A recent executive order from President Trump directed the Department of Labor to begin allowing cryptocurrencies, private equity, and real estate in 401(k) investments.

While this change will take time to work its way through the regulatory system, it could set off a chain reaction resulting in a broader, and riskier, diversification of 401(k) assets.

The aim is to open up the more than 90 million employer-sponsored 401(k) plans to what are known as “alternative assets.” The White House bills this as a way for less wealthy Americans to participate in these burgeoning asset classes. As the stock market shrinks and private equity, real estate, and crypto expand, the White House sees the ability to participate in more areas of Wall Street as a win for Main Street.

Critics see opening up retirement funds to these asset classes as a way to introduce speculative products that savers often don’t quite understand into retirement savings.

While the new rules are pitched as an upside for retirement portfolios, they are not without controversy. Credit unions should be aware of these new rules and potential drawbacks – not just for members, but for their own fiduciary duties as 401(k) providers.

The Member Impact

For roughly 90 million Americans, 401(k)s are the main retirement plan. Credit unions strive to go beyond banking and to help members reach full financial wellness. Because of that, understanding the risks in these new rules is crucial for credit unions to better educate members to make the best decisions.

These risks include:

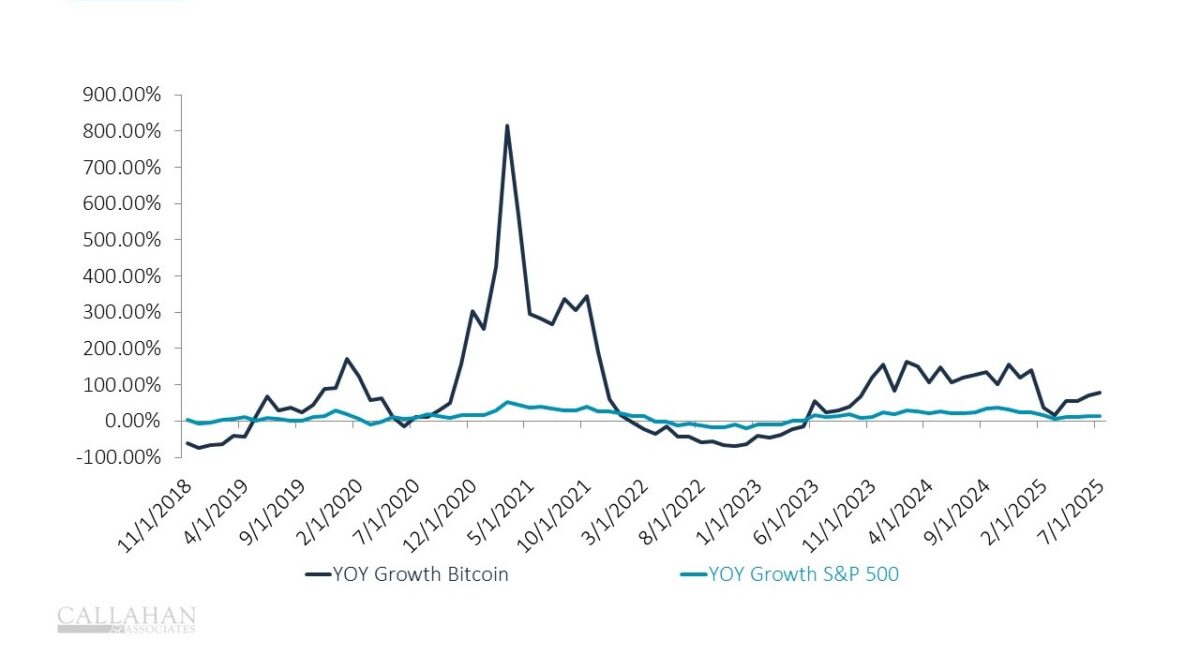

- Volatility: While private equity and some cryptocurrencies can see higher returns for investors, that often comes with higher volatility. That can be attractive for younger consumers whose 401(k) plans may not reach maturity for decades. But those closer to retirement could pay dearly. If that member’s portfolio is hit by a “crypto-winter,” as seen in 2022-23, it could prolong their retirement plans. Further, many finance experts are skeptical as to whether a plan centered on private equity can match the performance of a more traditional stock-and-bonds plan.

Annual Growth Rates of Bitcoin and S&P 500

DATA AS OF JULY 2025

SOURCE: CoinDesk and S&P Dow Jones Indices

- Cost: Investing in private equity and crypto funds can bring additional fees and costs to the member than a fund invested in a traditional portfolio. Over time, fees can add up and eat into compounding returns, costing members with 401(k) plans significant money. Further, liquidity issues with private equity funds can complicate 401(k) administration.

- Valuation: Private equity portfolios are not publicly listed, therefore it is more difficult to obtain up-to-the-minute price information prior to investing. Thus, members may not have a clear understanding of what they own and could have a difficult time running the financial calculations on whether to retire.

- Disclosure: Private equity investments and crypto are not disclosed in the same way as equities or publicly traded stocks, meaning there’s less oversight on performance or due diligence. 401(k) funds that are invested in public markets, on the other hand, are required to disclose their financial performance. This way, members can be confident that their investments are performing well and the custodians are taking care of their savings.

The Employee Impact

While these changes are important for members, there are also implications for employees, since many credit unions offer 401(k) plans as an employee benefit.

There are two key things for employers to keep in mind (including credit unions):

- Employers have a fiduciary responsibility, due to their control over plan management and assets. This is designed to ensure plan participants are not harmed by imprudent decisions by the employer.

- While President Trump’s executive order is designed to address these fiduciary obligations, there are still compliance requirements related to ensuring the funds have fair fees, transparent performance, and alignment with market returns.