This is part of the Callahan Financial Performance Series. Presented by the analysts at Callahan & Associates, the series helps leaders interpret data to drive smarter decisions and uncover new approaches to measure performance. Callahan clients can access the full version of this article right now on the client portal. Read it today.

Credit unions wrapped the first quarter of 2026 from a position of balance sheet strength despite persistent uncertainty in the broader U.S. economy. Although margins have benefited from favorable rate dynamics, the most durable advantage might be capital itself.

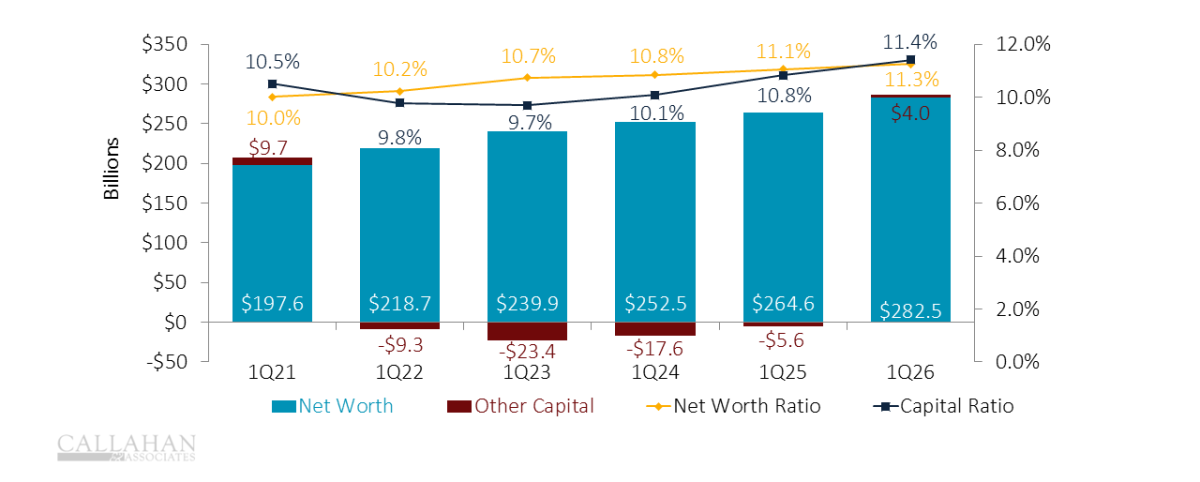

Accumulated earnings and disciplined balance sheet management have pushed net worth and capital ratios to multi year highs — creating flexibility at a time when many households remain under financial pressure.

NET WORTH AND OTHER CAPITAL

FOR U.S. CREDIT UNIONS

SOURCE: CALLAHAN & ASSOCIATES

- Capital ratios are at five year highs, reinforcing credit unions’ ability to absorb volatility while maintaining confidence among regulators, members, and markets. Capital is doing its job as a stabilizer in an uncertain macro environment.

- Strong capital reflects earnings durability, not one‑time gains. Elevated margins and controlled expense growth have steadily flowed into net worth, strengthening the balance sheet quarter after quarter.

- Excess capital creates choice as well as urgency. Although it’s prudent to build a robust buffer, holding capital indefinitely carries opportunity cost. In a prolonged period of uncertainty, the strategic question shifts from preservation to purpose.

- Well‑capitalized credit unions can play offense, using capital to support pricing relief, reinvest in technology and service delivery, or expand access through new products and markets — all without compromising safety and soundness.

How do macro trends influence credit union performance? Interest rates, labor market shifts, inflation, and delinquency trends all influence credit union performance. A free 30-day Peer Suite Premium trial helps leaders benchmark results against national economic indicators like rates, unemployment, and delinquency trends to better interpret performance in broader economic context. Start your 30-day trial.