Top-Level Takeaways

- Digital tools and affordable platforms lower the accessibility barriers that often prevent members from starting an estate plan.

- Financial literacy programming and one-on-one coaching help members overcome the discomfort of talking about death, inheritance, and financial planning.

- Multi-generational banking under one institution benefits families, too, especially during transitions for caregivers.

It’s not called the Great Wealth Transfer for nothing.

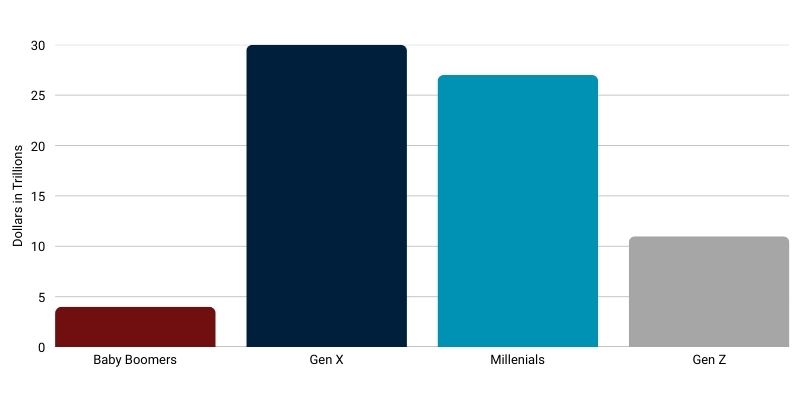

According to research and consulting firm Cerulli Associates, $124 trillion in assets is set to shift hands by 2048. The lion’s share of that — as much as 81% — will flow from the Silent Generation and baby boomers to, mostly, Gen X and millennial heirs.

Tom Montilli, chief operating officer at Harvard Federal Credit Union ($1.2B, Cambridge, MA), says it’s a major life change set to impact members regardless of which side of it they’re on.

“We see a lot of responsibility in making sure our members are financially healthy and prepared for these major life events,” Montilli says. “That’s where we know the greatest need will be over the next decade, and we want to make sure we’re well-positioned to help them through it.”

There’s a common misconception that wealth transfer matters primarily when dealing with significant assets. According to data from the Federal Reserve, the average inheritance in the United States is $46,000 to $58,000 per household; however, large, wealthy estates heavily skew this figure. In reality, 70% to 80% of U.S. households never receive an inheritance. For households that do, the amount is often quite modest, with the bottom 50% averaging less than $10,000.

Still, according to Montilli, that money matters.

“Any inheritance deserves care and planning,” he says. “Something is always better than nothing.”

ESTIMATED WEALTH INHERITANCE THROUGH 2035

FOR U.S. HOUSEHOLDS | DATA AS OF 2023

SOURCE: CERULLI ASSOCIATES, U.S. CENSUS BUREAU, IRS, SOCIAL SECURITY ADMINISTRATION

What Keeps People From Making A Plan?

When it comes to estate planning, some communication is better than nothing, too. But that’s not happening.

A Fidelity Investment study released in 2025 concluded that a full 35% of parents 55 or older don’t want their children to know how much they’ll get. A 2024 Catalyst Advisory’s study estimates only 14% of American adults have had detailed, meaningful conversations about inheritance; 36% have never discussed it at all.

“Families don’t like talking about death or money, and combining the two is especially uncomfortable,” Montilli says. “There’s also the sense that it feels overwhelming or complex just to get started, and sometimes there’s a false sense of security like maybe someone else has taken care of it.”

Perceived complexity and stigma often prevent members from taking the first step, but a lack of dialogue can raise the risk of damaged relationships, financial confusion, and legal disputes over assets.

“They see this monumental task ahead of them, but even starting with basics like a power of attorney helps tremendously down the road,” Montilli says.

Ditching The Traditional For Digital

A few years ago, Harvard FCU addressed some of these barriers through a partnership with Gentreo, an online estate-planning platform founded in part by a Harvard alumni. The service helps users create, manage, and securely store the legal documents needed to organize their affairs. Instead of working directly with an attorney, users complete guided online questionnaires that generate legally valid estate-planning documents tailored to their them.

“The cost model allowed us to subsidize it for many members,” Montilli says. “Even at full price with the credit union discount, it’s about $100 a year, but depending on the relationship, that could be $50 or completely free. It was about making this affordable and lowering that barrier to entry by keeping things simple.”

Harvard FCU continuously promotes this service to its members. There was strong adoption in the beginning, but Montilli says there’s still a long ways to go.

“We want to do more through education and communications to help normalize the conversation and give people guidance on how to start the process,” he says.

Today, Harvard FCU’s partnership with Gentreo extends beyond its digital vault to in-person education resources. The credit union’s community engagement team offers several webinars and workshops about estate planning in general as well as what tools are available and how to use them.

Montilli says the credit union typically times these events around major holidays, when multiple generations are more likely to come together.

Expanding Investment And Advisory Services

Another key piece of Harvard FCU’s wealth transfer strategy is personalized investment services, which it offers through a broker-dealer partnership. Members can sign up for appointments both in-branch or through Zoom.

“With many large investment firms, if you don’t have a million dollars in invested assets, it’s hard to get true one-on-one attention or guidance,” Montilli says. “Again, our goal is to make these services accessible to all members. We believe someone with a $50,000 inheritance deserves the same care and attention.”

The chief operating officer says it’s important members know they don’t have to act too quickly. Priority No. 1 is simply securing the money. From there, advisors encourage them to take a breath and wait until they’re in a less emotionally charged place.

“That’s when you make better decisions,” Montilli says. “There’s no rush, but it is important to start.”

Connections For The Long-Term

CU QUICK FACTS

CU QUICK FACTS

HARVARD FCU

HQ: Cambridge, MA

ASSETS: $ 1.2B

MEMBERS: 58,391

BRANCHES: 6

EMPLOYEES: 148

NET WORTH: 8.7%

ROA: 0.29%

With a growing number of families set to experience this shift in the coming years, Montilli says credit unions are in the exceptional position to “right-size” traditional estate planning so any member can benefit.

“This is where credit unions have always been strong: providing personal service and one-on-one guidance regardless of affluence,” he says.

An increasingly top-of-mind focus at Harvard FCU is encouraging multiple generations to bank together within the same institution. There are clear balance-sheet benefits to this, but it also means easier financial oversight, shared account access, and smoother transitions for caregivers. Montilli says the goal is to establish long-term trust.

“One advantage of being not-for-profit is that we don’t have to look at these conversations through a sales lens or quarterly quotas,” he says. “We’re thinking about relationships that span decades.”