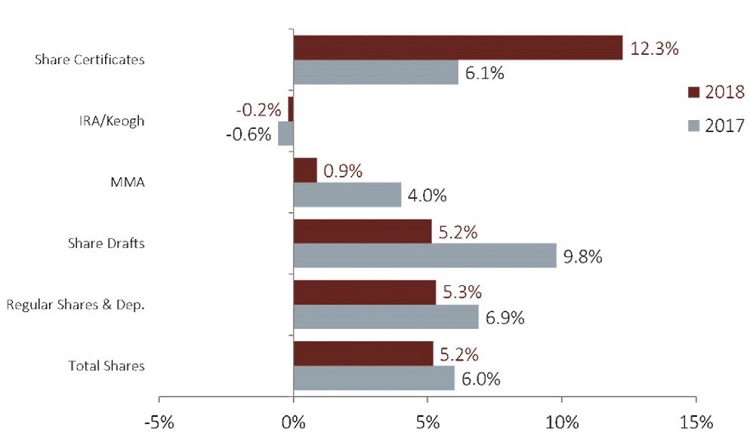

Credit unions did report accelerating growth in share certificates as members looked to take advantage of interest-bearing accounts in the rising rate environment. Certificates have proven to be an important liquidity source that doesn’t require a credit union to reprice its entire portfolio although across the industry, 3,193 credit unions have raised certificate rates since Dec. 31, 2017.

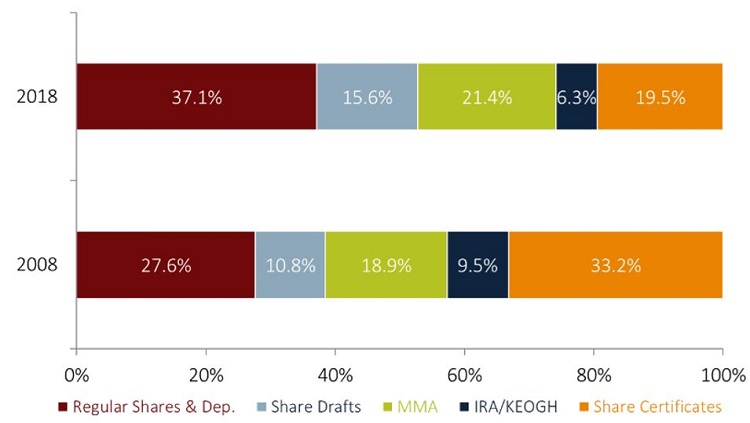

Certificate balances grew 12.3% year-over-year to $240.6 billion that’s more than double the 6.1% rate credit unions reported one year ago. However, certificates still comprise a far smaller percentage of the overall portfolio than they did at the onset of the financial crisis. In 2008, 33.2% of all credit union deposits the largest portion of the share portfolio were certificates. At the end of 2018, certificates made up 19.5% of all deposits at credit unions.

Today, regular shares and deposits comprise the largest portion of the share portfolio 37.1% as of Dec. 31. Regular share balances grew 5.2% in 2018 to $458.5 billion at year-end and have increased their share of the portfolio 9.5 percentage points since 2008. Share draft balances increased 5.2% annually to $192.8 billion at year-end. They’ve also grown in size relative to other segments their share of the portfolio is up 4.8 percentage points in the past 10 years to 15.6%.

All core deposits which includes regular shares, share drafts, and money market shares together comprised 74.2% of the total share portfolio. Considered sticky deposits because they often lead to deeper, longer lasting member relationships, these products made up only 57.3% of the portfolio in 2008. Since the onset of the recession, core deposits have accounted for 95.7% of growth in the overall share portfolio.

SHARE GROWTH BY PRODUCT

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

Share certificate growth more than doubled in the past year and balances expanded 12.3% in 2018 to $240.6 billion.

SHARE COMPOSITION

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

Although share certificates were the only product with accelerating growth, they made up a lower percentage of the portfolio than they did in 2008.

Liquidity

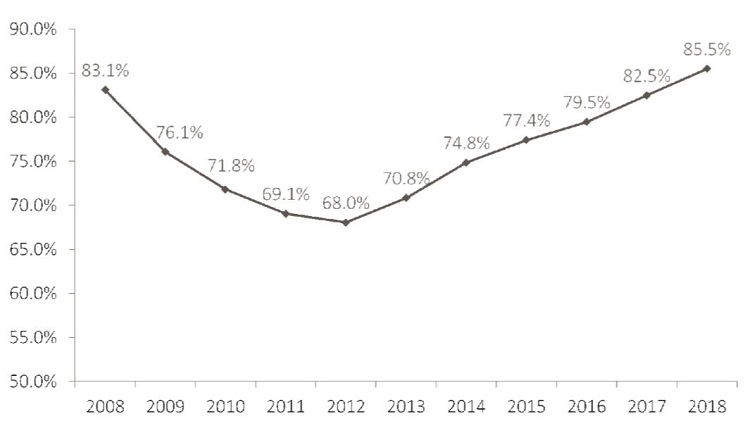

Tightening liquidity has been on the radar of more executives for the past few years, Taft says. With a rising loan-to-share ratio, credit unions have found ways, such as liquidating investments and selling loans, to fund loan demand.

The fourth quarter marked the 19th consecutive quarter that the loan-to-share ratio increased. The ratio has increased 3.0 percentage points year-over-year to 85.5% as of Dec. 31, 2018. That’s up 17.5 percentage points from a fourth quarter low in 2012.

Notably, there is a clear correlation between asset size and loan-to-share levels. The average loan-to-share ratio at credit unions with more than $1 billion in assets was 89.2% in the fourth quarter. By contrast, cooperatives with less than $100 million in assets reported a loan-to-share ratio of 65.1%.

LOAN-TO-SHARE RATIO

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

At 85.5%, the loan-to-share ratio at U.S. credit unions is the highest it has ever been.

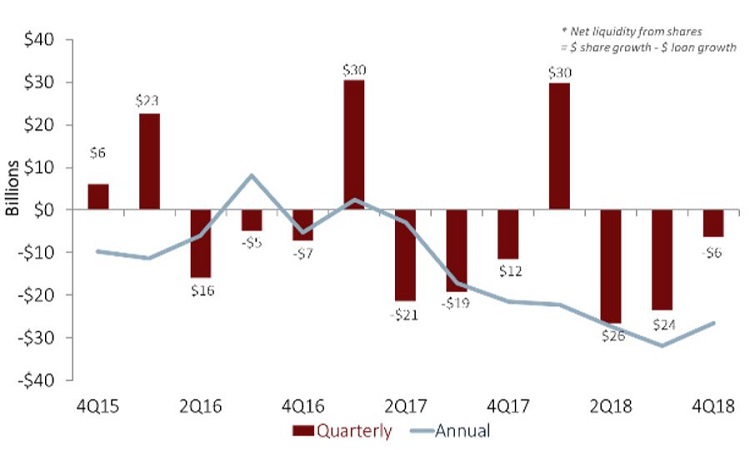

Whereas the loan-to-share ratio paints a general picture of the industry’s liquidity, the net liquidity change which measures the net difference between annual loan outflows and deposit inflows shows how credit unions have managed liquidity through the year.

Deposit flows tend to peak in the first quarter of the year, and credit unions use that gained liquidity to fund loan demand through the rest of the year. As of Dec. 31, 2018, the net liquidity change decreased $6.1 billion quarter-over-quarter and $26.4 billion year-over-year. As a result, during 2018, credit unions reported increased liquidity only in the first quarter.

NET LIQUIDITY CHANGE

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

In 2018, the net liquidity position for credit unions was positive in the first quarter only.

Fourth quarter stock market dynamics and slowing interest rate hikes might lead members to return to insured deposit accounts, Taft says. Although loan demand remained robust through 2018, this dynamic will hopefully ease liquidity pressures in the industry today.

Income Statement

-

Total revenue was up 12.8% year-over-year at U.S. credit unions.

-

The net interest margin gained 12 basis point year-over-year. It closed the year just 2 basis points lower than the operating expense ratio.

-

Net income increased 25.2% in 2018 and drove up ROA 14 basis points year-over-year.

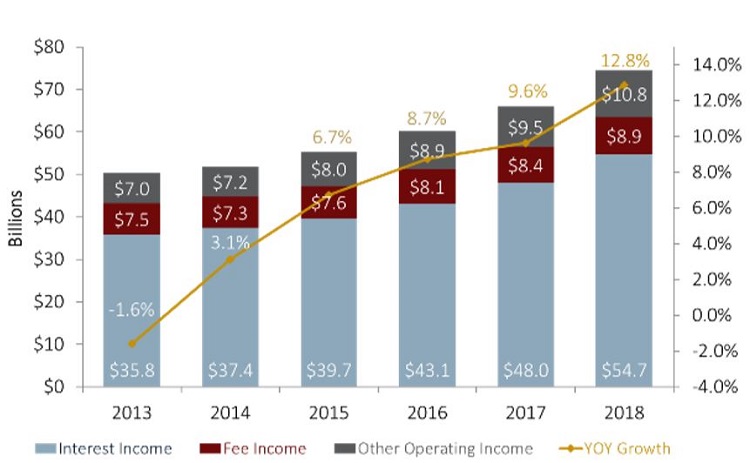

Total revenue in 2018 for U.S. credit unions grew 12.8% to $74.4 billion, an acceleration of 3.2 percentage points from 2017. Annual income has increased 37.4%, or $20.2 billion, since the Great Recession. Largely a result of rising loan demand and interest rate trends, the amount of income generated at credit unions has expanded throughout 2018.

Buoyed by interest rate hikes, interest income rose 13.9% year-over-year to $54.7 billion at year-end 2018. Interest income, which consists of income from investments and loans, comprised 73.5% of credit union revenue. The Federal Reserve issued four rate hikes throughout the year, which subsequently pushed up interest rates on both sides of the balance sheet. Gaining more per dollar loaned and invested, loan income (less interest refunded) at credit unions in 2018 increased 13.1% annually to $47.6 billion and investment income increased 20.3% to $7.1 billion.

TOTAL REVENUE AND ANNUAL GROWTH

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

Interest income, which makes up 73.5% of total income at U.S. credit unions, increased 13.9% year-over-year in 2018.

Non-interest income, primarily fee income and other operating income, accounted for the remaining 26.5% of credit union revenue. Total non-interest income reached $20.0 billion, 9.4% above 2017 year-end levels. Fee income in 2018 increased 5.7% to $8.9 billion. Other operating income increased at the fastest rate, 14.1%, of any non-interest income component and reached $10.8 billion. Other operating income, propped up by the NCUSIF rebates, made up 14.6% of total revenue at U.S. credit unions.

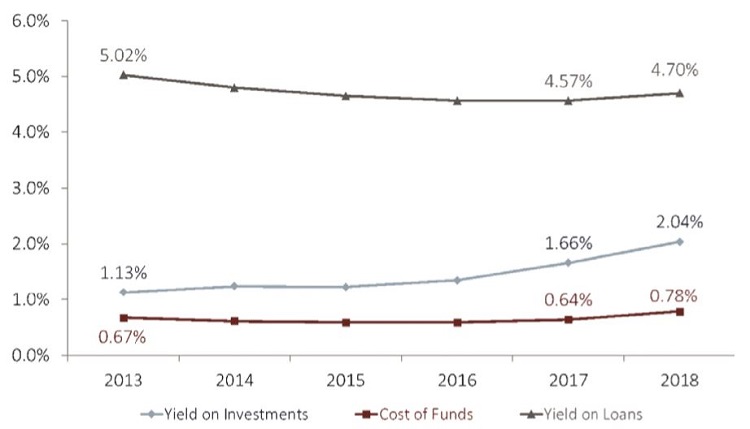

Credit unions reported smaller balance declines in short-term investments those maturing in fewer than three years than in longer segments. Credit unions can reinvest shorter investments at a faster rate than longer ones, and in a rising rate environment, these investments are constantly repriced at higher rates, offering higher yield. Additionally, the front end of the yield curve has increased, which has flattened the overall curve and made short-term investments more profitable. Looking ahead to 2019, as the Fed moves away from planned rate hikes for the remainder of the year, the yield curve might readjust and bring back relative value to longer maturity products.

Total yield on investments was up 38 basis points since year-end 2017 to 2.04% as of Dec. 31, 2018. Yield on loans and cost of funds both increased in relative lockstep, up 13 and 14 basis points over the year to 4.71% and 0.78%, respectively.

YIELD ANALYSIS

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

Yield on loans and cost of funds increased 13 and 14 basis points, respectively, from year-end 2017. Yield on investments, meanwhile, expanded 38 basis points.

In 2018, the net interest margin at U.S. credit unions increased 12 basis points to 3.13%. The operating expense ratio also expanded during the year and was up 5 basis points to 3.15%. With the net interest margin growing at a faster rate than the operating expense ratio, the gap between the two metrics has shrunk to just 2 basis points. For comparison, in 2013, the gap was 35 basis points.

In practical terms, a nearly identical net interest margin and operating expense ratio indicates that credit unions are almost covering their operating expenses through their interest margins. Consequently, net income expanded 24.9% from the fourth quarter of 2017 to $13.1 billion in the fourth quarter of 2018. Return on assets grew 14 basis points to 0.92%.

ROA

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.18

Callahan Associates | CreditUnions.com

ROA was up 14 basis points on the back of a 24.9% net income expansion.

In 2018, credit unions made $7.5 billion in dividend payments, which equates to 11.3% of total income. On average, credit unions paid every credit union member $64 in the form of dividends. That’s up $13 from the year prior. It all goes to show that, first and foremost, cooperatives are working to return value to their members.

All things considered, 2018 was a great year for financial institutions, particularly credit unions, Johnson says. As cooperatives look forward to 2019, they must stay in tune with both macro and local trends as they plan to maximize value to and services for their members.

This article appeared originally in Credit Union Strategy Performance. Read More Today.