Share, loan, and member growth are three major metrics that help formulate a big picture of a credit union’s performance.

In a third quarter clean sweep, Pioneer Federal Credit Union($438.0M, Mountain Home, ID) topped the leader tables for all three of those measures, besting 343 credit unions in the $250 million to $500 million asset range.

Leaders at the 63-year-old former air base credit union that now serves most of southwest Idaho have relied on upgraded systems and processes to fuel growth. A merger, relationship lending with a twist, a core processing conversion, mobile apps, and some good, old-fashioned asset liability management have underpinned growth as well. And, of course, people make a difference, too.

How Do You Compare?

Callahan clients can click on any of the graphs in the slideshow to visit Peer-to-Peer analytics and compare their credit union’s performance against Pioneer or any peer groups of their choosing.

You need to establish the right chemistry, find the right employees, and then growth should come,says Curt Perry, who joined the credit union in 2002 and became CEO in 2011. Bigger doesnt always lead to better, but better can easily lead to bigger. Do your part to nail down the culture and work atmosphere first, the rest will follow.

Here Perry and his vice president of marketing, Elizabeth Thomas, share a deeper look behind Pioneer FCU’s financial performance numbers.

Click through the tabs below for an in-depth discussion about Pioneers financial performance.

$(‘.collapse’).collapse()

// ]]>

1. Leaders In Member Growth ($250M-$500M)

MEMBER GROWTH

FOR ALL U.S. CREDIT UNIONS $250M-$500M | DATA AS OF 09.30.16

Callahan & Associates | CreditUnions.com

#NameStateTotal Assets (In Millions)Members 3Q16Members 3Q13Member Growth: Past 3 YearsMember Growth: Past 3 Years CAGR1PioneerID$444.350,79831,70760.2%17.0%2AtomicOH$262.142,32226,48659.8%16.9%3Del-OneDE$415.354,52938,68041.0%12.1%4Safe AmericaCA$439.034,44224,98137.9%11.3%5PeoplesRI$450.638,47928,20136.5%10.9%6GuardianAL$375.247,78335,33835.2%10.67UniWyoWY$296.026,07519,37034.6%10.4%8Cornerstone Community FinancialMI$278.227,70920,61034.4%10.4%9Team OneMI$488.647,74635,72533.7%10.2%10FrankenmuthMI$457.735,65226,88732.6%9.9%

Source: Callahan & Associates

A merger in 2015 added a few thousand members and contributed to the momentum already underway at Pioneer Federal Credit Union. New products and services as well as a focus on helping members improve their financial wellness, including their credit scores, all underpin a growing membership roster.

Some credit unions grow by any means necessary for the sake of growth,says CEO Curt Perry. I dont believe in growing to establish bragging rights. We dont offer the highest rates in the market to inflate deposit growth. We dont offer the lowest rates in the market to corner the loan market. We don’t have to.

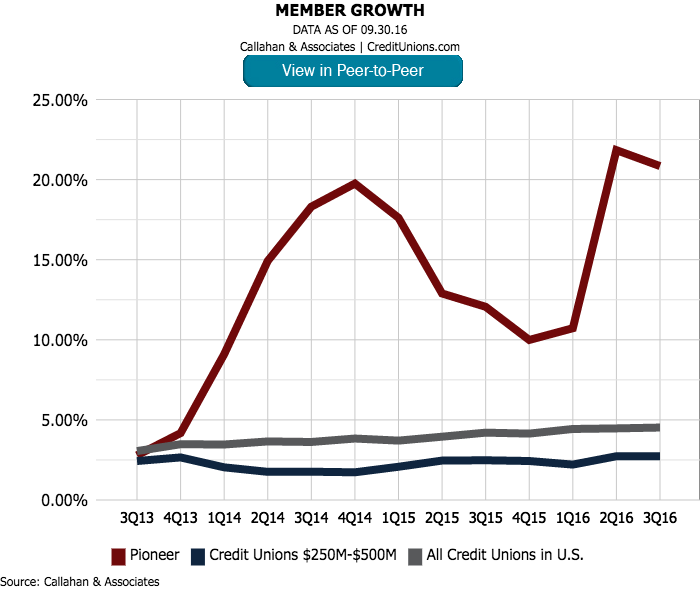

2. Pioneer Member Growth

Pioneer absorbed $15 million, 4,000-member Cornerstone Credit Union in June 2016. Lending, meanwhile, grew through both direct and indirect channels, and the credit union dramatically broadened service options after a core platform conversion in 2012.

With the new core, we were able to put in place some of the programs and systems we had wanted for some time,says Elizabeth Thomas, the vice president of marketing for the 50,000-member cooperative. We could start building a service model that allows our members to be served in a way that works best for them.

That service model includes 14 branches with more on the way, mobile banking complete with bill pay and check deposits, and interactive teller machines that expand personal service hours at many of Pioneer’s drive-throughs to 7 a.m. to 7 p.m. on weekdays and 9 a.m. to 2 p.m. on Saturdays. Members can also apply for loans and new accounts through online and mobile channels.

3. Leaders In Loan Growth ($250M-$500M)

LOAN GROWTH

FOR ALL US CREDIT UNIONS $250M-$500M | DATA AS OF 09.30.16

Callahan & Associates | CreditUnions.com

| # | Name | State | Total Assets (In Millions) | Loans 3Q16 (In Millions) | Loans 3Q 13 (In Millions) | Loan Growth: Past 3 Years | Loan Growth: Past 3 Years CAGR |

|---|---|---|---|---|---|---|---|

| 1 | Pioneer | ID | $444.3 | $354.2 | $157.0 | 125.6% | 31.2% |

| 2 | Glendale Area Schools | CA | $341.5 | $84.7 | $39.4 | 114.8% | 29.0% |

| 3 | Fairfax County | VA | $370.7 | $291.1 | $138.8 | 109.7% | 28.0% |

| 4 | Guardian | AL | $375.2 | $278.3 | $133.2 | 109.0% | 27.8% |

| 5 | SafeAmerica | CA | $439.0 | $395.6 | $189.4 | 108.9% | 27.8% |

| 6 | Sun Community | CA | $407.6 | $293.5 | $149.6 | 96.2% | 25.2% |

| 7 | UNCLE | CA | $355.5 | $244.6 | $127.5 | 91.2% | 24.3% |

| 8 | Dover | DE | $455.4 | $297.6 | $159.4 | 86.7% | 23.1% |

| 9 | IH | OH | $298.3 | $165.5 | $89.0 | 86.0% | 23.0% |

| 10 | Alliance | CA | $410.9 | $336.9 | $197.0 | 71.0% | 19.6% |

Source: Callahan & Associates

We presented an engaging marketing campaign that focused on individual member success stories and promoted our Credit Score Analysis program across many mediums,Thomas says.

The credit-building service helps members consolidate and eliminate debt as well as raise their credit score. And when members qualify for the credit union’s 720 Club, they get better rates that can lead to significant savings.

Community and family relations also contribute to the credit union’s lending success.

Our employees ask friends, family, and members to see if we can lower their monthly payments and raise their credit score,Thomas says.

4. Pioneer Loan Growth

Third-quarter lending in 2014 was up 70% from the year-ago quarter before falling to level with its peer group and then above average again last year. Perry says the 2014 lending surge occurred across the portfolio: RV loans increased 68%, auto loans increased 169%, credit card lending increased by 30%, for example.

We fine-tuned our indirect lending department in 2014, but our growth was not isolated to indirect lending,the Pioneer CEO notes.

5. Leaders In Share Growth ($250M-$500M)

SHARE GROWTH

FOR ALL US CREDIT UNIONS $250M-$500M | DATA AS OF 09.30.16

Callahan & Associates | CreditUnions.com

| # | Name | State | Total Assets (In Millions) | Shares 3Q13 (In Millions) | Shares 3Q16 (In Millions) | Share Growth: Past 3 Years | Share Growth: Past 3 Years CAGR |

|---|---|---|---|---|---|---|---|

| 1 | Pioneer | ID | $444.3 | $256.1 | $403.1 | 57.4% | 16.3% |

| 2 | Frankenmuth | MI | $457.7 | $245.2 | $384.8 | 56.9% | 16.2% |

| 3 | Guardian | AL | $375.2 | $202.0 | $313.0 | 55.0% | 15.7% |

| 4 | Freedom First | VA | $453.0 | $241.0 | $356.8 | 48.0% | 14.0% |

| 5 | Fairfax County | VA | $370.7 | $194.8 | $283.0 | 14.0% | 13.3% |

| 6 | Southwest Airlines | TX | $426.4 | $259.8 | $372.5 | 43.4% | 12.3% |

| 7 | Superior Choice | WI | $352.9 | $214.2 | $303.1 | 41.5% | 12.3% |

| 8 | Partner Colorado | CO | $325.4 | $205.4 | $285.9 | 39.2% | 11.7% |

| 9 | Piedmont Advantage | NC | $327.2 | $202.0 | $279.3 | 38.2% | 11.4% |

| 10 | Family Trust | SC | $442.7 | $254.8 | $352.0 | 38.2% | 11.8% |

Source: Callahan & Associates

Perry says efforts to increase core deposits over the past few years have included instant issue cards, personalized debit and credit cards, programs that round up debit card purchases, reward and youth checking accounts, and self-service conveniences.

Those, along with competitive savings rates, have helped give the Idaho credit union the liquidity needed to sharply grow lending. Pioneer’s loan-to-share ratio is now 88.3%, versus 75.5% for its $250 million to $500 million asset-based peer group and 77.2% for all credit unions nationwide, according to data from Callahan & Associates.

6. Pioneer Share Growth

Asset and liability management strategies came into play as Pioneer worked with share growth dips and spikes, including year-over-year jumps of 35% in second quarter 2015 and 19.5% in third quarter 2016. The latter ranks in the top 5% nationwide regardless of asset class.

7. Pioneer Share Composition

When I took over in 2011, I wasn’t crazy about our balance sheet composition,Perry says. Especially on the deposit side of the house.

At the time, Pioneer held 55% of its deposits in certificates that were five-year obligations locked in at the elevated rates prevailing in 2008 and 2009. That when the credit union entered into a net worth restoration plan with regulators.

By the end of 2014, 32% of our deposits were in certificates, with the rest sitting in core deposits,Perry says. Morphing your deposit mix takes time, especially with long-term certificates.

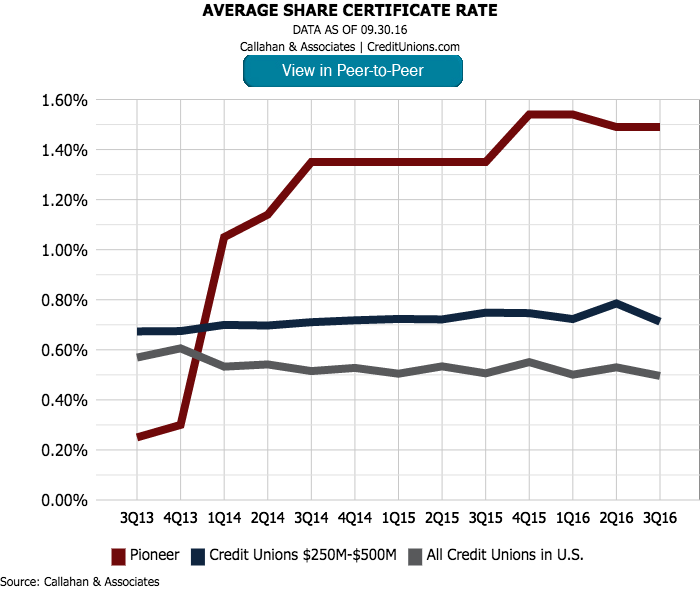

8. Pioneer Share Certificate Rates

The Idaho credit union’s average rate for share certificates was 1.49% in third quarter 2016. That’s more than twice the 0.71% average of its asset-based peer credit unions and nearly three times the 0.50% average for credit unions nationally.

9. Pioneer Share Certificate Growth

It isn’t a secret what our focus has been since 2010,Perry says. Over that period of time we’ve increased our core deposits by $111 million while reducing our certificate balances by $170,000.

At the same time, total dollars in regular shares and checking accounts doubled.

Certificates serve a purpose when it comes to asset-liability management,Perry says. However, you can throw a high rate out there and grow certificates without any effort. When you can grow your core deposits as we’ve done, it shows you’ve strengthened member relationships and trust across the board.