This is part of the Callahan Financial Performance Series. Presented by the analysts at Callahan & Associates, the series helps leaders interpret data to drive smarter decisions and uncover new approaches to measure performance. Callahan clients can access the full version of this article right now on the client portal. Read it today.

As credit union leaders turn their calendars deeper into 2026, the effects of interest rate changes are becoming more important. Rapidly rising rates the past few years have allowed credit unions to reprice their portfolios to a more favorable earnings position.

The structure of a credit union’s earnings model is central to how an institution fares in this changing environment. Credit unions that can capitalize on earnings-model flexibility during times of solid revenue growth typically are better positioned to weather storms in the future.

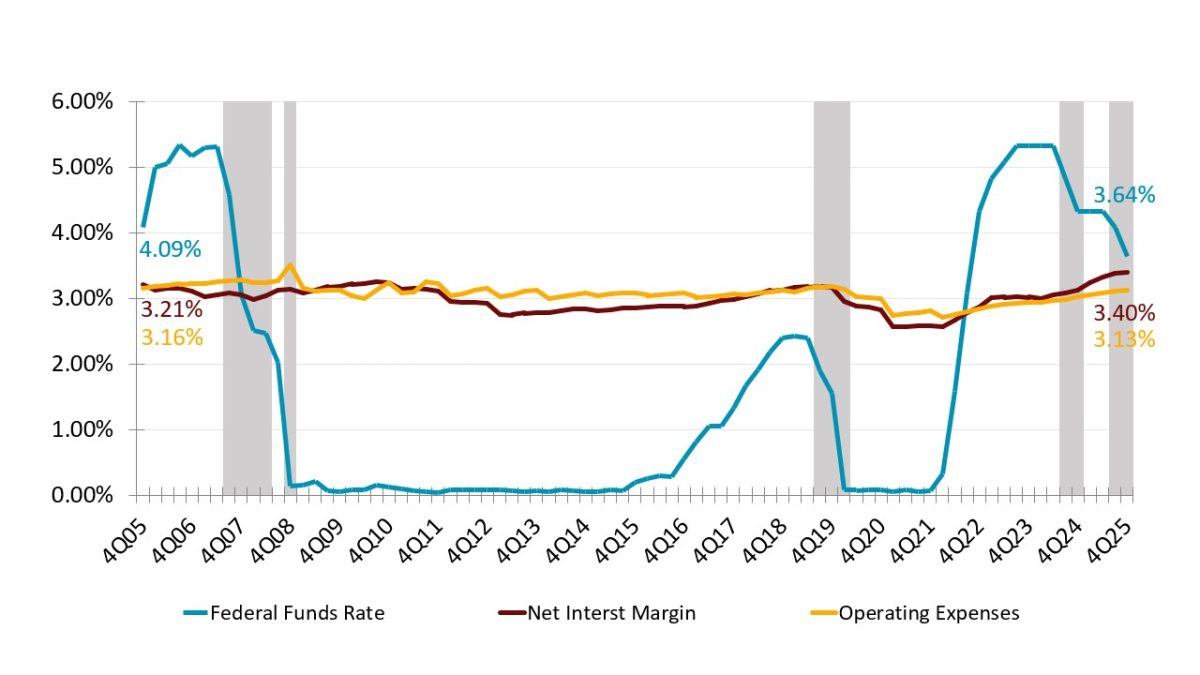

Net Interest Margin

At the center of that transition is the net interest margin. The primary driver of earnings in the past few quarters is also most directly affected by shifting interest rates. At 3.40%, margins remain at the industry’s highest level in the past two decades. In fact, margins outpace the operating expense ratio (as a percentage of average assets) by 27 basis points, continuing the largest and longest sustained gap of the past two decades.

CREDIT UNION MARGINS AND OPERATING COSTS

FOR U.S. CREDIT UNIONS

SOURCE: CALLAHAN & ASSOCIATES

During a downward interest rate cycle, however, loans tend to reprice faster than shares, particularly for credit unions with higher concentrations of variable-rate or shorter duration assets.

Operating Expenses

Operating expenses tend to adjust slowly to external forces, as they’re driven by staffing, branch networks, and technology investments that typically don’t feel the immediate impacts of monetary policy shifts. Historically, operating expense ratios have not declined meaningfully during rate-cut cycles.

During the past few years, operating expense ratios have grown at a remarkably steady rate, generally tracking the pace of inflation nationally, which has been elevated. If margins start to contract, finding efficiency returns on the technical investments of the past few years will grow in importance.

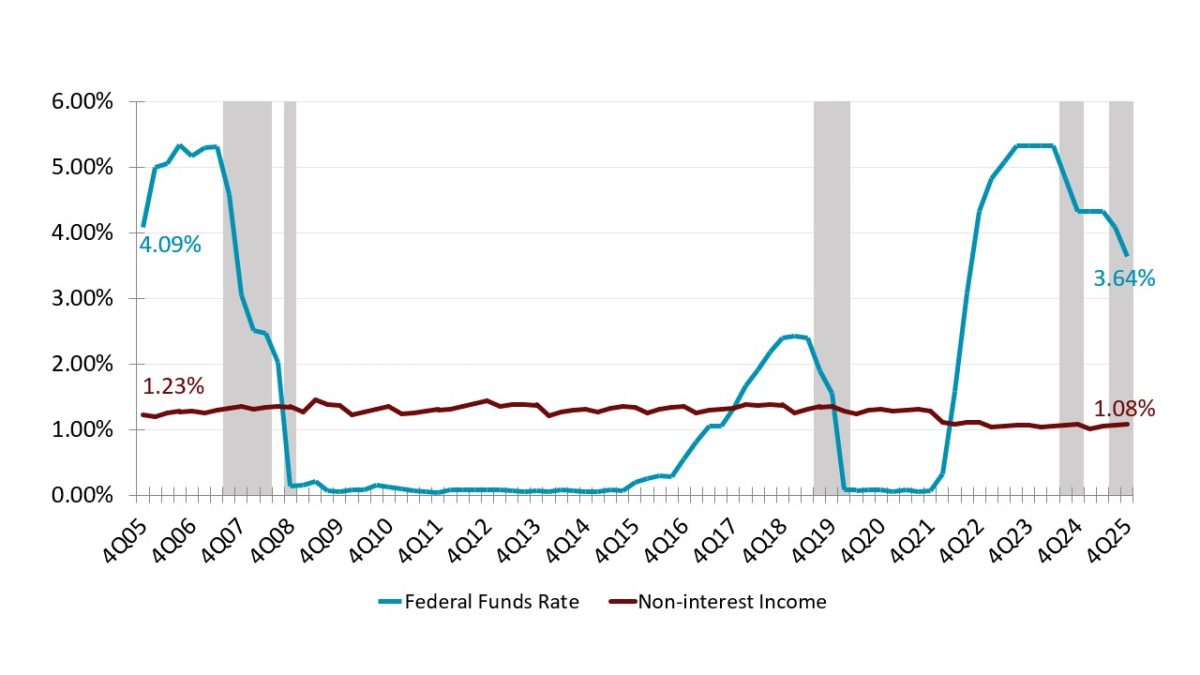

Non-Interest Income

Non-interest income (NII) has steadily declined as a share of average assets in the past several years, most recently falling to 1.08%. As margins diminish, NII re-enters the earnings conversation as a stabilizing force. Unlike the net interest margin, NII is less directly tied to repricing dynamics and more influenced by member behavior, product penetration, and scale, a distinction that matters as earnings stability becomes harder to maintain through rates alone.

NON-INTEREST INCOME

FOR U.S. CREDIT UNIONS

SOURCE: CALLAHAN & ASSOCIATES

Credit unions that face a compressing net interest margin might wish to investigate greater income-stream diversification through CUSOs, interchange, secondary sales, or other routes.

Join Callahan’s Non-Interest Income Survey. Understanding where your non-interest income comes from, and how it compares to peers, is critical. Tap into a unique, non-public dataset built through voluntary data sharing and gain detailed insights that go far beyond what is available in the 5300 Call Report. Learn more today.

Looking forward to the rest of 2026, the earnings conversation ultimately converges on balance sheet flexibility. Credit unions will reshape portfolios in response to falling rates, as lower rates bring opportunities for cheaper financing and refinancing.

The challenge facing credit unions is not unfamiliar, but this environment is where the cooperative model shines — when member focus is no longer a philosophy, but a financial choice.

Ready To Read The Full Story? Callahan clients can access the full version of this article right now on the client portal. Read it today. Not yet a client but looking for expert insights to help you adapt to change, develop your organization’s leaders, and stay at the forefront of industry trends? Connect with our team to learn more.