Top-Level Takeaways

-

Patelco and Workers are building their reserves against loan losses as a hedge against the risk of increased loan losses in the face of COVID-19.

-

Both credit unions expect the pandemic’s economic impact to be sharper next year after deferrals are several months a thing of the past.

Patelco Credit Union ($7.5B, Dublin CA) is now reserving against loan losses at three times the rate it had planned going into this year, but, of course, a pandemic hadn’t arrived on U.S. soil when the credit union set that budget.

The big California cooperative is not alone in putting aside cash against the risk of delinquencies that could turn into foreclosures, repossessions, and charge-offs in the wake of COVID-19.

Three time zones away, Workers Credit Union ($1.9B, Fitchburg, MA) has doubled how much it’s putting aside compared to last year. It has also deferred 10% to 12% of major segments of its lending portfolio but still recorded a delinquency rate jump to 1.47% in the first quarter.

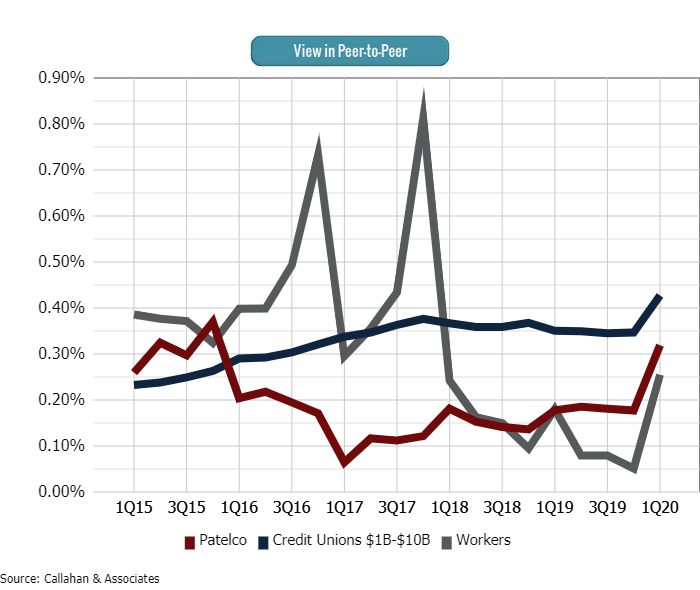

PROVISION FOR LOAN LOSS/AVERAGE ASSETS

DATA AS OF 03.31.20

Callahan & Associates |CreditUnions.com

The ratio of provision for loan losses to average assets for Workers and Patelco credit unions were both lower than the average for the 323 credit unions of $1 billion or more in assets in the first quarter.

Tripling Down After Modeling Scenarios

We entered the year believing adding $1.1 million per month [to the provision for loan losses] would be sufficient, says Susan Gruber, Patelco’s chief financial officer.But we have now raised that to $3.4 million per month based on in-depth scenario and loan modeling we have done for the rest of 2020 and 2021.

Susan Gruber, Chief Financial Officer, Patelco Credit Union

It’s all because of the economic fallout of the pandemic, she continues.California and the nation have been badly hurt by job losses, and we believe credit losses will follow job losses.

At the end of the first quarter, Patelco had $5.9 million in PLL on its books. Three months later, Gruber says, the cooperative has deferred 881 mortgages for $318 million and 7,936 auto loans for $174 million, approximately 12% of each of those portfolios.

It has deferred another 4,637 consumer loans for $37 million, or approximately 10% of that book, as well as $164 million in member business loans, comprising 38 loans and 35% of that portfolio, which are largely in participations.

These are true deferrals, where we put the payment on the back end of the loan, Gruber says.The most common was three months. We took a we’re here to help’ approach with no questions asked, but any renewals have to be hardship based.

Deferrals And Forbearances Can’t Go On Forever

Workers had $812,775 in PLL on its books at the end of the first quarter and has since added enough to double where it was last year as a percentage of its assets.

The cooperative has just crossed the 2,000 and $30 million mark in deferred consumer loan numbers and balances, respectively, with approximately 200 mortgages worth $40 million in forbearance.

Tim Smith, Chief Financial Officer, Workers Credit Union

What happens nationwide when those millions of deferrals and mortgage forbearances expire is the big question; analytics and gut feeling can only go so far in predicting what will happen then.

That’s the real mystery, says Tim Smith, senior vice president, chief financial officer, and treasurer at Workers.We’re doing some analysis, running scenarios, looking at payment histories, collateral values, employment but it’s not all science because we’re in such uncharted territory.

Smith is among many who see indicators that some borrowers are using deferrals handed out without question by Workers and thousands of other financial institutions to relieve financial stress as the pandemic struck even when they could make their payments.

If I were a young homeowner and given the opportunity to defer mortgage payments for six months and save, I’m not sure I wouldn’t do that, Smith says.You don’t know what’s going to happen next.

Indeed, there’s still a lot of uncertainty in the Bay State credit union’s field of membership in central Massachusetts. Smith says the credit union expects some jobs such as at large employers like the local hospital system to return. But, for others, it’s just too soon to say.

Get Creative With Data Using A Custom Data Scorecard

With credit unions changing their strategies and leaning on industry data to help make these decisions, Callahan is here to help. Request a custom data scorecard and see how your credit union is well positioned and how you can provide value to your members after this crisis.

There will be some percentage who will have problems when their deferrals are over, Smith says.We’re trying to get a better handle on what’s going on while being conservative and preparing for the worst.

State-imposed restrictions against proactively reaching out to members who might be struggling, even if they’re 60 days delinquent, further complicated matters for Workers. But the credit union can start calling again, Smith says, which will help it educate members about what Workers offers rather than relying on them seeing what was available via the website. Financial counseling has been part of the effort all along, and the credit union will consider boosting collections staff if that becomes necessary.

Not Waiting To Fill The GAAP

Smith and Gruber both expect their members and their credit unions to begin feeling the real pain next year. Gruber says stress tests on Patelco’s portfolio indicate its charge-off ratio, now at 30 basis points, will peak at around 100 basis points next year before sliding back down. Armed with that projection, Patelco is taking action now.

With the blessing of our external auditors, we’re front-loading our future losses even though that’s not technically following GAAP, Gruber says.A lot of people are doing a wait-and-see and following GAAP to the letter. In my opinion, this is not a good idea. The losses are going to come. You can’t avoid them if people aren’t employed. That’s why we’re being proactive.

Smith, meanwhile, says he is surprised and encouraged by how many companies in his market have hired employees back and attributes much of that to the Payroll Protection Program.

He also says he expects 2021 to be worse than this year. But, after that, who knows?

We haven’t thought out to 2022, the Workers CFO says.I guess it depends on a second wave and how many companies don’t make it through lockdowns.

As for how bad could it possibly get, Smith won’t wade into those waters.

I won’t predict, Smith says.I wish I knew.