Recently released mortgage data courtesy of the Home Mortgage Disclosure Act (HMDA) is a gold mine of insights on industry trends. Callahan & Associates has already written about the relationship-based, open-ended loans now included in the 2018 release and discussed how these loans more accurately reflect how credit unions are assisting their member-borrowers.

Readers are also likely to be interested in the results of another new, long-desired dataset: Market share across age ranges.

These trends can help highlight what attracts and what repels different generations, allowing credit unions to devise strategies to appeal to a new, young, or up-and-coming membership base.

INSTITUTIONAL MARKET SHARE BY AGE RANGE

FOR U.S. MORTGAGE LENDERS | DATA AS OF 12.31.18

Callahan & Associates | CreditUnions.com

| Age | <25 | 25-34 | 35-44 | 45-54 | 55-64 | 65-74 | 75+ | Totals |

|---|---|---|---|---|---|---|---|---|

| Totals ($000’s) | $36,923,380 | $363,349,635 | $462,654,783 | $395,149,835 | $279,603,735 | $144,705,820 | $43,922,895 | $1,726,310,083 |

| Credit Unions | 7.7% | 7.4% | 7.7% | 8.4% | 8.9% | 8.0% | 6.8% | 8.0% |

| Banks | 32.0% | 38.0% | 43.5% | 45.9% | 48.9% | 50.3% | 51.6% | 44.3% |

| HUD | 60.3% | 54.6% | 48.8% | 45.7% | 42.2% | 41.7% | 41.6% | 47.7% |

Consistency is key for credit unions. They hold a larger market share among older borrowers but need to look for ways to build relationships, and market share, among younger ones.

Credit unions hold an average market share of 8.0% for all borrowers (institutional borrowers have been excluded for the purpose of this data examination). Of note, cooperatives are the only lenders to hold a steady average market share across all age brackets. The greatest variance comes from borrowers 74 and older, who looked to credit unions for only 6.8% of their mortgage originations a difference of 1.2 percentage points from the mean.

Although HUD lenders including mortgage finance companies and banks control much larger shares of the mortgage market, they do not consistently appeal to all ages.

Is Your Mortgage Lending Strategy Working?

Home Mortgage Disclosure Act (HMDA) data was recently released. With the help of MortgageAnalyzer, you will be able to see the complete picture of leaders and laggards in mortgage lending and gather insight into the local mortgage market. Let us show you how you can create a winning mortgage lending strategy.

Learn More

HUD lenders with their online, tech-oriented foundations, extensive multimedia marketing campaigns, and (often) lower-cost selling points are particularly dominant among younger generations, holding a 51.7% share of the market for borrowers younger than 45. Though young people tend to appreciate the opportunity to apply for a mortgage using a smartphone app, this impersonal technology proves to be a harder sell to older borrowers. Market share for HUD lenders drops to 42.0% for borrowers older than 55.

Banks operate in the reverse. These traditional, relationship-based institutions control 49.6% of the 55 and older market versus 40.7% of the 44 and younger market, reflecting the relative struggle of banks to appeal to millennials.

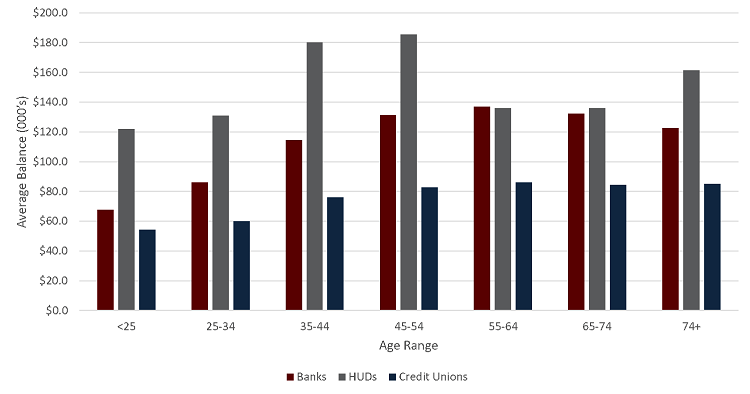

AVERAGE LOAN ORIGINATION

FOR U.S. MORTGAGE LENDERS | DATA AS OF 12.31.18

Callahan & Associates | CreditUnions.com

Cooperatives are, at heart, a platform for local members to help one another. This purpose is reflected in average origination size, which is smaller than banks and HUD lenders across all age ranges.

Average loan balances tell a similar story. The average mortgage balance peaks from the late 20s to the mid-40s when most homebuyers make their first large purchases. As with market share, the average loan balance issued by credit unions stays relatively flat over all age ranges, whereas banks and HUDs report far more variability.

Cooperatives average $147,000 per loan across all age groups. This is well below the $237,500 and $242,800 averages reported by banks and HUD lenders, respectively. Credit unions, however, control 12.4% of the total number of mortgage loans originated. This is significantly higher than their 8.0% share of total dollar originations. Credit union make their mark by offering a larger quantity of smaller loans, which reflects their mission to help small, local borrowers.

As banks and HUD lenders duke it out for the bulk of the market, credit unions are thriving in their niche market: borrowers who prioritize trust and reliable service over speed and low cost. Even online-oriented millennials and Gen-Zers borrow from credit unions at a rate similar to boomers and Gen-Xers. Though many in the industry feel uneasy about cooperatives abilities to make inroads with younger generations, 2018 numbers should be reassuring as performance remains consistent across all age groups.

Open-Ended Lending By Age Range

Although open-ended loans made up only 7.7% of the individual-buyer mortgage market in 2018, credit unions held a disproportionate 15.7% share of these relationship-based loans almost double their share of the overall market. This suggests borrowers like to use big brand banks and HUD lenders to finance home purchases but are more likely to turn to relationship-based lenders like retail banks and credit unions for a second loan.

| Age | <25 | 25-34 | 35-44 | 45-54 | 55-64 | 65-74 | 75+ | Totals |

|---|---|---|---|---|---|---|---|---|

| Totals ($000’s) | $137,670 | $6,057,265 | $22,199,530 | $34,234,300 | $36,016,460 | $24,248,730 | $9,936,115 | $132,830,070 |

| Credit Unions | 32.9% | 26.6% | 22.0% | 17.4% | 14.2% | 10.6% | 7.6% | 15.7% |

| Banks | 66.0% | 72.7% | 77.3% | 82.1% | 84.4% | 82.9% | 75.6% | 81.1% |

| HUD | 1.2% | 0.7% | 0.7% | 0.6% | 1.4% | 6.5% | 16.8% | 3.1% |

HUD lenders hold a surprising 16.8% market share in open-end loans for borrowers over age 74.

One point to note, however, is that credit unions lose market share in open-end lending as members age, whereas HUD lender market share grows. This pattern is the reverse of overall lending trends.

AVERAGE OPEN-ENDED LOAN ORIGINATION BALANCE

FOR U.S. MORTGAGE LENDERS | DATA AS OF 12.31.18

Callahan & Associates | CreditUnions.com

Although traditional lenders gain ground in later age groups, the small number of open-end loans originated by HUD lenders tend to particularly large across the board.

As members age and gain more equity in their home, they tend to take out larger open-ended loans for home improvement or other monetary needs. The average open-ended loan taken out by credit union members younger than 45 is $71,100. This grows to $84,500 after age 45.

The average open-ended loan at U.S. credit unions increases in lockstep with member age, yet market share declines correspondingly. In the future, cooperatives will need to balance their investments in cost-reducing technologies with their efforts to build interpersonal connections with borrowers.

HMDA data shows cooperatives do more business in rapport-based loan categories relative to other lenders. Learn more in Credit Unions Excel In Relationship Mortgage Lending on CreditUnions.com.