What’s In A Name: Chief Efficiency Officer

Kelli Wisner-Frank serves as the linchpin between finance and innovation at Community Choice Credit Union, aligning automation, smarter processes, and cost discipline to turn front-line

![]() Diana Dykstra, CEO of San Francisco Fire Credit Union ($423m, San Francisco, CA) describes their 2007 strategy for demonstrating the credit union difference – allowing members to set their own rates and create their own accounts.

Diana Dykstra, CEO of San Francisco Fire Credit Union ($423m, San Francisco, CA) describes their 2007 strategy for demonstrating the credit union difference – allowing members to set their own rates and create their own accounts.

Backed by record-setting financials but with low member growth, Pete Sainato, CEO of Justice FCU, is instigating a program of significantly boosting return and value to members.

How Oxford FCU is having success with its’ two-pronged strategy that is attracting younger members and driving up debit card usage.

The fastest growing segment of our country’s population represents an oportunidad importante for credit unions.

Defying the stall in industry growth rates, BECU is growing shares at five times the national average according to First Look data. What is driving their success?

Outbound calling allows a credit union to personalize the point of contact and can be successful at getting members to increase their relationship with the credit union.

BECU grew in assets from $3 billion in 1999 to $5 billion in 2004. One catalyst for this growth: 33 new branches built in retail stores.

University of Wisconsin Credit Union in Madison with $730 million in assets have begun using RSS news feeds to update members on its monthly website content.

Navy Federal Credit Union grew by nearly $3 billion in assets in 2004. Find out what the main drivers were behind their success in 2004.

Many credit unions are growing their lending portfolio through member business lending. The foundation for a successful program is an all-encompassing strategy.

A rethink of closing costs, rate relief, and employer partnerships helped 7 17 Credit Union build an affordable housing mortgage program that works.

Where is mortgage growth coming from right now? This week, CreditUnions.com covers a mix of home equity campaigns, targeted affordability programs, and niche lending strategies that are bringing borrowers back into the market.

Home equity lending is a winning option for credit unions in today’s mortgage environment. Learn how three different shops meet members’ needs.

Manufactured home loans can provide members access to affordable housing, including those in rural areas. Two credit unions share how they approach the niche product.

After a prolonged slowdown, signs of life are returning to mortgage lending. Growth is uneven, with first-time buyers and shifting rate dynamics driving activity in select segments.

The Michigan cooperative keeps everyday payments working and members happy by using a common friction point to build brand loyalty.

How a former Sam’s Club finance leader adapted his member-first mindset to a not-for-profit credit union.

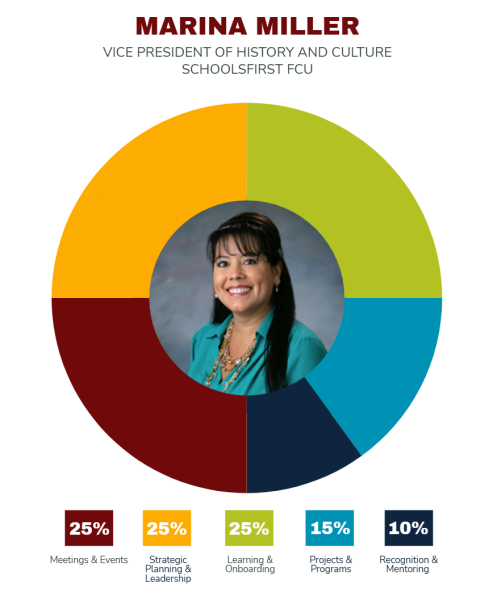

How a novel role instills SchoolsFirst FCU’s future leaders with an appreciation for its past.

Arriba Advisors co-founder Tom Russell explores how credit unions can bridge the gap between a growth mindset and their technical reality.

RKL offers insight, expertise, and experience to help fight off growing threats.