How’s this for a credit union-friendly demographic? Late 20s, employed and notably underbanked. Then multiply that by millions.

These are the millennials and according to last week’s weekly report from the Brookings Institution, their numbers are being spiked by a just-in-time growth in new immigrant and multi-racial minorities.

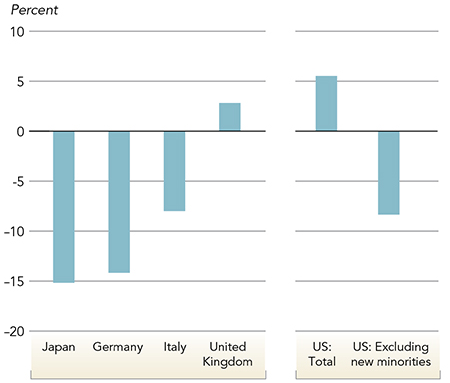

In the report, William Frey, senior fellow at Washington, D.C.-based Brookings, compares the burgeoning generation of young Hispanics, Asians, and multi-racial Americans to stagnant population growth in some other major world markets.

Frey author of the 2014 book Diversity Explosion: How New Racial Demographics Are Remaking America writes, As the management textbooks might say, the growth of the young, new minority population from recent immigration and somewhat higher fertility is providing the country with a just-in-time’ demographic infusion as the largely white U.S. population continues to age.

The Brookings report says that the U.S. working age population is projected to grow more than 5% between 2010 and 2030. Take away new minorities and that would be an 8% decline.

Projected Growth In Labor Force-Age Populations,

Selected Countries, 2010-30

Labor force-age populations defined here as ages 15-64.

Source: United Nations, World Population Prospects: The 2012 Revision

U.S. Census Bureau projections.

Beyond a source of much-needed labor and entrepreneurship, this big group represents both great opportunity and great obligation to the credit union movement, which itself was founded on serving people in very similar circumstances a scant few generations ago.

No other market has the potential that Hispanics and immigrants represent for our future and our relevance, says Pablo DeFilippi, membership director for the National Federation of Community Development Credit Unions in New York.

It’s a market where mission and opportunity come hand in hand, DeFilippi says. It’s also a market that’s financially very underserved, particularly for recent arrivals and first-generation immigrants.

Beyond a source of much-needed labor and entrepreneurship, this big group represents both great opportunity and great obligation to the credit union movement.

The industry has been beating the drum for several years now about the age of the average credit union member and the need to drive that metric down. Serving new Americans could certainly help in that regard, says an industry consultant with a stake in that effort.

The median age for Hispanics is 27, a vast difference from the life stage of the average credit union member today, who’s 48, says Miriam De Dios, president/CEO of the Coopera marketing consultancy out of Iowa.

Next: The Largest Living Generation

The Largest Living Generation

Some demographers have identified 2015 as the year that millennials of all stripes become America’s largest living generation, and the Brookings report makes clear that the immigrant population is one of its largest segments.

But are enough credit unions going beyond lip service? Michael Emancipator, assistant vice president at Callahan Financial Services, isn’t sure. The sheer size of the millennial market should whet the appetite of any credit union executive looking for an opportunity to grow membership, the credit union consultant says.

Although I’ve heard dozens of strategic plans that attempt to draw millennials to the credit union, Emancipator says, I’ve only heard a handful that actually segment the market to recognize their unique needs.

Those needs include providing alternatives to payday lenders, providing access to credit that would be otherwise denied, providing entry into mainstream financial services. And sometimes it involves doing things differently, like Travis Credit Union in northern California is with a program that combines traditional tanda crowdsourcing with formal banking services.

Others simply adjust their underwriting criteria to member realities. Tuscaloosa Credit Union does that with a homeownership program that is helping the Alabama town continue its comeback from a devastating 2011 tornado.

Those needs include providing alternatives to payday lenders, providing access to credit that would be otherwise denied, providing entry into mainstream financial services.

And First Imperial Credit Union near the Mexico border in southern California offers alternative checking accounts and uses work records instead of credit records to price loans, serving as a check cashing and payday lending alternative while driving its own deposit growth.

Credit unions are pulling this off without taking on undue risk, according to Scott Butterfield, a credit union consulting strategist who operates as Your Credit Union Partner.

The Seattle-based consultant points across the country to 15-year-old, $151 million Latino Community Credit Union in Durham, NC. That institution grew loans by an average of 17.71% each year for the past five years with an annual charge-off rate of a scant 0.45% and an average ROA of a healthy 1.35%, Butterfield notes.

Next: Minorities Go Mainstream

Minorities Go Mainstream

Potentially, tens of millions of younger consumers many of whom have avoided mainstream financial institutions because they lack Social Security numbers or come from a generation that distrusts banks will be in a position to consider a mainstream auto, home or small business loan, Butterfield says.

Access to and adoption from this group en masse could be the answer to many credit unions’ millennial prayers, he says.

That said, De Dios at Coopera says it goes beyond appropriate products and services. It’s imperative that credit unions be representative and inclusive of new markets on their boards and in their management teams as well, she says.

Luckily, there’s no better time than the present for credit unions to connect with these growing markets that seek inclusivity from the consumer level to the leadership level, De Dios adds.

But it’s not necessarily easy and for many credit unions, perhaps not even necessary.

The systems and cultural change that’s needed to serve the diversity wave isn’t for everyone, Butterfield says. But I do believe that credit unions who pursue this route successfully will be guaranteeing their longevity for at least another hundred years.