According to the Federal Reserve’s Quarterly Report on Household Debt and Credit, 16.8 million credit card accounts were opened in the past year.

In the second quarter of 2019, credit card debt made up 6.3% of total household debt that’s 2 basis points more than the same time last year. Credit card lending increased $39 billion to $870 billion, which is the highest it has been since the fourth quarter of 2008.

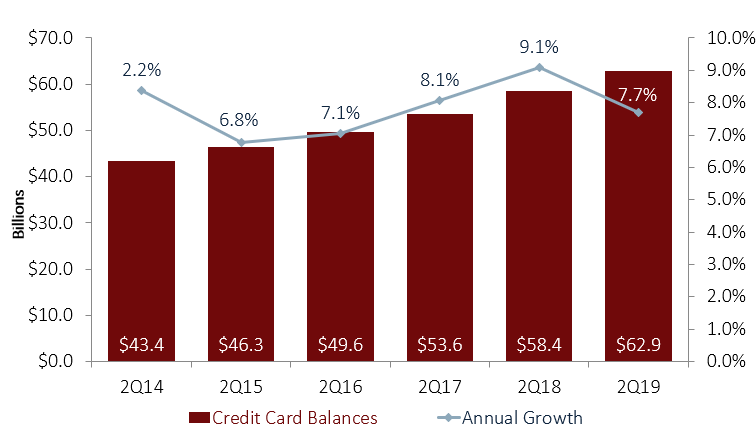

Credit unions held $62.9 billion in unsecured credit card balances at midyear. That’s a $4.7 billion increase in the past 12 months.

CREDIT CARD BALANCE AND GROWTH

FOR U.S. CREDIT UNIONS | DATA AS OF 06.30.19

Callahan & Associates | CreditUnions.com

Credit unions held $62.9 billion in credit card balances as of June 30, 2019.

As of June 30, 62% of U.S. credit unions offered credit card loans to their members, an increase of 87 basis points year-over-year. Credit card balances grew 7.7% and neared $63.0 billion at midyear. Unfunded commitments, however, also rose 9.0% to $129.1 billion as credit unions extended credit faster than members used it.

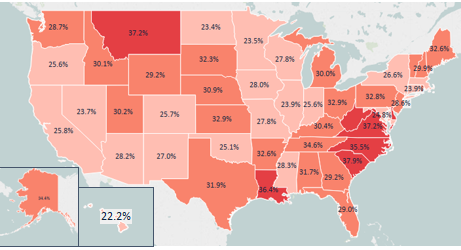

Credit Card Utilization=Outstanding balances/(outstanding balances + unfunded commitments).

Credit card utilization varies across the nation. The industry average as of June 30, 2019, was 30.9%. Credit unions in the NCUA Eastern Region typically report a higher credit card utilization rate. True to form, their midyear average was 33.9%. The NCUA Southern Region followed with an average of 31.7%, and credit unions in the Western Region rounded out the country with an average utilization of 27.1%.

CREDIT CARD UTILIZATION BY STATE

FOR U.S. CREDIT UNIONS | DATA AS OF 06.30.19

Callahan & Associates | CreditUnions.com

Credit card utilization at credit unions varies across the country, but the national average was 30.9% in the second quarter.

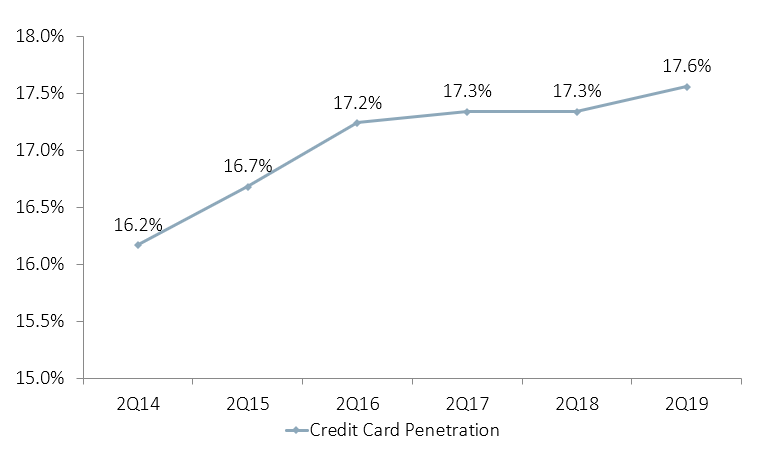

As of June 30, 2019, 17.6% of members nationally held a credit card with their credit union. Credit card penetration has increased 14 basis points in the past year and 1.3 percentage points in the past five. The average credit card balance increased $130 year-over-year to top $2,900 at midyear.

To compete with today’s plethora of credit card issuers, credit unions have invested in technology. For example, many have implemented online services, such as mobile apps and mobile payments, that make managing finances easier. And investments in contactless card services, such as ApplePay, have fostered higher credit card usage.

CREDIT CARD PENETRATION

FOR U.S. CREDIT UNIONS | DATA AS OF 06.30.19

Callahan & Associates | CreditUnions.com

The number of consumers using a credit union credit card has steadily increased in the past five years. It’s up 1.3 percentage points since 2014.

A well-managed credit card program can yield strong results for the loan portfolio however, credit unions must remain vigilant about asset quality.

The credit card delinquency rate as of June 30 was 1.21%, the highest in the loan portfolio. Still, this is significantly lower than it was at the start of the decade. Credit card delinquency was 1.92% in 2009. It declined every year until 2014, when it hit a low of 0.82%. Since then, delinquency has grown at double-digit rates; however, the 13.4% growth reported in the second quarter of 2019 was slower than the 16.5% reported one year ago.

Net charge-offs, another sign of asset quality, reached 3.5% for credit cards in the second quarter of 2019. That’s a year-over-year increase of 17 basis points; however, credit card charge-off growth was much slower than it has been in the past five years. Overall, credit cards accounted for 32.3% of total net charge-offs across all loan products at midyear. This is an increase of 7.7 percentage points since 2018.

CREDIT CARD ASSET QUALITY

FOR U.S. CREDIT UNIONS | DATA AS OF 06.30.19

Callahan & Associates | CreditUnions.com

Credit card delinquency has steadily increased over the past five years. It was 1.21% as of June 30, 2019.

Knowing the size and scale of the charged-off accounts are important considerations for credit quality improvement. Credit unions might have above-average losses compared to other loan products, but they also offer above-average returns if the credit union manages the portfolio well.

Consumer demand for credit cards is increasing across the nation. Technology advancements combined with the right reward program will help credit unions offer the popular payment method with an improved member experience.

What’s Next?

To learn how to better manage your credit card portfolio, read about these best practices only on CreditUnions.com:

- A Strategy To Achieve Double-Digit Card Growth: Suncoast Credit Union sparks a cards surge with an automatic, opt-out approach.

- Truity Takes The Pain Out Of Pre-Approvals: An automated credit card approval process at the Oklahoma cooperative makes it easy to deepen the member relationship.

- The Richest Credit Card In Credit Union Land?: InFirst FCU’s rewards card takes a move from Costco’s playbook and offers a rich deal.